- Fed meets as strong US data bolster rate hike bets.

- BoJ expected to hike, intervention risk also in focus.

- RBA to remain on hold, hawkish message could boost Aussie.

- BoE to also stand pat, inflation outlook to shape rate path speculation.

Fed Rate Hike Expected by the End of the Year

The US dollar outperformed most of its major counterparts this week, with investors remaining convinced that the Fed may need to press the rate hike button before the end of this year.

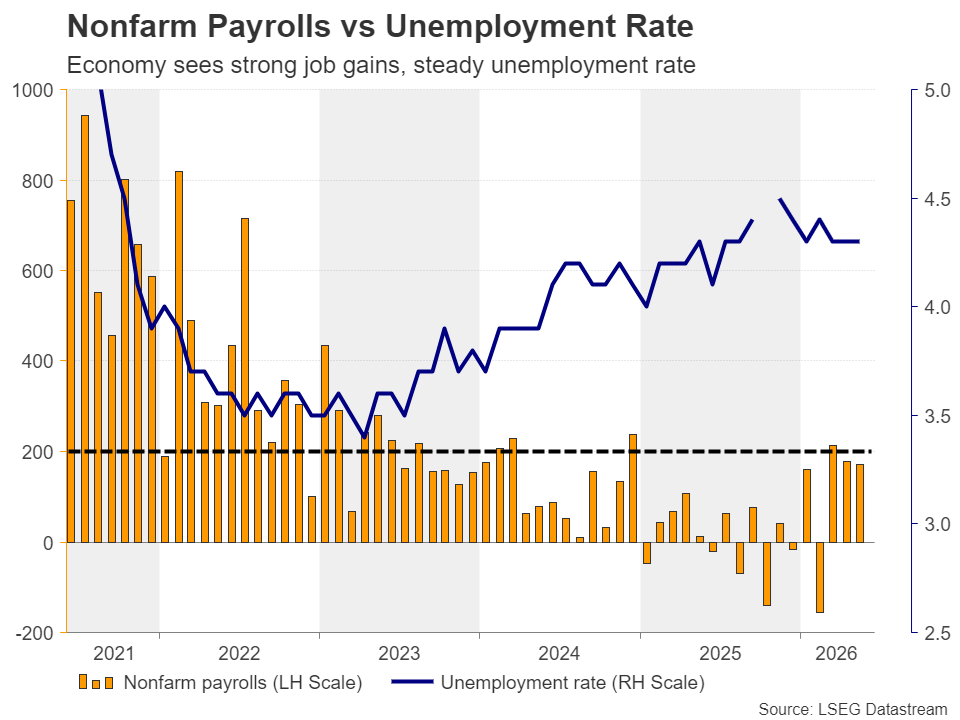

Fed hike bets were significantly bolstered after the US jobs report for May came in much stronger than expected, with nonfarm payrolls rising to 172k and confounding expectations of a much more modest 85k gain. April’s figure was revised up to 179k from 115k initially, while the unemployment rate held steady at 4.3%.

The report painted a picture of a labor market astoundingly strong considering the ongoing conflict in the Middle East and the resulting energy crisis, giving the Fed the green light to proceed with a tighter monetary policy stance.

