Canadian Dollar suffers heavy selling in early US session as the large deceleration in CPI to 2.2% raising doubts on whether BoC would still hike next week. Meanwhile Yen and Swiss Franc are among the weakest ones. Widening of German-Italian spread is not translated into selloff in European stocks nor any meaningful movements in the forex markets. New Zealand Dollar and Australian Dollar are the strongest ones, with help from reversal in Chinese stocks despite GDP miss.

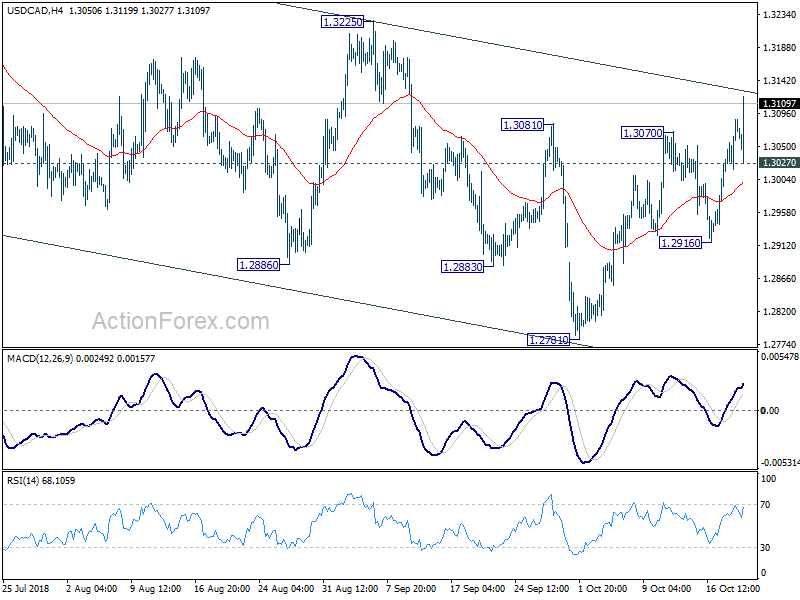

Technically, USD/CAD’s strong break of 1.3081 resistance is taken as a solid sign of bullish trend reversal. Focus is turned to 1.3225 resistance for confirmation. Euro is consolidating above yesterday’s low against Dollar and Yen. While there is no extended selloff in Euro, it remains technically vulnerable for another fall. AUD/USD, despite today’s rebound is still holding in tight range below 0.7159 temporary top.

In Europe, FTSE is trading up 0.37%, DAX is down -0.16% and CAC is down -0.66%. German 10 year yield is down -0.005 at 0.416. Italian 10 year yield is up 0.059 at 3.737. That is, German-Italian yield spread is now above 330.

In Asia, Chinese stocks staged a strong rebound after initial selloff. The Shanghai SSE dipped to 2449.20 but ended up 0.26% at 2550.47, reclaiming 2500 handle. Hong Kong HSI was also lifted and rose 0.42% to 25561.40. However, Singapore Strait Times fell -0.23% while Nikkei lost -0.56%. Japan 10 year JGB yield dropped -0.0044 to 0.151.

Canadian Dollar dives notably after a set of much weaker than expected data.

Headline retail sales dropped -0.1% mom in August versus expectation of 0.4% mom. Ex-auto sales dropped -0.4% mom versus expectation of -0.2% mom.

Headline CPI dropped sharply by -0.4% mom in September versus expectation of -0.1% mom. Annually, CPI slowed to 2.2% yoy, down from 2.8% yoy and missed expectation of 2.9% yoy.

CPI core common slowed to 1.9% yoy, down from 2.0% yoy. CPI core median slowed to 2.0% yoy, down from 2.1% yoy. CPI core trim slowed to 2.1% yoy, down from 2.2% yoy.

The set of data, in particular the sharp fall in CPI, raises the important question of whether BoC is still going to hike next week on October 24.

EU: Italy’s budget an obvious significant deviation of Stability and Growth Pact

EU Commissioners Valdis Dombrovskis and Pierre Moscovici wrote a joint letter to warn Italy of its budget plan. Handing the letter directly to Italian Economy Minister Giovanni Tria, the EU started the first formal step to reject the budget which will lead to direct clash between Rome and Brussels. Italy will now have until October 22 to respond to the letter.

EU said in the letter that Italy’s plan is an “obvious significant deviation” of the recommendations adopted by the European Council under the 2019 Stability and Growth Pact. Also, while the Council suggested fiscal adjustment, the Italy plans fiscal expansion of close to 1% of GDP, and the “size of the deviation (a gap of around 1.5% of GDP) are unprecedented”.

EU also criticized that the macroeconomic forecasts under the plan has not been endorsed by the Parliamentary Budget Office. And this appears “not to respect” the rules of having forecasts produced or endorsed by an “independent body”.

Released in European session, Eurozone current account surplus widened to EUR 23.9B in August. UK Public sector net borrowing dropped to GBP 3.3B in September.

China Q3 GDP slowed to 6.5%, slowest since Q1 2009

China’s economic growth decelerated further in 3Q18, as the impacts of restraining infrastructure investment and trade war surfaced. GDP growth moderated to 6.5% yoy in the third quarter, the slowest since the first quarter of 2009. Growth came in lower than market expectations and second quarter’s 6.7%. On an annualized basis, GDP eased to 5.9% qoq, from 6.4% in 2Q18 and 7.2% in 1Q18.

