US equities’ up trend resumed overnight with all three major indices closed at new record highs. Sentiments were lifted by news that US president Donald Trump will deliver a "phenomenal" plan to overhaul taxes on business without "two or three weeks". DJIA jumped 118.06 pts, or 0.59%, to close at 118.06. S&P 500 rose 13.2 pts, or 0.58%, to close at 2307.87. NASDAQ rose 32.73 pts, or 0.58%, to close at 5715.18. Treasury yields followed with 10 year yield gained 0.044 to close at 2.395. 30 year yield rose 0.050 to close at 3.011. Dollar also strengthened some what but the dollar index lost momentum after hitting 100.73, limited by 55 day EMA (now at 100.66). In the currency markets, Yen is the biggest loser for the day and with USD/JPY, EUR/JPY and GBP/JPY took out minor resistance level, suggesting more upside.

10 year yield recovered some support from 55 day EMA and recovered. The development affirmed the view that price actions from 2.621 are merely forming a consolidation pattern. That is, up trend from 1.336 remains intact. This is also in line with the view that Dollar index should receive strong support from around 99.43 to bring up trend resumption. Real focus is on 2.621 resistance in TNX. Decisive break there will confirm rally resumption and that should help pull dollar index back to 103.82 high. However, sustained trading below 55 day EMA (now at 2.357) will dampen our view and turn focus to 38.2% retracement of 1.336 to 2.621 at 2.130.

St. Louis Fed Bullard: Why Not Wait?

St. Louis Fed president James Bullard said that "it is unlikely that fiscal uncertainty will be meaningfully resolved by the March meeting, which is only a few weeks away." Therefore, "why not wait until that gets resolved?" He emphasized that "there is some downside risk as well as upside to the growth rate in the U.S. economy." And policymakers should see what the fiscal package is really going to be before moving on rates. Chicago Fed president Charles Evans reiterated yesterday that it is "not unreasonable, and that’s three" rate hikes. He noted that "there is uncertainty but it’s got a particular direction to it in terms of economic stimulus" and that direction is "up," he said of fiscal policies.

Shinzo Abe to Meet Donald Trump

The meeting between US president Donald Trump and Japan prime minister Shinzo Abe in Washington today will be closely watched by the markets. While there are news surrounding Trump’s accusation of Japan as currency manipulator and others, the key would be the development in trade relationships of the two countries. Trump dismissed the Trans Pacific Partnership in his very early days in office. And it’s known that Abe would like to secure a bilateral trade deal with the US.

China trade surplus widened to USD 51.4b in January, up from USD 40.8b, and beat expectation of USD 48.8b. In CNY terms, trade surplus widened to CNY 354.5b, up from CNY 275.4b, and beat expectation of CNY 295.3b. Japan domestic CGPI rose 0.5% yoy in January. Australia home loans rose 0.4% in December. UK trade balance will be released in European session, together with productions. Canada employment will be the main focus in US session. US will release import price index and U of Michigan sentiment.

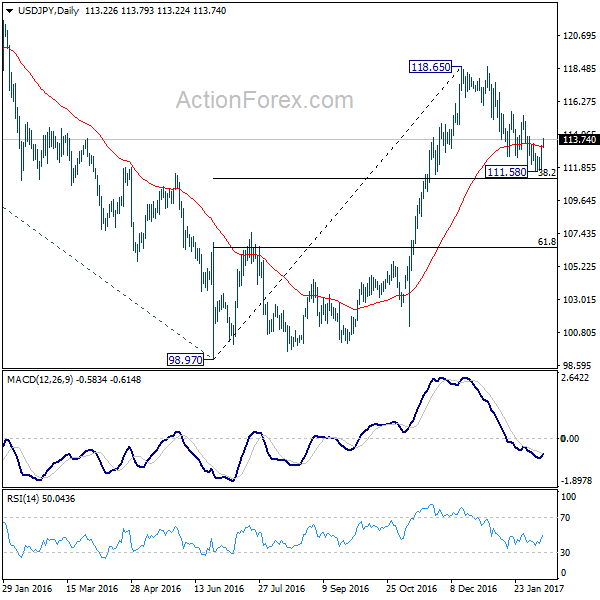

USD/JPY Daily Outlook

Daily Pivots: (S1) 112.19; (P) 112.76; (R1) 113.81; More…

USD/JPY rebounds strongly with a break of 113.44 minor resistance. The development suggests that correction fro 118.65 has completed at 111.58 already, ahead of 38.2% retracement of 98.97 to 118.65 at 111.13. Intraday bias is mildly on the upside for 115.36 resistance next. Break will confirm this bullish case and target 118.65 high next. In that case, the larger rally from 98.97 could be resuming.

In the bigger picture, price actions from 125.85 high are seen as a corrective pattern. The impulsive structure of the rise from 98.97 suggests that the correction is completed and larger up trend is resuming. Decisive break of 125.85 will confirm and target 61.8% projection of 75.56 to 125.85 from 98.97 at 130.04 and then 135.20 long term resistance. Rejection from 125.85 and below will extend the consolidation with another falling leg before up trend resumption.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Consensus | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Domestic CGPI Y/Y Jan | 0.50% | 0.00% | -1.20% | |

| 0:30 | AUD | Home Loans Dec | 0.40% | 1.00% | 0.90% | 1.30% |

| 0:30 | AUD | RBA Statement on Monetary Policy | ||||

| 3:30 | CNY | Trade Balance (USD) Jan | 51.4B | 48.8B | 40.8B | |

| 3:30 | CNY | Trade Balance (CNY) Jan | 354.5B | 295.3B | 275.4B | |

| 4:30 | JPY | Tertiary Industry Index M/M Dec | -0.20% | 0.20% | ||

| 9:30 | GBP | Visible Trade Balance (GBP) Dec | -11.5B | -12.1B | ||

| 9:30 | GBP | Industrial Production M/M Dec | 0.20% | 2.10% | ||

| 9:30 | GBP | Industrial Production Y/Y Dec | 3.20% | 2.00% | ||

| 9:30 | GBP | Manufacturing Production M/M Dec | 0.50% | 1.30% | ||

| 9:30 | GBP | Manufacturing Production Y/Y Dec | 1.70% | 1.20% | ||

| 9:30 | GBP | Construction Output M/M Dec | 1.00% | -0.20% | ||

| 13:30 | CAD | Net Change in Employment Jan | 0.0k | 53.7k | ||

| 13:30 | CAD | Unemployment Rate Jan | 6.90% | 6.90% | ||

| 13:30 | USD | Import Price Index M/M Jan | 0.20% | 0.40% | ||

| 15:00 | GBP | NIESR GDP Estimate Jan | 0.50% | |||

| 15:00 | USD | U. of Michigan Confidence Feb P | 97.8 | 98.5 |

Subscribe to our daily and mid-day newsletter to get this report delivered to your mail box

{kind=link}