- Q2 earnings come at sensitive time geopolitically and for the tech sector.

- AI and chip stocks to face scrutiny as Wall Street wobbles.

- Is the AI outlook still optimistic or are fears of a bubble well-founded?

Hyperscalers vs enablers

The Q2 earnings season is here, with Tesla and Alphabet kicking things off for the technology sector on July 22. Artificial intelligence (AI) stocks look set to dominate the season once again. But this time round, the focus is as much on AI enablers, if not more, as it is on the hyperscalers. Specifically, semiconductors were the big winners of the second quarter, as their stocks skyrocketed to new all-time highs.

Soaring demand for AI datacentre infrastructure is proving to be a boon for chipmakers as well as other datacentre equipment manufacturers. These so-called AI enablers are benefiting directly from all the spending on AI by hyperscalers such as Microsoft, Alphabet, Amazon, Meta and Oracle.

Whereas there’s a big question mark about whether all the AI investment will pay off for Wall Street’s big guys, the earnings prospects for the recipients of this spending are much more of a sure bet. Hence, investors have been piling into chipmakers these past few months, while losing enthusiasm for the usual favourites like the Magnificent Seven (M7).

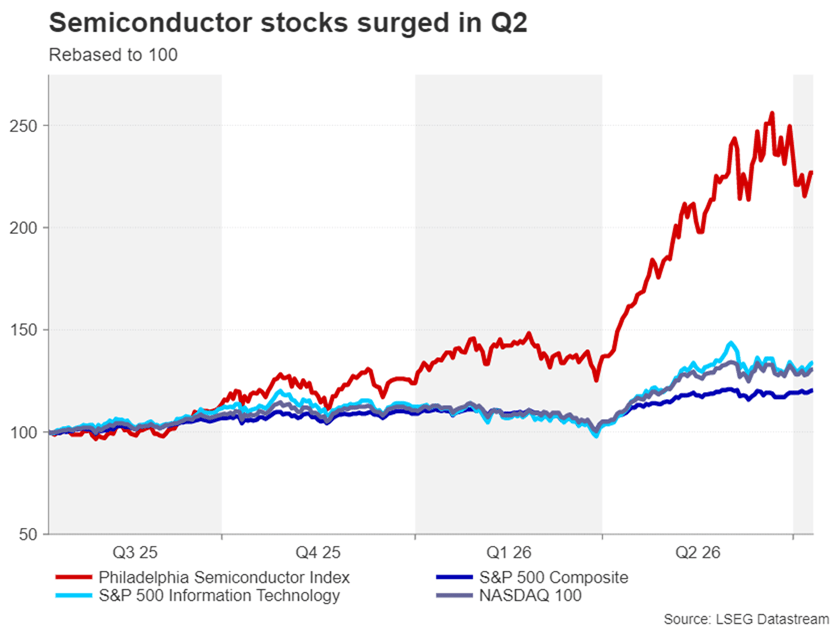

The semiconductor boom

The Philadelphia Semiconductor sector index, which measures the 30 largest US-traded companies that design and manufacture semiconductors, surged almost 88% in Q2. In comparison, the wider tech index – Nasdaq 100 – was up 27.5%, while the benchmark S&P 500 index gained nearly 15%.

The chip rally has created new trillion-dollar companies, notably Micron Technology and SK Hynix. Interestingly, current AI and chip giant Nvidia’s stock performance was more in line with those of the broader indices than the semiconductor gauge, as the company got caught in the AI frenzy much earlier on than its smaller rivals and its rally has started to cool off lately.

Heading into the Q2 earnings season, excitement is running high for the major chip stocks following the bumper earnings reported in the first quarter. The challenge is whether they will be able to sustain similar revenue growth while maintaining the bullish outlook for the upcoming quarters.

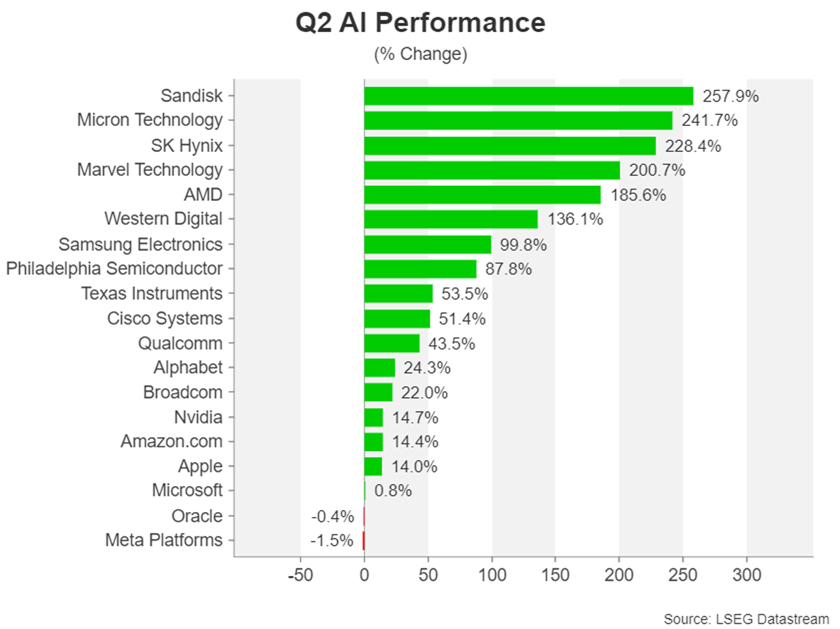

Chip stocks lead the way

For traders, though, the risk is that the triple-digit growth of Q1 will be a tough act to follow and therefore the scope for additional gains may be limited. Among the winners, Sandisk, Micron Technology and South Korea’s SK Hynix topped the leaderboard, while Meta, Oracle and Microsoft found themselves at the bottom of the table.