Statistics bureau spokesman Mao Shengyong said China is still able to reach the full-year growth target of around 6.5% in 2018 even though downward pressure increases. He added that infrastructure investment growth will stabilize and “consumption upgrade” will continue. Nonetheless, Mao also admitted that external environment will pose uncertainties on stabilizing growth.

Also released, industrial production grew 5.8% yoy in September, down from 6.1% and missed expectation of 6.0% yoy. But retail sales rose 9.2% yoy, up from 9.0% yoy and beat expectation of 9.0% yoy. Fixed asset investment rose 5.4% ytd yoy, up from 5.3% ytd yoy and beat expectation of 5.3% ytd yoy.

More on China in China’s Economic Growth Slowed More than Expected. Worst of Trade War Yet to Come

Also released in Asian session, Japan national CPI core accelerated to 1.0% yoy in September, up from 0.9% yoy and matched expectations.

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.3036; (P) 1.3063; (R1) 1.3112; More…

USD/CAD’s rally extends to as high as 1.3119 so far today. The strong break of 1.3081 resistance is taken as first sign of completion of whole choppy fall from 1.3385. Intraday bias remains on the upside for 1.3225 resistance to confirm this bullish case. Decisive break there will pave the way to retest 1.3385 high. On the downside, below 1.3027 minor support will turn intraday bias neutral first. But as long as 1.2916 support holds, further rally will remain mildly in favor in case of retreat.

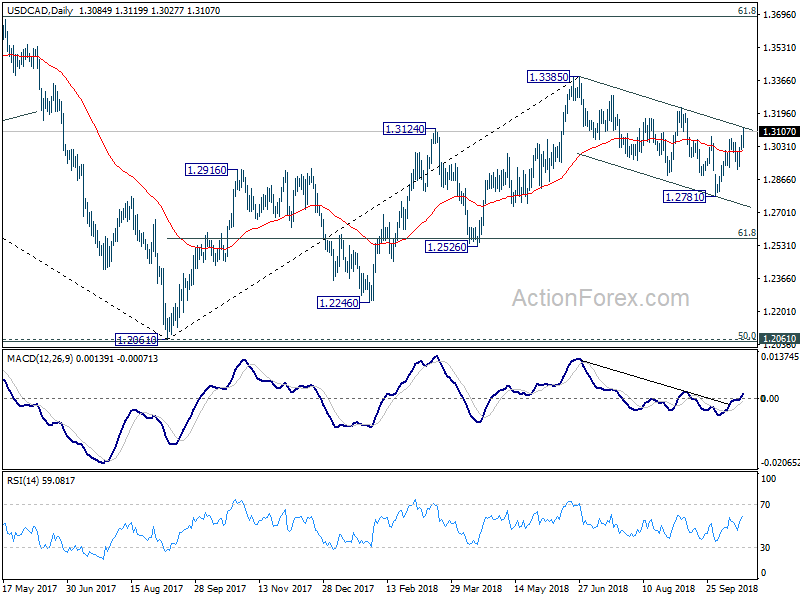

In the bigger picture, current development argues that choppy corrective fall from 1.3385 has completed at 1.2781 already. And that in turns suggests that the up trend from 1.2061 is still in progress. Decisive break of 1.3385 will pave the way to 61.8% retracement of 1.4689 to 1.2061 at 1.3685. On the downside, though, break of 1.2916 support will likely extend the fall fro 1.3385 to 61.8% retracement of 1.2061 to 1.3385 at 1.2567 before completion.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | National CPI Core Y/Y Sep | 1.00% | 1.00% | 0.90% | |

| 02:00 | CNY | GDP Y/Y Q3 | 6.50% | 6.60% | 6.70% | |

| 02:00 | CNY | Retail Sales Y/Y Sep | 9.20% | 9.00% | 9.00% | |

| 02:00 | CNY | Industrial Production Y/Y Sep | 5.80% | 6.00% | 6.10% | |

| 02:00 | CNY | Fixed Assets Ex Rural YTD Y/Y Sep | 5.40% | 5.30% | 5.30% | |

| 08:00 | EUR | Eurozone Current Account (EUR) Aug | 23.9B | 21.4B | 21.3B | 19.5B |

| 08:30 | GBP | Public Sector Net Borrowing Sep | 3.3B | 4.6B | 5.9B | 4.8B |

| 12:30 | CAD | Retail Sales M/M Aug | -0.10% | 0.40% | 0.30% | 0.20% |

| 12:30 | CAD | Retail Sales Ex Auto M/M Aug | -0.40% | -0.20% | 0.90% | 0.80% |

| 12:30 | CAD | CPI M/M Sep | -0.40% | -0.10% | -0.10% | |

| 12:30 | CAD | CPI Y/Y Sep | 2.20% | 2.90% | 2.80% | |

| 12:30 | CAD | CPI Core – Common Y/Y Sep | 1.90% | 2.00% | ||

| 12:30 | CAD | CPI Core – Median Y/Y Sep | 2.00% | 2.10% | ||

| 12:30 | CAD | CPI Core – Trim Y/Y Sep | 2.10% | 2.20% | ||

| 14:00 | USD | Existing Home Sales Sep | 5.31M | 5.34M |

{kind=link}