Dollar got a very brief lift overnight as Fed delivered a hawkish rate hike. But it quickly lost steam as weighed down by concern over trade war between US and China. For today, the greenback is only trading slightly better than Australian Dollar, which is weighed down by its down job data and China data. Euro, on the other hand, is picking up a little bit of strength today as focus now turns to ECB rate decision and press conference. Sterling is mixed despite yesterday’s CPI miss as focus will turn to retail sales.

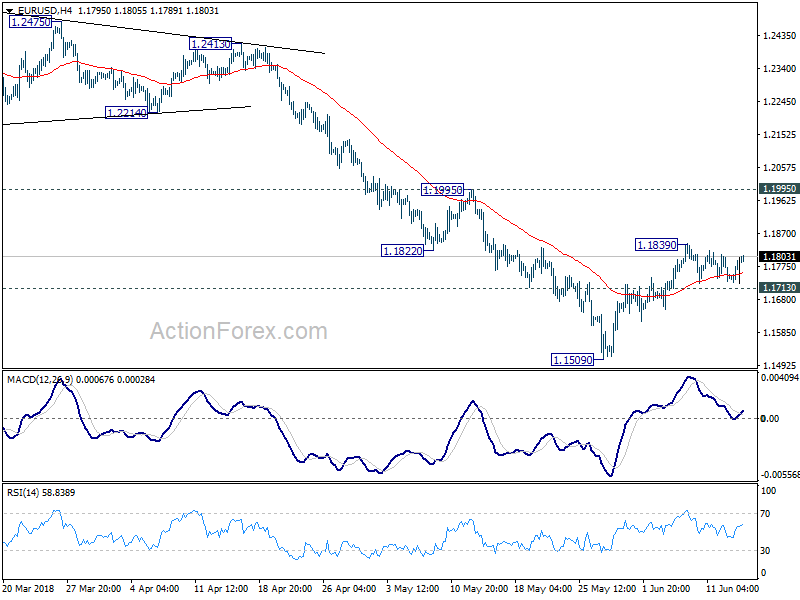

Technically, EUR/USD is holding in tight range above 1.1713 minor support and there is prospect of extending the near term rebound from 1.1509. 1.1839 resistance is the level to watch in EUR/USD. USD/JPY lost much momentum after hitting 110.84 and focus is back on 109.18 minor support. EUR/GBP is still resiliently held below 0.8844 resistance as range trading continue. But ECB meeting could provide the trigger for a breakout.

Fed delivered hawkish rate hike and projections

Fed delivered the widely expected rate hike overnight, with hawkish statement and economic projections. FOMC raised the Fed funds rate by +25 bps to a range of 1.75-2.00%. In a technical adjustment, it also lifted the interest rate paid on required and excess reserve balances, by +20 bps, to 1.95% so as to maintain the trading in the fed funds market at rates well within the FOMC’s target range.

The members are more upbeat on the economic developments since the last meeting, noting “solid” growth, compared with “moderate” growth in the prior meeting. The staff upgraded the GDP growth forecast for this year and inflation outlook for this year and 2019. The median dot plot suggests 2 more rate hikes, one more than projected in the prior meeting.

More in Fed Raised Policy Rate in June. Two More to Come amidst Upbeat Economic Developments

Also on Fed:

- Dollar jumps on hawkish Fed projections, four hikes in total this year

- FOMC Recap: Hawkish Statement And Projections, Hesitant Powell

- FOMC Review: Four Hikes More Likely After Removal Of Soft Wordings

- FOMC Raises Funds Rate Target, Alters Forward Guidance

- FOMC Raises the Fed Funds Rate to Range of 1¾ to 2 Percent

- Fed Raises Rates, Drops Forward Guidance in Pared Down Statement

Dollar gains capped by trade war concerns

The concern of trade war is a main factor that’s weighing down the greenback. It’s reported that Trump is ready to snap tariffs on USD 50B of Chinese imports. The original list consists of around 1300 product lines. Trade advisor Peter Navarro’s comments suggested that the tariffs could be on a “subset” of the original list. The decision would be made on Thursday today, and the final list of products would be unveiled on Friday.