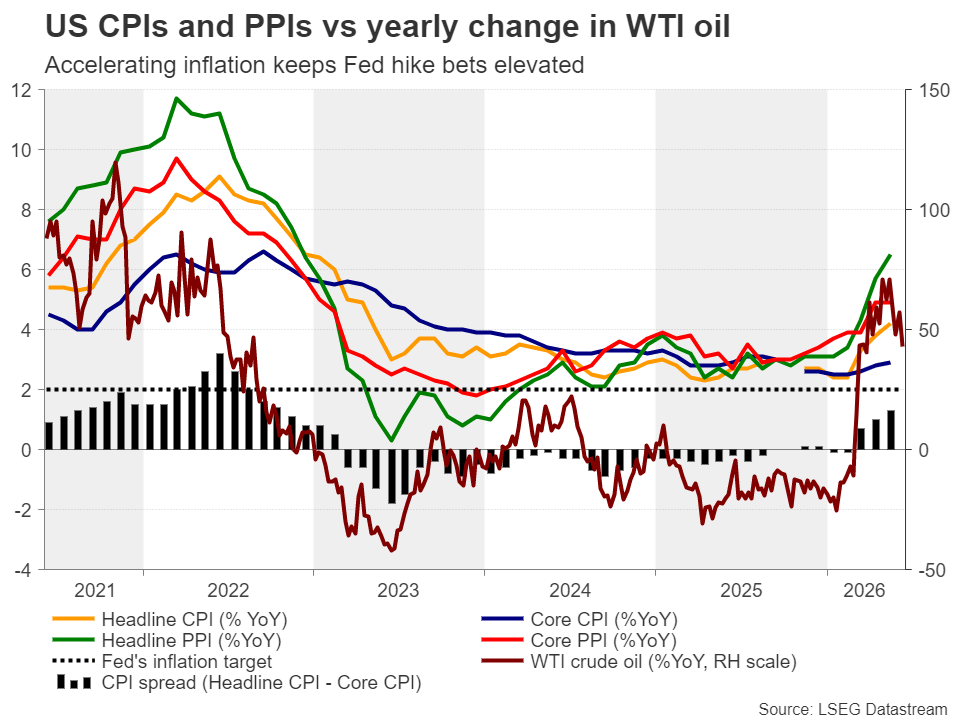

Although investors remained somewhat hopeful about a truce in the Middle East despite several episodes of hostilities during the week, they maintained their hawkish bets, especially after the US CPI data for May revealed that the headline rate rose from 3.8% y/y to 4.2%, more-than-double the Fed’s objective of 2%, with the core rate ticking up to 2.9% y/y from 2.8%.

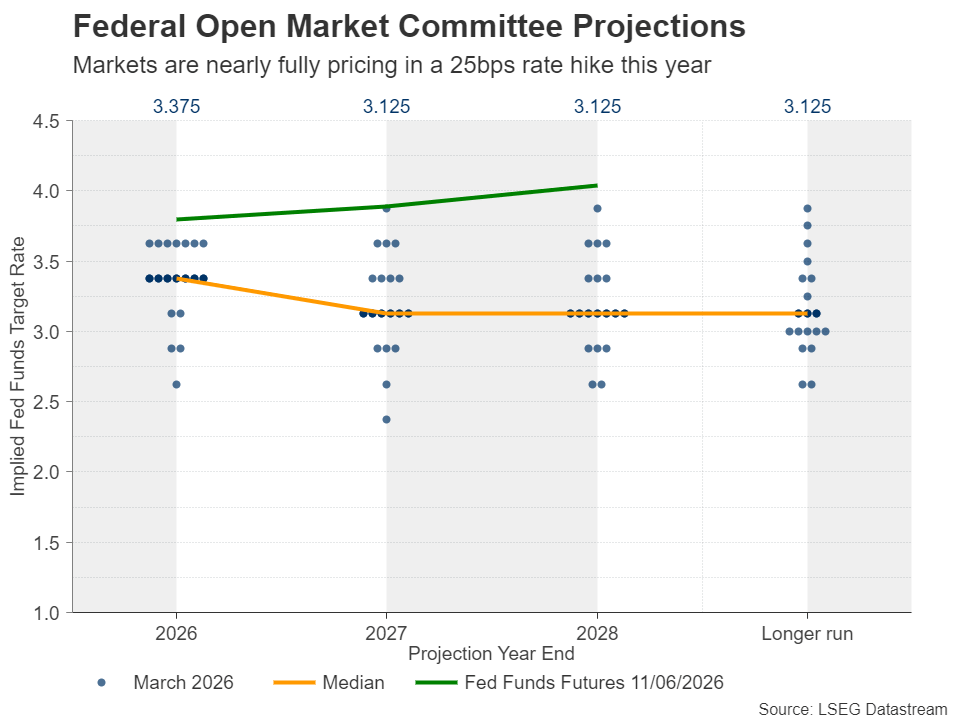

According to Fed funds futures, a 25bps rate hike is nearly fully priced in for December, while the probability of it being delivered in September is almost 35%. And this is even after US President Trump said that they have agreed with Iran on peace deal, which will be signed very soon.

Will the Fed Satisfy Hawkish Market Expectations?

With Wednesday’s meeting being the first of the new Chair, Kevin Warsh, it is unlikely that the Fed will press the hike button before September. After all, Warsh was appointed by US President Trump, on the premise that he holds a less hawkish view than his predecessor Jerome Powell.

Thus, the spotlight will be on how Warsh’s communicates his views and whether there will be strong signals about rate hikes amid concerns and upside risks to the inflation outlook. If indeed Warsh and his colleagues maintain concerns about inflation spiraling out of control, and the new dot plot, not only removes previously anticipated rate cuts, but shifts towards rate hikes, then the US dollar’s engines are likely to receive more fuel as Treasury yields march higher and the probability of a September rate hike increases.