Although Oracle isn’t considered part of the Big Tech, worries about its spending plans and balance sheet are casting a shadow on an otherwise healthy earnings growth, as well as on the prospects of other hyperscalers. For Meta and Microsoft, there are growing doubts about their AI ambitions and earnings potentials, which don’t stack up as well when compared to their M7 peers like Alphabet and Amazon.

Going forward, the key questions for investors are: Is the strong demand holding up? How much optimism has already been priced into these stocks? And is the scarcity in memory and storage chips easing?

Rosy forecasts

The forecasts are certainly on the optimistic side. According to FactSet, Earnings growth for the S&P 500’s Information Technology (IT) sector is estimated at 63.3% y/y for the second quarter, which is the second highest behind the Energy sector (122.9% y/y).

Within the IT sector, semiconductors are doing much of the heavy lifting as their projected earnings growth of 131% far eclipses that of the other sub-sectors.

Apart from the Energy and IT sectors, Materials is the only other sector that’s expected to achieve faster earnings growth than the whole of the S&P 500, which is forecast at 23.6%.

Whilst the energy sector had a bumper quarter due to the jump in oil and gas prices from the US-Iran war, the AI boom has started to spread beyond IT, boosting the Materials sector. Specifically, companies engaged in the mining and production of raw materials such as metals are enjoying strong demand from the massive infrastructure spending on datacentres.

Non-tech sectors may struggle

The projections for the other sectors are not as upbeat, with only Utilities expected to achieve earnings growth of more than 10%. Nevertheless, the S&P 500 is headed for a second straight quarter of plus 20% earnings growth and the seventh with double digit growth.

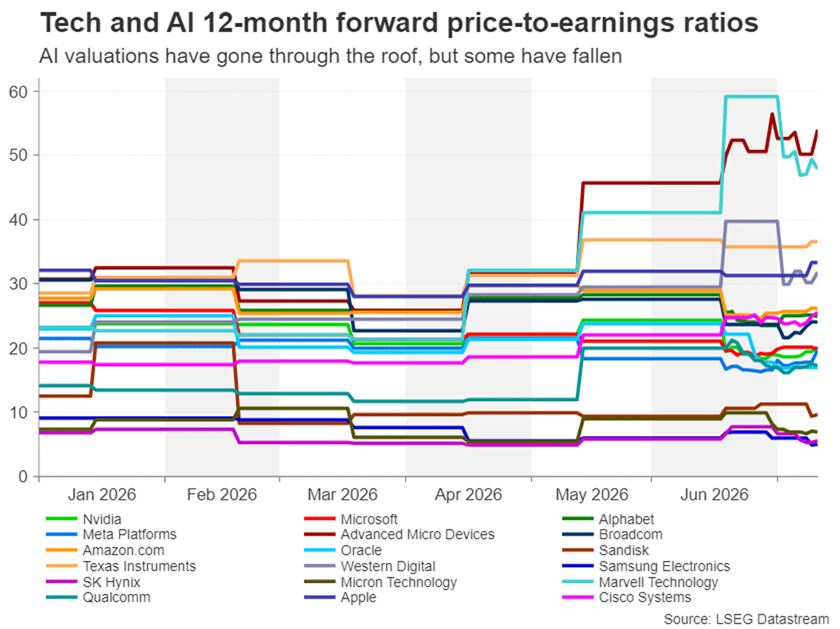

This is an impressive run given the Trade War in 2025 and the Middle East conflict just in the last quarter. But will traders be impressed? Many valuations are already considered to be at extremely overstretched levels, prompting comparisons with the dot-com bubble of the late 1990s.

Elon Musk’s Tesla and UK chipmaker ARM Holdings have forward price/earnings (P/E) ratios of 177 and 135, respectively, while Intel’s P/E is a lofty 82.5, all of which are far above the S&P 500 trailing average of just over 22. However, some P/E ratios have come down, such as Nvidia’s, and there are several chip stocks that still have below 20 P/Es, even after the recent rally.

Room to grow?

This suggests that if actual earnings match the expected results over the coming quarters and the outlook remains positive, there’s room for much more substantial gains for these stocks before becoming significantly overvalued.

Among them, Micron Technology, Qualcomm, SanDisk, Broadcom, Texas Instruments and Western Digital have all benefited from the explosion in new datacentres. The huge surge in demand has led to shortages in memory and storage chips, pushing up gross margins for the major producers. But others such as Advanced Micro Devices and Marvell Technology are looking somewhat overvalued with P/Es in the 50 region.