To recap, that’s the action under section 301 investigation in response to forced transfer of U.S. technology and intellectual property. It’s different from the section 232 steel and aluminum tariffs against the world. The section 301 tariffs solely targeted at China.

South Korean Moon approved the result of Kim-Trump summit

South Korean President Moon Jae-in met with US Secretary of State Mike Pompeo today and gave a nod to what the US has done in the Kim-Trump summit. Moon said that “there have been many analyses on the outcome of the summit but I think what’s most important was that the people of the world, including those in the United States, Japan and Koreans, have all been able to escape the threat of war, nuclear weapons and missiles.”

Pompeo said that “we’re hopeful that we can achieve that in the 2-1/2 years,” referring the major nuclear disarmament in North Korea. And he tweaked the meaning of “complete” and said it “encompasses verifiable and irreversible” denuclearization. But no one asked him when the word “complete” started including those extra meaning.

In Japan, the Yomiuri newspaper reported that Prime Minister Shinzo Abe is arranging a meeting with North Korean Leader Kim Jong-un, possibly in Pyongyang around August.

Australian Dollar lower on job and China data

Australian Dollar is trading as the weakest one today as pressured by its own data miss as well as weaker than expected China data. Australia employment rose 12k seasonally adjusted in May, below consensus of 19.2k. Unemployment rate dropped to 5.4%, as participation rate also dropped to 65.5%.

From China, retail sales rose 8.5% yoy in May, slowed from 9.4% yoy and missed expectation of 9.6% yoy. Industrial production slowed to 5.8% yoy, down from 7.0% yoy and missed expectation of 7.0% yoy. Fixed asset investment slowed to 6.1% yoy, down from 7.0% yoy and missed expectation of 7.0% yoy.

High expectation on ECB but beware of dovish tweak

ECB rate decision and press conference is the biggest focus today. Expectations is high after chief economist Peter Praet said it’s a “judgement call” this week on the EUR 30B/month asset purchase program, which is going to end in September. With Eurozone inflation picked up again in May, ECB should be much more comfortable to end the asset purchase program this year.

However, the tricky point is, if they don’t end the program after September, it doesn’t make much sense to taper it for another three months till December. If ECB extends the tapered program for six months, it will push away the timing of the first rate hike, which will be Euro negative. Stopping the program right after September is certainly Euro positive. But are they confident enough to do so? It’s doubtful. Adding to that, it’s still possible for ECB to wait until July to make that judgement. Hence, there could be some dovish tweaks out of the meeting.

Here are some suggested readings on ECB:

- ECB: More Upbeat, But June May be Too Early for QE Commitment

- ECB Ready To Map The End Of APP

- ECB Preview – Members to Discuss QE Tapering This Week, Attention Moves to Rate Hike Path and Forward Guidance

On the data front – UK and US retail sales watched

UK retail sales will also be a focus in European session while Germany will release May CPI final. US retail sales will catch most attention later in the day, when import price index, jobless claims and business inventories will also be featured. Canada will release new housing price index.

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1745; (P) 1.1773 (R1) 1.1822; More…..

Outlook in EUR/USD remains unchanged. It’s staying in tight range of 1.1713/1839 and intraday bias remains neutral. On the upside, break of 1.1839 will extend the rebound from 1.1509. But as it’s seen as a correction, upside should be limited by 1.1995 resistance to bring reversal. On the downside, break of 1.1713 will argue that such correction is finished. Intraday bias would then be turned back to the downside to resume larger fall from 1.2555, through 1.1509 to 50% retracement of 1.0339 to 1.2555 at 1.1447.