Strong US industrial production numbers on Monday, and solid retail sales prints on Wednesday, ahead of the Fed announcement, could add more credence to hawkish market bets.

BoJ Set to Hike, but More Is Needed for the Yen to Stage a Comeback

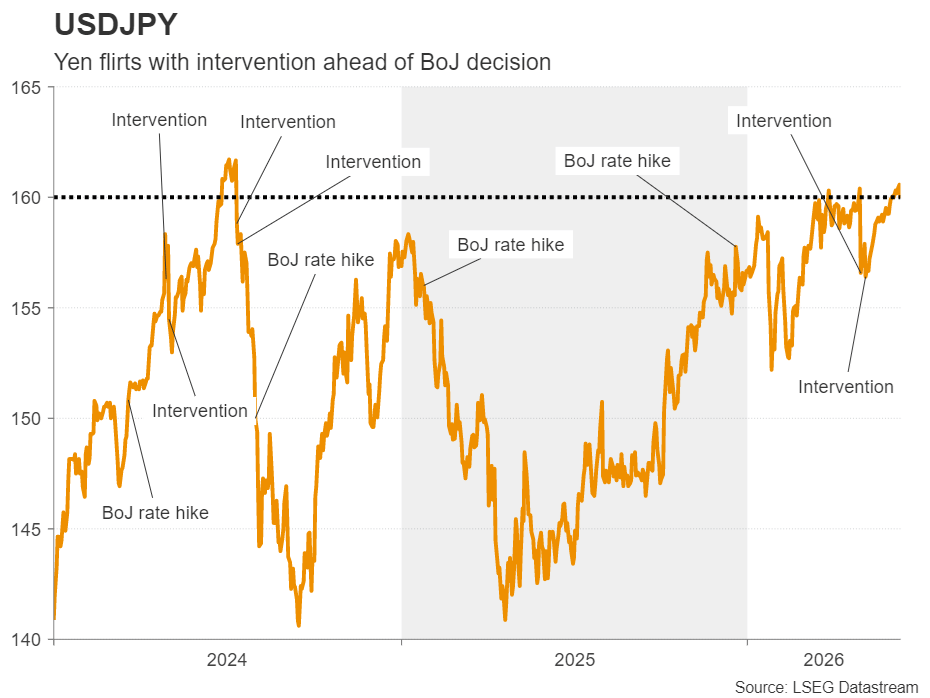

The yen continued suffering, with traders testing waters above the 160-per-dollar mark. Although market participants may be sitting on the edge of their toes in anticipation of a potential intervention episode, they are also keeping an eye on Tuesday’s BoJ decision, scheduled during the Asian morning.

The Bank is largely expected to raise interest rates at its upcoming meeting, but that is not necessarily a helping hand for the yen, as the move is already priced in. For the yen to stage a meaningful recovery, an intervention episode alone, even accompanied by an upcoming rate hike, may not be enough. The BoJ may have to appear even more hawkish, signaling additional increases in borrowing costs for the months to come. In other words, a hawkish hike by the BoJ and an intervention episode just ahead of or after the meeting may be the successful recipe for a bullish reversal in the yen.

Towards the end of the week, during the Asian session Friday, Japan’s National CPI data will be released and will prove whether the BoJ should remain concerned about inflation getting out of control, even if officials do press the hike button on Tuesday.

