The financial markets are mixed in Asia today as risk aversion seemed to have peaked for now. NASDAQ led US stocks decline overnight a hit as low as 7654.84 but closed down only -0.67% at 7735.95. S&P 500 also dipped to 2862.08 but closed down -0.04% at 2884.43. DOW even reversed earlier loss to close up 0.15% at 39.73. In Asia, China Shanghai SSE is up 0.49%, paring some of yesterday’s -3.7% loss. Hong Kong HSI is up 0.42%. Nikkei and Singapore Strait Times, however, are down -1.31% and -0.40% respectively.

In the currency markets, Australian Dollar is trading as the strongest one for today so far, as lifted by stabilizing Chinese stocks, as well as improvement in business confidence. Yen follows as the second strongest, which could in that risk aversion is ready to come back any time. Dollar is trading as the weakest one, as yesterday’s rally attempt failed. Swiss Franc follows as the second weakest, then Canadian.

Technically, a main focus is whether USD/JPY could draw support from 112.94. fibonacci level for rebound, or it will dip lower in sync with other yen crosses. Also, there are signs that Dollar has made temporary tops, against Euro, Aussie and Canadian. We could see some corrective trading in Dollar in near term as it digests last week’s gains.

Australian business confidence rose, ongoing strength but meek price pressures

Australian NAB Business Confidence rose to 6 in September, up from 5 and beat expectation of 5. Business Conditions rose to 15, up from 14 and beat expectation of 9.

Alan Oster, NAB Group Chief Economist noted in the release that “business conditions appear to have stabilized after declining through the middle of 2018.” Also, “despite having eased notably from the highs earlier in the year, they remain well above average, suggesting that the business environment continues to be favorable”. And, “ongoing strength in employment is especially encouraging.”

The only concern remains around “lower forward orders”. Mining again is strongest but “retail is weak and deteriorating”. And, “retail has now lagged for some time and is unlikely to turn around anytime soon with the weaker outlook for the consumer and ongoing structural changes in the sector”. Overall, the survey points to “ongoing strength in business activity” in to latter part of 2018, but “ongoing meek price pressures”.

IMF downgrades global growth forecasts as risks materialized

IMF downgraded global growth forecasts for both 2018 and 2019 as some downside risks identified earlier in April have been realized and “the likelihood of further negative shocks to our growth forecast has risen.” The risks included “rising trade barriers and a reversal of capital flows to emerging market economies”. Financial market conditions could “tighten rapidly” if trade tensions and policy uncertainty were to intensify. And, unexpectedly high inflation readings in the US could “lead investors to abruptly reassess risks”

In several key economies, “growth is being supported by policies that seem unsustainable over the long term.” IMF warned that “these concerns raise the urgency for policymakers to act.” For the US, IMF said “growth will decline once parts of its fiscal stimulus go into reverse.” Also, US forecasts were downgraded “owing to the recently enacted tariffs on a wide range of imports from China and China’s retaliation”, At the same time, China’s 2019 forecasts was also marked down. IMF also warned that “domestic Chinese policies are likely to prevent an even larger growth decline than the one we project, but at the cost of prolonging internal financial imbalances.”

- Global growth projected at 3.7% (3.9% prior) in 2018, 3.7% (3.9% prior) in 2019.

- US growth projected at 2.9% (2.9% prior) in 2018, 2.5% (2.7% prior) in 2019.

- Eurozone growth projected at 2.0% (2.4% prior) in 2018, 1.9% (2.0% prior) in 2019.

- Germany growth projected at 1.9% (2.5% prior) in 2018, 1.9% (2.0% prior) in 2019.

- Japan growth projected at 1.1% (1.2% prior) in 2018, 0.9% (2.9% prior) in 2019.

- UK growth projected at 1.4% (1.6% prior) in 2018, 1.4% (1.5% prior) in 2019.

- China growth projected at 6.6% (6.6% prior) in 2018, 6.2% (6.4% prior) in 2019.

Elsewhere

UK BRC retail sales monitor dropped -0.2% yoy in September versus expectation of 0.1% yoy. Japan current account surplus narrowed to JPY 1.43T in August versus expectation of JPY 1.52T. Germany will release trade balance in European session. Canada will release housing starts. Overall, the economic calendar is pretty light today.

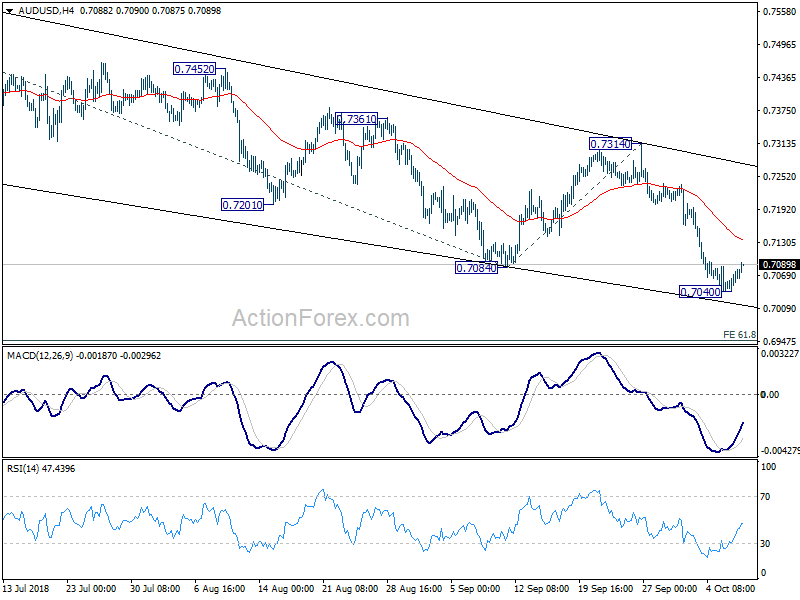

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7053; (P) 0.7068; (R1) 0.7093; More…

A temporary low should be in place at 0.7040 in AUD/USD with today’s recovery. Intraday bias is turned neutral for consolidation first. Stronger recovery could be seen to 4 hour 55 EMA (now at 0.7136). But upside should be limited well below 0.7314 resistance to bring fall resumption. Break of 0.7040 will resume whole down trend from 0.8135 to 61.8% projection of 0.7676 to 0.7084 from 0.7314 at 0.6948 next.

In the bigger picture, fall from 0.8135 is tentatively treated as resuming long term down trend from 1.1079 (2011 high). Decisive break of 0.6826 will target 0.6008 key support next (2008 low). However, break of 0.7500 support turned resistance will argue that the corrective pattern from 0.6826 is going to extend with another rising leg before completion.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:01 | GBP | BRC Retail Sales Monitor Y/Y Sep | -0.20% | 0.10% | 0.20% | |

| 23:50 | JPY | Current Account (JPY) Aug | 1.43T | 1.52T | 1.48T | |

| 0:30 | AUD | NAB Business Conditions Sep | 15 | 9 | 15 | 14 |

| 0:30 | AUD | NAB Business Confidence Sep | 6 | 5 | 4 | 5 |

| 5:00 | JPY | Eco Watchers Survey Current Sep | 47.3 | 48.7 | ||

| 6:00 | EUR | German Trade Balance (EUR) Aug | 15.9B | 15.8B | ||

| 10:00 | USD | NFIB Small Business Optimism Sep | 108.8 | |||

| 12:15 | CAD | Housing Starts Sep | 203K | 201K |

{kind=link}