Sterling remains strong in general today, next to Australian and New Zealand Dollar. UK and EU officials came out dismissing the news regarding a Brexit financial services deal. But that didn’t harm the Pound a bit. Instead, Sterling ignore weak manufacturing data and is supported by slightly more confidence BoE economic projections. On the other hand, Dollar and Yen are the weakest ones. In particular, Dollar suffers deep and steep pull back with EUR/USD’s rebound from 1.1300 spilling over to other pairs. The greenback will need to look into tomorrow’s non-farm payroll report for savior.

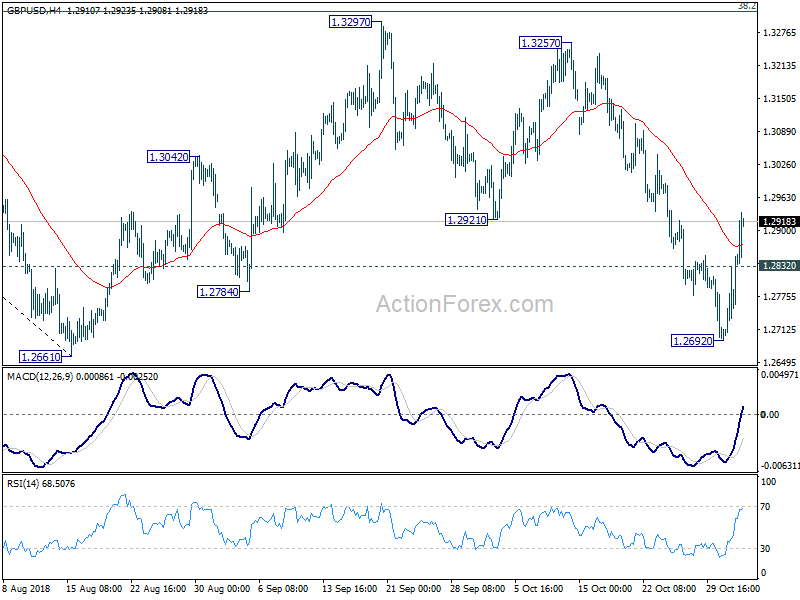

Technically, GBP/USD’s breach of 1.2921 resistance now serves as a sign of near term reversal. More upside could be seen back towards 1.3297 resistance. AUD/USD’s break of 0.7159 resistance is an early sign of medium term reversal, followed EUR/AUD’s break of 1.5984 support yesterday. Now it’s time for EUR/USD to break 1.1421 resistance to provide more evidence for a broad based Dollar reversal.

In other markets, European indices are mixed. At the time of writing, FTSE is up 0.06%, DAX up 0.26% but CAC is down -0.17%. German 10 year yield rises 0.0253 to 0.414, back above 0.4 handle. Italian 10 year yield drops -0.0691 to 3.363. That is, German-Italian spread is now back below 300. In Asia, Nikkei dropped sharply by -1.06% to close at 21687.65. But Hong Kong HSI, China Shanghai SSE and Singapore Strait Times recorded 1.75%, 0.13% and 1.39% gains respectively.

US initial jobless claims dropped to 214k, 4-week average at lowest since 1973

US initial jobless claims dropped -2k to 214k in the week ended October 27, slightly above expectation of 213k. Four-week moving average of initial claims rose 1.75k to 213.75k. Continuing claims dropped -7k to 1.631m in the week ended October 20, lowest since July 28, 1973. Four-week moving average of continuing claims dropped -6.25k to 1.62725m, lowest since August 11, 1973.

Also from the US, non-farm productivity rose 2.2% in Q3, unit labor costs rose 1.2%.

UK and EU officials dismiss misleading news on Brexit financial services deal

Earlier today, Sterling was boosted as the Times reported that a tentative deal is agreed between UK and the EU on all aspects of a future partnership on services. Most importantly, that would grant access of EU markets to for British financial services companies. However, the news was dismissed by both EU and UK officials.

EU chief Brexit negotiator Michel Barnier said in a tweet that EU is “ready” to have “close regulatory dialogue” with the UK. However, the report regarding UK banks’ access to the single market was “Misleading press articles today on #Brexit & financial services.” The UK government also said in an email statement that “While we continue to make good progress agreeing new arrangements for financial services, negotiations are ongoing and nothing is agreed until everything is agreed.”

BoE Bank Rate projections show more confidence on 2019 rate hike, but outlook depends significantly on Brexit

BoE left Bank Rate unchanged at 0.75% as widely expected. The asset purchase target was also held unchanged at GBP 435B. Both decisions were made by 9-0 unanimous vote. In the accompanying statement, BoE warned that the economic outlook will “depend significantly on the nature of EU withdrawal, in particular the form of new trading arrangements, the smoothness of the transition to them and the responses of households, businesses and financial markets.” And more importantly, “monetary policy response to Brexit, whatever form it takes, will not be automatic and could be in either direction.”