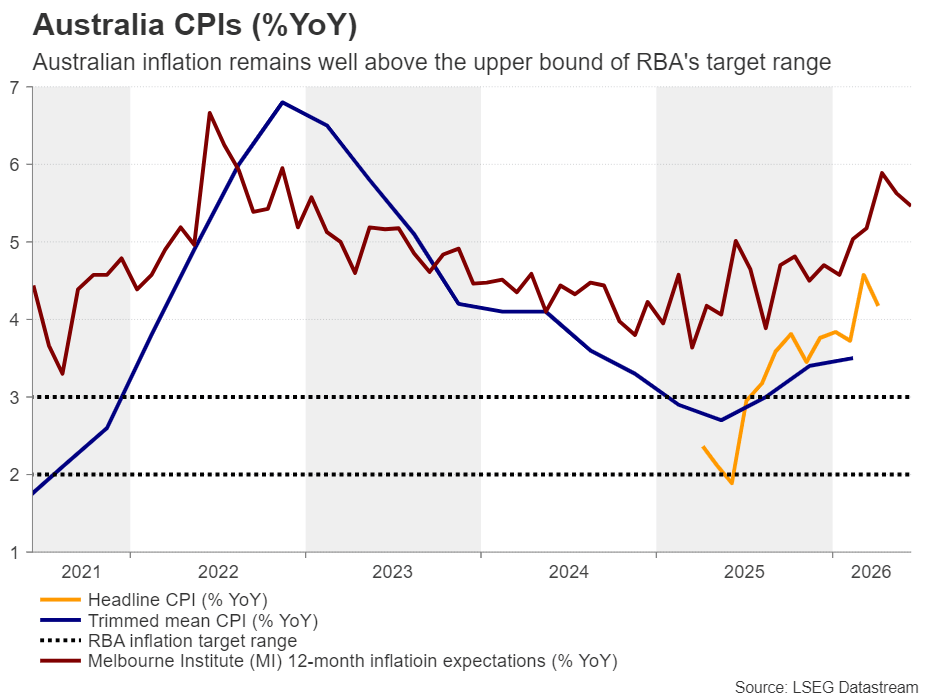

Will the RBA Keep the Door to More Hikes Open?

Soon after the BoJ, the RBA will announce its monetary policy decision. At its May meeting, the RBA decided to raise interest rates by 25bps for the third consecutive month, fully reversing the reductions made during last year. That said, the forward guidance was less hawkish than the previous ones, with policymakers not pre-committing to additional hikes and instead emphasizing data dependency.

This, combined with additional post-meeting comments by Gov. Bullock that rates are now in restrictive territory, prompted investors to bet on a pause at this gathering. On top of that, the increase in unemployment rate for April and the drop in household spending during the month added credence to the idea that the RBA may need to proceed at a slower pace from here onwards. Indeed, another 25bps rate hike is not even fully priced in by the end of the year, receiving only an 80% chance.

Having said that though, closing the door to additional rate increases may be a premature move, especially with Australian inflation remaining elevated. The headline CPI rate slowed to 4.2% y/y in April from 4.6% but remained well above the upper bound of the RBA’s 2-3% target range, while the trimmed mean rate ticked up to 3.4% y/y from 3.3%.

Therefore, with hostilities in the Middle East potentially escalating at some point and the strait of Hormuz remaining closed, the most likely outcome may be a hawkish hold that brings forward the timing of when the next rate hike may be delivered. This could prove positive for the Australian dollar.

The aussie may experience some early volatility though as ahead of the decision, China’s industrial production, fixed asset investment, retail sales and the unemployment rate, all for May will be released.

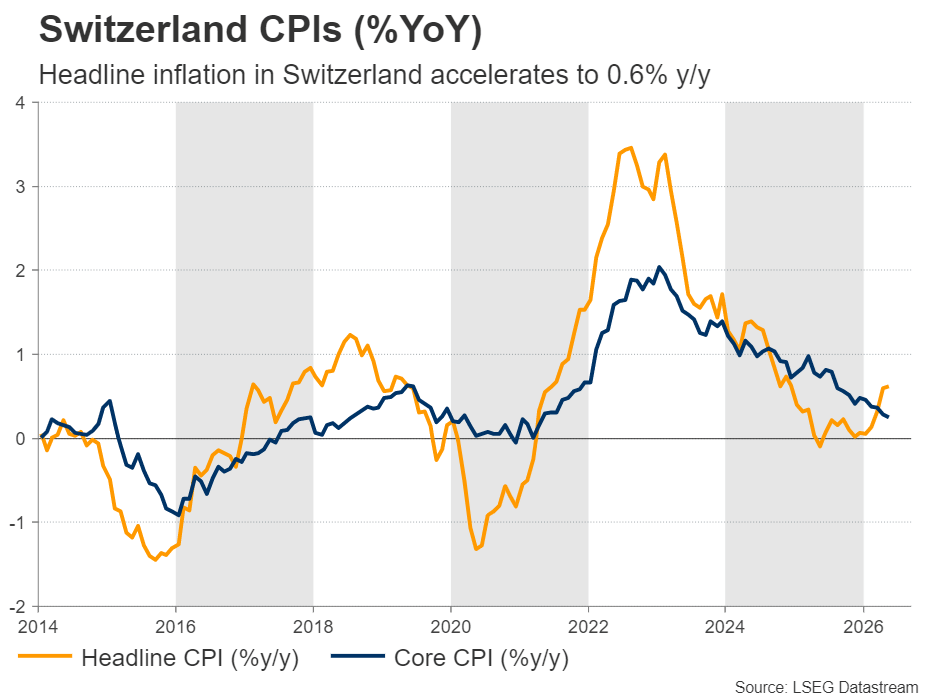

SNB to Stand Pat, Could Revise Up Inflation Projections

On Thursday, the central bank torch will be passed to the SNB and the Bank of England. Getting the ball rolling with the SNB, its latest meeting was on March 19, with the SNB keeping interest rates at 0.00% and policymakers acknowledging that inflation remained very low despite the spike in energy prices amid the Middle East conflict. They remained willing to intervene in the FX market to prevent the franc from appreciating amid increasing risk it could attract safe haven flows.