Nevertheless, with renewed jitters about the sustainability of the AI boom sparking a big selloff in chip stocks, the lower valuations may represent a buy-the-dip opportunity, even for some of the more expensive stocks. Yet, many traders will probably prefer to stay put until they’ve gotten a glimpse of what the new earnings season holds for the AI industry and the shifting dynamics within it.

Diverging valuations

Without a doubt, investors will be hoping to see continued double-digit growth in earnings in Q2 as well as upbeat guidance for the next few quarters. Any signs of a slowdown in revenue growth would likely spook markets. But it’s important to highlight that the risks differ for the hyperscalers and enablers.

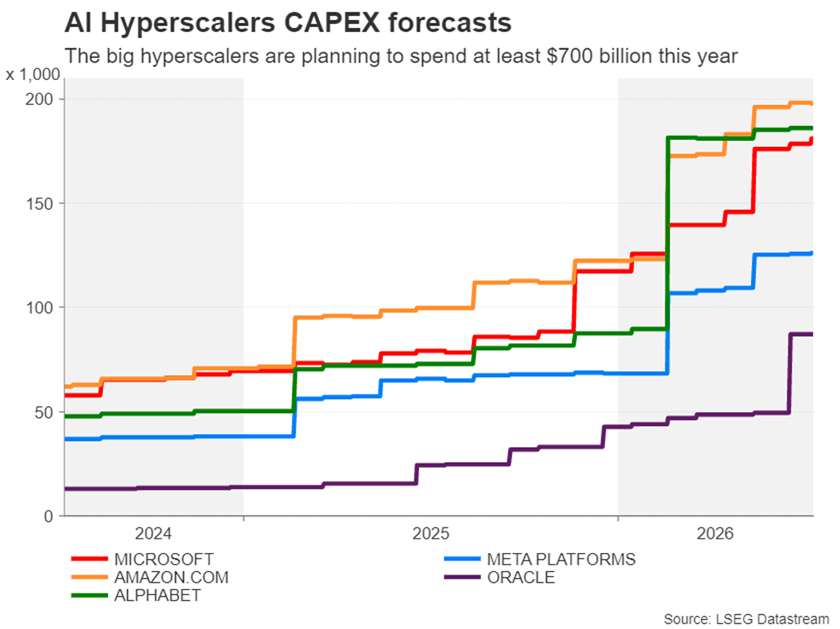

The key concern for the hyperscalers is that the record amount of capital expenditure being poured into AI is not delivering a satisfactory return on investment, particularly for those that are drying up their entire cash flows or resorting to new debt issuance to finance their AI ambitions.

The scarcity of memory chips and other AI components is also a problem for the hyperscalers, posing a two-way challenge, as it not only limits supply but also pushes up costs. Even the likes of Apple and Microsoft have been forced to hike the prices of some of their products, as margins have come under pressure. But for enablers, this is the windfall that’s been fuelling their stocks higher.

Risks to the outlook

That’s not to say that chip and AI equipment manufacturers are not susceptible to shortages themselves along the supply chain. Chipmakers additionally run the risk of overinvesting in their drive to expand production, potentially leading to a supply glut down the line.

The other danger for chipmakers is if the White House were to decide to loosen restrictions on Chinese memory chips – something Apple is lobbying the Trump administration for, easing the supply crunch and squeezing margins.

Beyond the AI-related developments, which are constantly evolving, there’s the turbulent geopolitical landscape, amid the ongoing US-Iran tensions that are boosting inflationary pressures by putting a strain on energy flows from the Gulf, and a more uncertain period of Fed policy, with rate hikes back on the horizon. The aforementioned have increased the risk of economic slowdown both in the United States and globally. A sharp economic pain makes it more likely that the big AI spenders would tighten their purse strings at some point, hurting AI enablers the most.

One might be asking, would Nvidia also be impacted from a cutback in AI investment? After all, the company has an order backlog of $1 trillion. But this is surely already priced into its stock price, so the answer is probably yes.

AI industry: It’s complicated

It’s important to bear in mind, however, that not all chipmakers are the same. Each serves a specific purpose within the processor architecture and semiconductor supply chain and therefore will be impacted differently by the AI headlines. Add to the mix the Big Tech hyperscalers and their varied fundamentals and the picture gets even more complicated.

One positive outcome of this is that it allows investors to rotate within the wider tech sector as demand and industry trends change. This pattern went into full swing in the second quarter and although it makes it more difficult to predict which way AI stocks will go, it’s a reminder that much of the AI industry is still in its infancy.

The Q2 earnings season will likely go only a small way in clearing all this up but will nonetheless be crucial in determining the short-to-medium term momentum in the AI trade. The one thing that has become more certain is that tech and AI stocks are more prone to large daily swings, warranting extra caution when trading them.

stocks look set to dominate the season once again. But this time round, the focus is as much on AI enablers, if not more, as it is on the hyperscalers. Specifically, semiconductors were the big winners of the second quarter, as their stocks skyrocketed to new all-time highs.){kind=link}