Dollar is trading in soft tone in range against most major currencies except versus Yen and Sterling. The greenback shrugs off stronger than expected PPI as markets are awaiting FOMC rate hike, economic projections and press conference. Sterling is trading as the weakest one today as headline UK CPI missed market expectations. But loss is limited so far. Yen is following as the second weakest. Meanwhile, New Zealand Dollar and Euro are the strongest one for today.

US Headline PPI rose 0.5% mom, 3.1% yoy in May, versus expectation of 0.2% mom, 2.8% yoy. Core PPI rose 0.3% mom, 2.4% yoy, versus expectation of 0.2% mom, 2.3% yoy. Focus will now turn to FOMC rate decision today. Fed is widely expected to raise federal funds rate by 25bps to 1.75-2.00%. Voting will be the first thing to watch even though it will very likely be unanimous. Fed will also release updated economic projections. The statement, as usual, will be scrutinized.

Awaiting FOMC, a look at Fed’s March projections

Currently, Fed fund futures are pricing in 75% chance of a hike in September 2.00-2.25%, but less than 50% chance for December hike to 2.25-2.50%. But market pricing could change drastically based on revision to Fed’s economic forecasts. To recap, back in March, Fed projected growth to be at 2.7% in 2018, to slow to 2.4% in 2019 then 2.0% in 2020. Unemployment rate is projected to be at 3.8% in 2018, dropped to 3.6% in 2019 and stay there in 2020. That is, Fed only expected the tax cut to have temporary boost to the economy. And based on recent economic data, Fed is not too likely to change these projections.

Headline CPI is projected to be at 1.9% in 2018, 2.0% in 2019 and 2.1% in 2020. Core CPI is projected to be at 1.9% in 2018, rise to 2.1% in 2019 and stay there in 2020. Headline PCE was already at 2.0% in April and core CPE at 1.8%. There is chance of an upgrade in inflation forecasts. And if Fed does, it would be Dollar positive.

Finally, and most importantly, Fed projects policy rate to be at 2.1% at the end of 2018, 2.9% in 2019 and 3.4% in 2020. That is, one more hike only this year, and three more next. Any chance to this set of figures could trigger strong reactions in the greenback.

Fed’s March projections:

More on FOMC

- FOMC Preview – Fed’s Rate Hike A Done Deal, Focus Turned to Forward Guidance

- FOMC Meeting: Rate Hike A ‘Done Deal’ But What About Inflation?

- Dollar Firm as Rate Hike Imminent; But Will Fed also Raise Rate Path Forecast?

Pound dips as UK CPI unchanged at 2.4% yoy, missed expectations

Sterling dips notably as UK consumer inflation data missed expectation. Headline CPI was unchanged at 2.4% yoy in May, below consensus of 2.5% yoy. Core CPI was also unchanged at 2.1% yoy, met expectations. RPI dropped to 3.3% yoy, down from 3.4% yoy and missed expectation of 3.4% yoy. But the pressure on the Pound is relatively mildly. While the set of inflation data doesn’t give BoE any push to hike in August, it doesn’t give a lot of reasons for BoE to wait. So, the MPC members and the markets would probably need another month of data before making up their mind.

PPI input was at 2.8% mom, 9.2% yoy, versus expectation f of 1.7% mom, 7.0% yoy, and prior 0.6% mom, 5.6% yoy. PPI output was at 0.4% mom, 2.9% yoy, versus expectation of 0.3% mom, 2.9% yoy, and prior 0.4% mom, 2.5% yoy. PPI output core was at 0.2% mom, 2.1% yoy, versus expectation of 0.1% mom, 2.2% yoy, and prior 0.2% mom, 2.0% yoy. UK House price index rose 3.9% yoy in April, below expectation of 4.4% yoy.

Also released in European session, Eurozone industrial production dropped -0.9% mom in April versus expectation of -0.5% mom. Eurozone employment rose 0.4% in Q1 versus expectation of 0.3% qoq. Swiss PPI rose 0.2% mom, 3.2% yoy in May versus expectation of 0.2% mom, 3.2% yoy.