For now, though, the MPC judged that current monetary policy stance “remained appropriate”. And, “an ongoing tightening of monetary policy over the forecast period would be appropriate to return inflation sustainably to the 2% target at a conventional horizon. Though, “future increases in Bank Rate are likely to be at a gradual pace and to a limited extent.”

In the updated economic projections in the Inflation Report, BoE lowered 2019 Q4 four-quarter GDP forecasts from 1.8% to 1.7%. For 2020, four-quarter GDP forecast was kept unchanged at 1.7%. On CPI inflation, BoE lowered CPI forecast for 2019 Q4 to 2.1% from 2.2%. However, for 2020 Q4, inflation forecast was raised to 2.1% from 2.0%. Bank Rate forecasts for 2019 Q4 was raised from 0.9% to 1.0%. For 2020, Bank Rate forecasts was also raised from 1.1% to 1.2%.

In short, the economic outlook was actually largely unchanged. Nonetheless, BoE is now more certain on a rate hike in 2019, and probably another one in 2020. Indeed, from the conditioning path that BoE used, the next rate hike is pulled ahead from Q1 2020 to Q4 2019. And, another rate could even but seen in between Q3 2020 and Q1 2021.

UK PMI manufacturing dropped to 51.1, worrying turnaround

UK PMI manufacturing dropped to 51.1. in October, down from 53.8, missed expectation of 53.0. Market noted that “new orders and employment decline for first time in 27 months” Also, “input cost and output price inflation both ease”.

Rob Dobson, Director at IHS Markit noted that “”October saw a worrying turnaround in the performance of the UK manufacturing sector. At current levels, the survey indicates that factory output could contract in the fourth quarter, dropping by 0.2%.” Also, confidence remained low in H2 of the year, “with views on prospects darkening again in October amid rising Brexit-related uncertainties and escalating global trade tensions.”

Also released in European session, Swiss PMI manufacturing dropped to 57.4 in October, down fro 59.7 and missed expectation of 58.5. Swiss CPI accelerated to 1.1% yoy in October, up from 1.0% yoy and matched expectations. Swiss SECO consumer confidence improved to -6 in October.

Italian PM Conte: No exchange of concession with EU on budget talks

Italian Prime Minister Giuseppe Conte warned in a newspaper interview that it’s “unreasonable and profoundly unfair” to blame the current government for weak economic data. He referred to GDP data released on Tuesday which showed 0% growth in Q3. Also, Conte emphasized that budget talk with EU will not be an “exchange of concession”. He insist on sticking to the deficit target of 2.4% of GDP in 2019 despite EU rejection.

Indeed, Conte also said earlier this week that the weak economic performance is the reason for the “expansionary budget”. This was echoed by Deputy Prime Minister Matto Salvini who said “the slowing GDP is another reason to go full steam ahead with the budget.”

China Caixin PMI manufacturing: Economy has not seen obvious improvement

China Caixin PMI manufacturing rose 0.1 to 50.1 in October, matched expectations. Markit noted there was only “marginal increase in total new work amid further drop in export sales”. Dr. Zhengsheng Zhong, Director of Macroeconomic Analysis at CEBM Group said, “Overall, expansion across the manufacturing sector was still weak. Production and business confidence continued to cool despite stable demand. The pressure on production costs didn’t ease. China’s economy has not seen obvious improvement.”

Also released in Asian session, Australia AiG Performance of Manufacturing index dropped to 58.3, seasonally adjusted, in October, down from 59.0. Australia trade surplus widened to AUD 3.02B in September. Japan PMI manufacturing was finalized at 52.9 in October

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2698; (P) 1.2765; (R1) 1.2833; More…

GBP/USD’s rebound from 1.2692 extends higher today but it’s limited below 1.2921 support turned resistance. Intraday bias stays neutral first. As long as 1.2921 holds, near term outlook stays cautiously bearish and another decline is in favor. On the downside, break of 1.2692 will target 1.2661 low first. Decisive break there will resume larger down trend from 1.4376. Next target is 61.8% projection of 1.4376 to 1.2661 from 1.3297 at 1.2237. However, break of 1.2921 should extend the consolidation pattern from 1.2661 with another rise towards 1.3297 resistance before completion.

