Dollar is struggling to find more upside momentum in early US session except versus Swiss Franc. Solid job data is not giving the greenback the needed fuel for rally. Nonetheless, Dollar is still firm as supported by the hawkish FOMC minutes released yesterday. For now, Australian Dollar is the strongest one for today, followed by New Zealand Dollar. For Aussie, strength in iron ore prices, which jumped to highest level since March, is more then enough to offset persistent weakness in Chinese stocks. Yen is following as the third strongest one, but it’s fate will depend on risk sentiments in general.

On the other hand, Canadian Dollar is the weakest one for today. Crude oil suffered steep selloff on larger than expected inventory increase yesterday and decline continues today. WTI crude oil is back below 69 handle and the fall is accelerating. Swiss Franc is the second weakest for the moment. Sterling is the third weakest after poor retail sales data. Also, Brexit impasse is also a key factor weighing down the Pound.

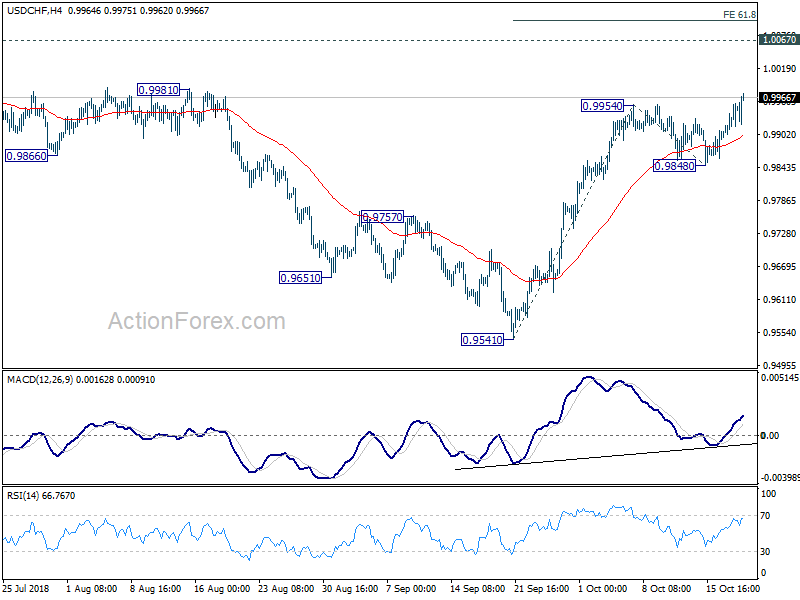

Technically, USD/CHF’s move away from 0.9954 resistances solidify the case of rise resumption for 1.0067 key resistance. EUR/USD is on track to retest 1.1431 support. But EUR/JPY will likely arrive at 129.11 support earlier. With today’s strong rebound 1.3070/81 resistance zone in USD/CAD is now in radar for US session.

In other markets, FTSE is flat at the time of writing. DAX is up 0.12% and CAC is up 0.40%. German 10 year yield is down -0.0015 at 0.463. Italian 10 year yield is up 0.0429 at 3.587. Earlier today, Nikkei dropped -0.8%, Singapore Strait Times dropped -0.05%, Hong Kong HSI dropped -0.03%. China Shanghai SSE suffered heavy selling and fell -2.94% to 2486.42, losing 2500 handle.

US initial jobless claims dropped to 210k, continuing claims dropped to lowest since 1973

US initial jobless claims dropped -5k to 210k in the week ended October 13, matched expectations. Four-week moving average of initial claims rose 2k to 211.75k. Continuing claims dropped -13k to 1.64m in the week ended October 6, lowest since August 3, 1973. Four-week moving average of continuing claims dropped -1.25k to 1.653m, lowest since August 18, 1973.

Philly Fed manufacturing index dropped 0.7 to 22.2, above expectation of 21.0

UK PM May talked about a further idea of extending the Brexit implementation period

UK Prime Minister Theresa May said today that she had already put forward on a proposal for avoiding a hard Irish border to the EU. Meanwhile, “a further idea that has emerged – and it is an idea at this stage – is to create an option to extend the implementation period for a matter of months – and it would only be for a matter of months.” But she emphasized that “this is not expected to be used, because we are working to ensure that we have that future relationship in place by the end of December 2020.”