RBA Lowe: Any increase in interest rates, they’re some time away

RBA Governor Philip Lowe delivered a speech titled “Productivity, Wages and Prosperity” today. There he pointed out that “over the past couple of years, output growth has been subdued, but employment growth has been strong.” And, it’s productivity that’s holding the economy back. Low pointed to strong employment growth in household services, but output per hour worked was only 4% higher than it was in 2010. In contrast, the output per hour worked was up 13% to 16% in other industry groups.

He urged “strong ongoing focus on training, education and the accumulation of human capital” to bring up the overall productivity. And he emphasized that “our national comparative advantage will increasingly be built on the quality of our ideas and our human capital.”

Regarding monetary policy, Lowe said the economy is “moving in the right direction” and the next move in interest rate will be “up, not down”. But, “the environment in which interest rates are increasing is also likely to be one in which people’s incomes are growing more quickly than they are now.”And, “any increase in interest rates, however, still looks to be some time away.”

Also released, Australia Westpac consumer confidence rose 0.3% in June.

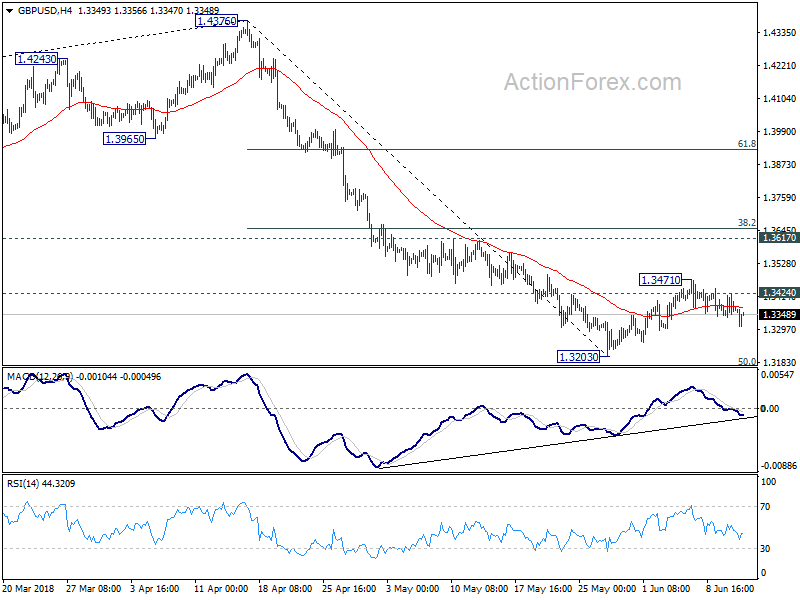

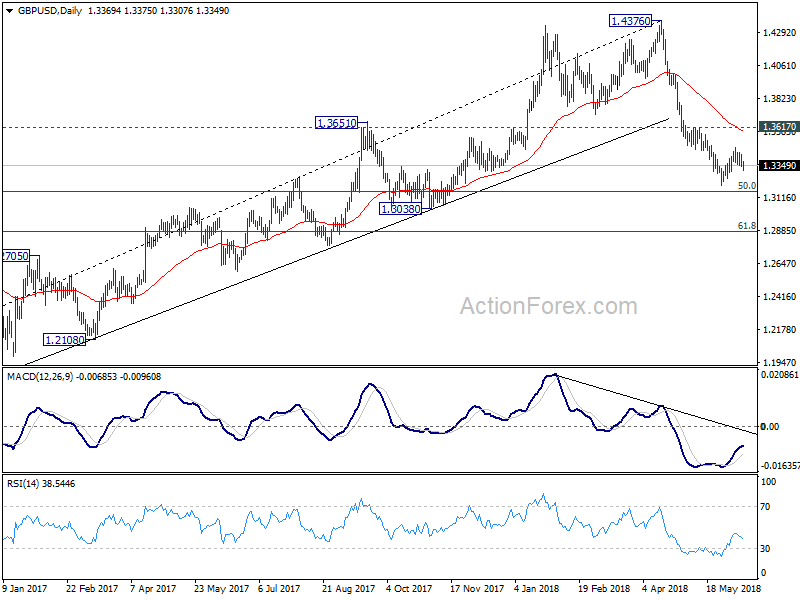

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3333; (P) 1.3379; (R1) 1.3416; More…