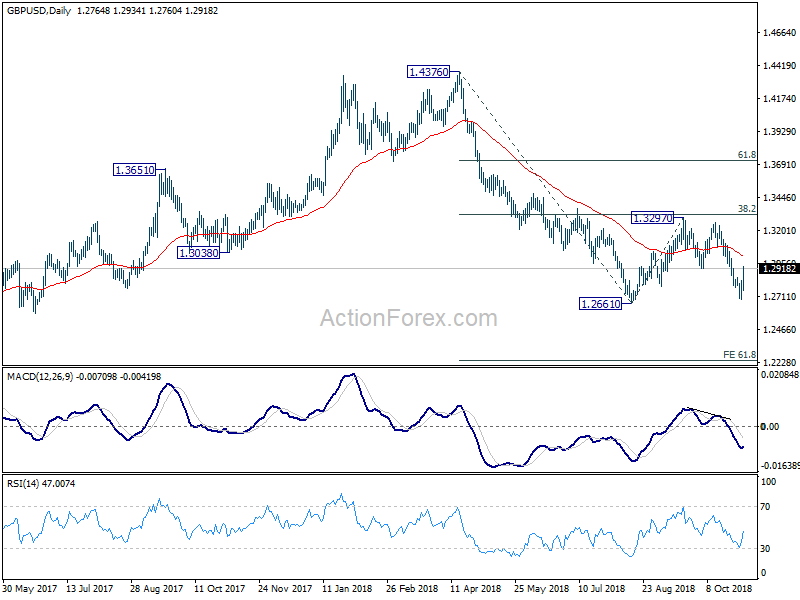

In the bigger picture, whole medium term rebound from 1.1946 (2016 low) should have completed at 1.4376 already, after rejection from 55 month EMA. The structure and momentum of the fall from 1.4376 argues that it’s resuming long term down trend. And this will be the preferred case as long as 38.2% retracement of 1.4376 to 1.2661 at 1.3316 holds. However, firm break of 1.3316 would bring stronger rebound to 61.8% retracement at 1.3721. And, the eventual depth of the fall from 1.4376, and the chance of hitting 1.1946 low, will depend on the strength of the interim corrective rebound from 1.2661.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:30 | AUD | AiG Performance of Manufacturing Index Oct | 58.3 | 59 | ||

| 00:30 | JPY | PMI Manufacturing Oct F | 52.9 | 53.1 | ||

| 00:30 | AUD | Trade Balance (AUD) Sep | 3.02B | 1.71B | 1.60B | 2.34B |

| 01:45 | CNY | Caixin PMI Mfg Oct | 50.1 | 50.1 | 50 | |

| 06:45 | CHF | SECO Consumer Confidence Oct | -6 | -8 | -7 | |

| 08:15 | CHF | CPI M/M Oct | 0.20% | 0.20% | 0.10% | |

| 08:15 | CHF | CPI Y/Y Oct | 1.10% | 1.10% | 1.00% | |

| 08:30 | CHF | PMI Manufacturing Oct | 57.4 | 58.5 | 59.7 | |

| 09:30 | GBP | PMI Manufacturing Oct | 51 | 53 | 53.8 | 53.6 |

| 11:30 | USD | Challenger Job Cuts Y/Y Oct | 153.60% | 70.90% | ||

| 12:00 | GBP | BoE Bank Rate | 0.75% | 0.75% | 0.75% | |

| 12:00 | GBP | BoE Asset Purchase Target | 435B | 435B | 435B | |

| 12:00 | GBP | MPC Official Bank Rate Votes | 0–0–9 | 0–0–9 | 0–0–9 | |

| 12:00 | GBP | MPC Asset Purchase Facility Votes | 0–0–9 | 0–0–9 | 0–0–9 | |

| 12:00 | GBP | BoE Inflation Report | ||||

| 12:30 | USD | Nonfarm Productivity Q3 P | 2.20% | 2.00% | 2.90% | |

| 12:30 | USD | Unit Labor Costs Q3 P | 1.20% | 1.10% | -1.00% | |

| 12:30 | USD | Initial Jobless Claims (OCT 27) | 214K | 213K | 215K | 216K |

| 13:30 | CAD | Manufacturing PMI Oct | 54.8 | |||

| 13:45 | USD | Manufacturing PMI Oct F | 55.9 | 55.9 | ||

| 14:00 | USD | Construction Spending M/M Sep | 0.20% | 0.10% | ||

| 14:00 | USD | ISM Manufacturing Oct | 59 | 59.8 | ||

| 14:00 | USD | ISM Prices Paid Oct | 67.5 | 66.9 | ||

| 14:00 | USD | ISM Employment Oct | 58.8 | |||

| 14:30 | USD | Natural Gas Storage | 53B | 58B |

{kind=link}