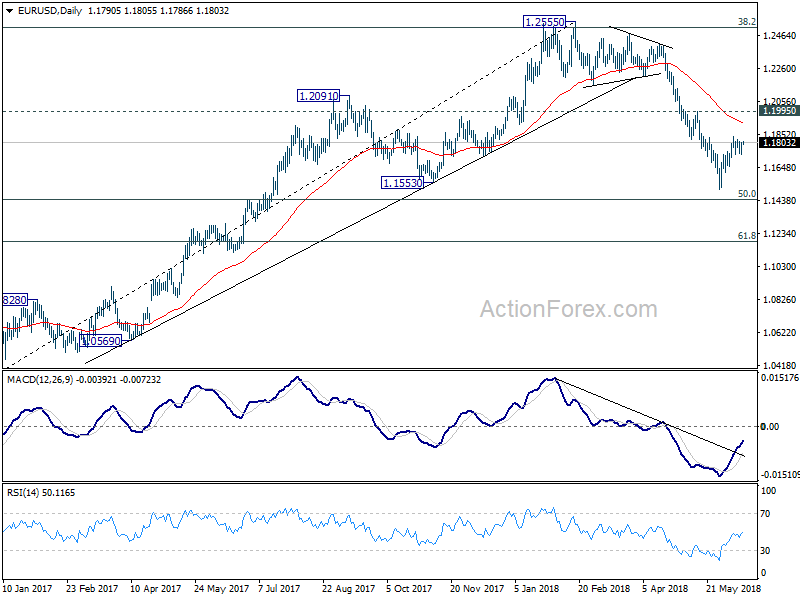

In the bigger picture, current development suggests that EUR/USD was rejected by 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. And, a medium term top was formed at 1.2555 already. Decline from there should extend further to 61.8% retracement of 1.0339 to 1.2555 at 1.1186 and below. For now, even in case of rebound, we won’t consider the fall from 1.2555 as finished as long as 1.1995 resistance holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:01 | GBP | RICS House Price Balance May | -3% | -5% | -8.00% | -7% |

| 01:00 | AUD | Consumer Inflation Expectation Jun | 4.20% | 3.70% | ||

| 01:30 | AUD | Employment Change May | 12.0K | 19.2K | 22.6k | 18.3K |

| 01:30 | AUD | Unemployment Rate May | 5.40% | 5.60% | 5.60% | |

| 02:00 | CNY | Retail Sales Y/Y May | 8.50% | 9.60% | 9.40% | |

| 02:00 | CNY | Industrial Production Y/Y May | 6.80% | 7.00% | 7.00% | |

| 02:00 | CNY | Fixed Assets Ex Rural YTD Y/Y May | 6.10% | 7.00% | 7.00% | |

| 04:30 | JPY | Industrial Production M/M Apr F | 0.50% | 0.30% | 0.30% | |

| 06:00 | EUR | German CPI M/M May F | 0.50% | 0.50% | ||

| 06:00 | EUR | German CPI Y/Y May F | 2.20% | 2.20% | ||

| 08:30 | GBP | Retail Sales Inc Auto Fuel M/M May | 0.50% | 1.60% | ||

| 11:45 | EUR | ECB Rate Decision | 0.00% | |||

| 12:30 | EUR | ECB Press Conference | ||||

| 12:30 | CAD | New Housing Price Index M/M Apr | 0.20% | 0.00% | ||

| 12:30 | USD | Retail Sales Advance M/M May | 0.40% | 0.30% | ||

| 12:30 | USD | Retail Sales Ex Auto M/M May | 0.30% | 0.30% | ||

| 12:30 | USD | Import Price Index M/M May | 0.50% | 0.30% | ||

| 12:30 | USD | Initial Jobless Claims (Jun 09) | 223K | 222K | ||

| 14:00 | USD | Business Inventories Apr | 0.30% | |||

| 14:30 | USD | Natural Gas Storage |

{kind=link}