The extension is believed to be a proposal put forward by EU’s chief negotiator Michel Barnier. Under the proposal, both sides could commit to a free trade agreement by the end of 2021. That is, a year of extension in the transition period. And, only if the FTA failed to deliver so called “frictionless” trade would the Irish backstop come into action. Barnier believed that the extension would unlock the stalled debate on Irish border backstop while there would be enough time for the trade deal.

However, the idea of extending the implementation period would catch furious responses from Brexiteers. That would effectively mean another year of EU budget payments as well as continued free movements.

UK retail sales dropped -0.8% mom, stark slowdown in food sales in September

Sterling pays little attention to weaker than expected retail sales data. Retail sales including auto and fuel came in at -0.8% mom, 3.0% yoy in September versus expectation of -0.4% mom, 3.6% yoy. Retail sales excluding auto and fuel came in at -0.8% mom, 3.2% yoy in September versus expectation of -0.4% mom, 3.8% yoy.

ONS Head of Retail Sales Rhian Murphy said in the release that “retail continued to grow in the three months to September with jewellery shops and online stores seeing particularly strong sales. This was despite a stark slowdown in food sales in September, following a bumper summer.”

German DIHK lowered GDP forecasts, big deterioration in business expectations

Germany’s DIHK Chambers of Industry and Commerce lowered 2018 growth forecasts significant from 2.2% to 1.8%. German economic growth is expected to slow further to 1.7% in 2019.

DIHK said “companies are noticeably more cautious about their business outlook, we see the biggest deterioration in business expectations in four years”. It added “given the rapid pace of change, for example in global trade policies or digitalization – and the unclear outcome of Brexit, it is becoming more difficult for companies to foresee a clear trend in their business development,”

In the survey titled “the air is getting thinner” business expectations dropped sharply to 11, down from 17. Current situation was unchanged at 25 though.

BoJ Kuroda: consumer inflation moving around 1 percent

BoJ Governor Haruhiko Kuroda offered a slightly more upbeat view on inflation today, in a quarterly meeting with regional branch managers. He said that consumer inflation was “moving around 1 percent”. That compared to the wordings of moving around 0.5 to 1 percent three months ago. On the economy, Kuroda maintained that it’s “expected to continue expanding moderately”. On monetary policy, Kuroda reiterated that “the BOJ will make necessary policy adjustments to sustain the economy’s momentum to achieve the price target … while looking at risks that warrant attention.”

Released from Japan, trade deficit widened to JPY -0.24T in September, smaller than expectation of JPY -0.34T.

Australia unemployment dropped to 5%, lowest since 2012, as labor force contracted

Australia unemployment dropped sharply to 5.0% in September, down from prior 5.3% and beat expectation of 5.3%. However, it should also be noted that participation rate also dropped -0.2% to 65.4%. So, the drop in unemployment rate was more a reflection of decline in the size of labor force. Employment grew 5.6k versus expectation of 15.2k. Full-time jobs rose 20.3k to 8.65m. But part time jobs dropped -14.7k to 3.98m.

Australia NAB business confidence dropped to 3, inflationary pressures meek

Australia NAB business confidence dropped to 3 in Q3, down from Q2’s 7. Current business condition dropped to 13, down from 15. NAB noted that “though conditions remain well above average; confidence is now below average”. Meanwhile, “surveyed price and wage variables suggest at present inflationary pressures remain weak.”

On RBA monetary policy, NAB noted that markets are pricing in around 90% chance of a 25bps rate hike in the next 12-months. Pricing increased from 70% back in Q2. NAB’s own view is that “RBA will likely begin a gradual series of rate rises in mid-to-late 2019 but that this is highly data dependent.” NAB saw “inflationary pressures best described as meek at present.”

On exchange rate, NAB revised down its own forecasts on AUD/USD to “closer to US$0.70” as “global trade ructions continue to weigh.”

US Treasury not naming China as currency manipulator despite lack of transparency

US Treasury refrained from naming China a currency manipulator in the latest “Macroeconomic and Foreign Exchange Policies of Major Trading Partners of the United States” report.