GBP/USD drops to as low as 1.3307 so far today. Break of 1.3341 minor support indicate completion of corrective rise from 1.3203. Intraday bias is now on the downside for 1.3203. Break will resume the fall from 1.4376 to 50% retracement of 1.1946 to 1.4376 at 1.3161 first, and 61.8% retracement at 1.2875 next. Nonetheless, above 1.3424 minor resistance will extend the corrective rise through 1.3471 before completion..

In the bigger picture, current development suggests that whole medium term rebound from 1.1936 (2016 low) has completed at 1.4376 already, with trend line broken firmly, on bearish divergence condition in daily MACD, after rejection from 55 month EMA (now at 1.4223). 61.8% retracement of 1.1936 (2016 low) to 1.4376 at 1.2874 is the next target. We’ll pay attention to the reaction from there to asses the chance of long term down trend resumption. For now, outlook will stay bearish as long as 1.3617 resistance holds, even in case of strong rebound..

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 00:30 | AUD | Westpac Consumer Confidence Jun | 0.30% | -0.60% | ||

| 07:15 | CHF | Producer & Import Prices M/M May | 0.20% | 0.10% | 0.40% | |

| 07:15 | CHF | Producer & Import Prices Y/Y May | 3.20% | 3.20% | 2.70% | |

| 08:30 | GBP | CPI M/M May | 0.40% | 0.40% | 0.40% | |

| 08:30 | GBP | CPI Y/Y May | 2.40% | 2.50% | 2.40% | |

| 08:30 | GBP | Core CPI Y/Y May | 2.10% | 2.10% | 2.10% | |

| 08:30 | GBP | RPI M/M May | 0.40% | 0.40% | 0.50% | |

| 08:30 | GBP | RPI Y/Y May | 3.30% | 3.40% | 3.40% | |

| 08:30 | GBP | PPI Input M/M May | 2.80% | 1.70% | 0.40% | 0.60% |

| 08:30 | GBP | PPI Input Y/Y May | 9.20% | 7.00% | 5.30% | 5.60% |

| 08:30 | GBP | PPI Output M/M May | 0.40% | 0.30% | 0.30% | 0.40% |

| 08:30 | GBP | PPI Output Y/Y May | 2.90% | 2.90% | 2.70% | 2.50% |

| 08:30 | GBP | PPI Output Core M/M May | 0.20% | 0.10% | 0.10% | 0.20% |

| 08:30 | GBP | PPI Output Core Y/Y May | 2.10% | 2.20% | 2.40% | 2.00% |

| 08:30 | GBP | House Price Index Y/Y Apr | 3.90% | 4.40% | 4.20% | |

| 09:00 | EUR | Eurozone Industrial Production M/M Apr | -0.90% | -0.50% | 0.50% | |

| 09:00 | EUR | Eurozone Employment Q/Q Q1 | 0.40% | 0.30% | 0.30% | |

| 12:30 | USD | PPI M/M May | 0.50% | 0.20% | 0.10% | |

| 12:30 | USD | PPI Y/Y May | 3.10% | 2.80% | 2.60% | |

| 12:30 | USD | PPI Core M/M May | 0.30% | 0.20% | 0.20% | |

| 12:30 | USD | PPI Core Y/Y May | 2.40% | 2.30% | 2.30% | |

| 14:30 | USD | Crude Oil Inventories | -1.4M | 2.1M | ||

| 18:00 | USD | FOMC Rate Decision (Upper Bound) | 2.00% | 1.75% | ||

| 18:00 | USD | FOMC Rate Decision (Lower Bound) | 1.75% | 1.50% | ||

| 18:30 | USD | FOMC Press Conference |