Having said all that, inflation accelerated since then, with the CPI rate rising to 0.6% in April and remaining there in May, erasing deflation fears but not raising concerns about overshooting inflation either.

This means that policymakers will be more than happy to stay sidelined once again, without having to think whether negative rates could be needed at some point. They may even revise their inflation projections higher, which could prove positive for the franc.

However, the franc has depreciated notably against the euro since then, and thus, any meeting-related spike is unlikely to trigger urgency for intervention, though officials are likely to reiterate their readiness to step into the FX market if and when deemed necessary.

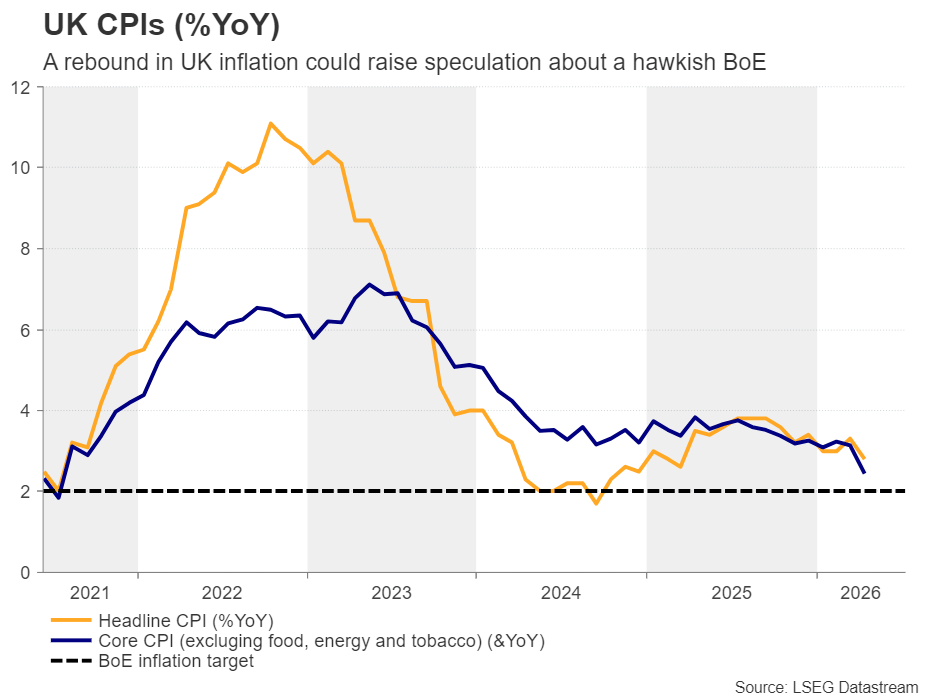

Will the BoE Reiterate Its No-Rush Mantra?

At its most recent gathering, on April 30, the BoE kept rates untouched, with the committee voting 8-1 in favor of that, with the dissenter preferring a quarter-point hike. Policymakers acknowledged that, due to the conflict in the Middle East, inflation risks have increased, but Governor Bailey most recently signaled that they are not in a rush to press the hike button and that allowing inflation to run above target is justified given the uncertainty about the impact of the Iran war on the economy.

Taking all that into account, traders are largely expecting the Bank to remain on the sidelines at next week’s gathering, with the rate-hike case receiving only an 11% probability. A 25bps rate increase is fully priced in for September and thus, investors will be looking for signals as to whether policymakers have the appetite to press the hike button sooner.

The UK CPI data for May will be out on Wednesday, and should they point to accelerating consumer prices after April’s slowdown, investors will be looking for a more hawkish message on Thursday. If they are satisfied, they could fully pencil in a rate hike for July, which could help the pound recover some ground.

The UK retail sales will be released on Friday, the day after the decision, while New Zealand’s GDP for Q1 and Canada’s retail sales are also on next week’s agenda, scheduled for Wednesday and Friday, respectively.

{kind=link}