In a statement, Treasury Secretary Seven Mnuchin said the department is “working vigorously to ensure that our trading partners dismantle unfair barriers that stand in the way of free, fair, and reciprocal trade.” And he singled out China as of “particular concern” due to the “lack of currency transparency and the recent weakness in its currency”. Mnuchin added that they will continue to “monitor and review” China’s currency practices.

The statement also noted that despite the lack of transparency, “Treasury estimates that direct intervention by the People’s Bank of China this year has been limited.” Though, it also warned that “recent depreciation of the renminbi will likely exacerbate China’s large bilateral trade surplus with the United States”. It placed ” significant importance” on ensuring China doesn’t engage in “competitive devaluation”.

A total of six major trading partners are put in the monitoring list, including China, Germany, India, Japan, Korea, and Switzerland.

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9915; (P) 0.9935; (R1) 0.9972; More…

USD/CHF’s rally continues today and reaches as high as 0.9975 so far. Intraday bias stays on the upside at this point. Current rise from 0.9541 should target 1.0067 key resistance and then 61.8% projection of 0.9541 to 0.9954 from 0.9848 at 1.0103. On the downside, break of 0.9848 support is needed to indicate short term topping. Otherwise, further rally will be expected even in case of retreat.

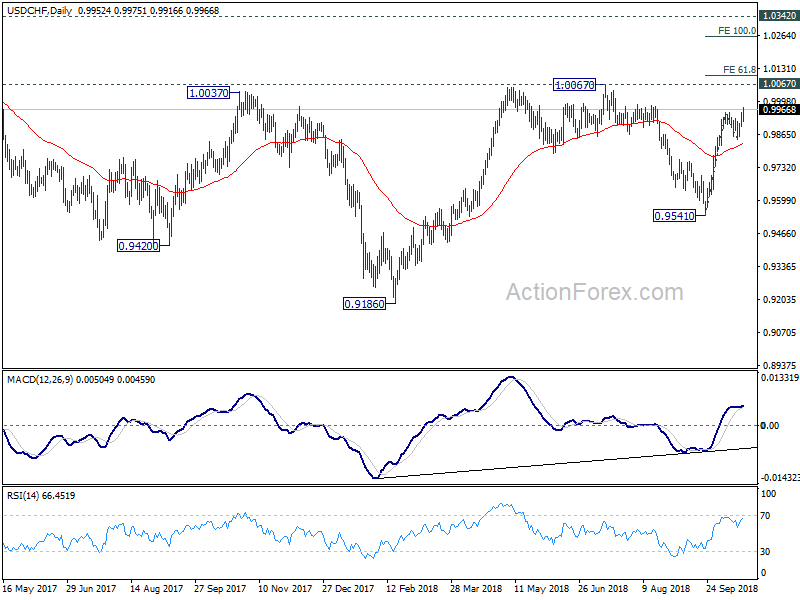

In the bigger picture, the pullback from 1.0067 has completed at 0.9541 already. And rise from 0.9186 is likely resuming. Firm break of 1.0067 will pave the way to retest 1.0342 key resistance. We’d be cautious on strong resistance from there to limit upside to bring another medium term fall to extend long term range trading.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Trade Balance (JPY) Sep | -0.24T | -0.34T | -0.19T | |

| 00:30 | AUD | Employment Change Sep | 5.6K | 15.2K | 44.0K | 44.6K |

| 00:30 | AUD | Unemployment Rate Sep | 5.00% | 5.30% | 5.30% | |

| 00:30 | AUD | NAB Business Confidence Q3 | 3 | 7 | ||

| 06:00 | CHF | Trade Balance (CHF) M/M Sep | 2.43B | 2.45B | 2.13B | 2.08B |

| 08:30 | GBP | Retail Sales M/M Sep | -0.80% | -0.30% | 0.30% | |

| 12:30 | CAD | ADP Payrolls Report | 28.8K | 13.6K | ||

| 12:30 | USD | Philly Fed Manufacturing Index Oct | 22.2 | 21 | 22.9 | |

| 12:30 | USD | Initial Jobless Claims (OCT 13) | 210K | 210K | 214K | 215K |

| 14:00 | USD | Leading Index Sep | 0.40% | |||

| 14:30 | USD | Natural Gas Storage | 90B |

x

{kind=link}