Sterling stages a broad based rebound today despite poor PMI services data. The Pound is partly helped by technical support from GBP/USD (at 1.2661) and EUR/GBP (at 0.8939). Additionally, traders are probably reassessing Brexit scenarios. A tricky point is on what would Common’s rejection of Prime Minister Theresa May’s Brexit deal lead to. One far fetched possibility is UK unilaterally withdrawing Brexit request. The ongoing Brexit debate in the parliament, and speculations ahead of December 11 vote might limit downside of the Pound for the moment.

Meanwhile, Euro follows as the second strongest on positive development in Italy. While nothing concrete has been delivered, it seems that Italy is working “intensely” with European Commission to revise its 2019 budget plan. Words from the coalition government are so far affirmative. German-Italian spread drops to around 280, suggesting acceptance by investors. Australian Dollar is currently the worst performing one after weak GDP data. Yen is the second weakest as there is no intensification in risk aversion.

Technically, most pairs are bounded in rather narrow range without any significant development. EUR/USD is staying in 1.1267/1472. GBP/USD recovers after hitting 1.2661 but upside is limited well below 1.2927 minor resistance. USD/CHF fails 1.0006 resistance again but it’s holding above 0.9908. USD/CAD is also holding in range of 1.3160/3359 despite strong rebound.

In other markets, major European indices are trading in red but losses are limited. FTSE is down 1.02%, DAX down -0.68%, CAC down -0.76%. German 10 year yield is up 0.0125 at 0.276. Italian 10 year yield is down -0.629 at 3.086. Earlier today, Nikkei closed down only -0.53% after paring much of earlier losses. Singapore Strait Times dropped -0.37%. Hong Kong HSI and China Shanghai SSE lost -1.62% and -0.61% respectively.

Focus will turn to BoC rate decision. And the central bank is widely expected to keep interest rate unchanged at 1.75%.

UK PMI services dropped to 28-month low, sharp deterioration in service sector growth

UK PMI services dropped notably to 50.4, down from 52.2 and missed expectation of 52.5. That’s also the lowest reading in 28 months. Markit noted there is only marginal expansion of overall business activity. Employment growth moderates to four-month low. And, business optimism is weakest since July 2016.

Chris Williamson, Chief Business Economist at IHS Markit, noted in the release that “a sharp deterioration in service sector growth leaves the economy flatlining in November as Brexit concerns intensified”. And, the PMI surveys are consistent with merely 0.1% GDP growth in Q3, “thanks to the expansion seen back in October”. And he warned that “growth momentum has since been lost and risks are clearly tilted to the downside.”

Eurozone PMI composite finalized at lowest since Sep 2016, Germany the center of slowdown

Eurozone PMI services was finalized at 53.4, revised up from 53.1 down slightly from October final of 53.7. PMI composite was finalized at 52.7, down from October’s 53.1. That’s the lowest level since September 2016.

Among the countries, Germany PMI composite dropped to 52.3, hitting 47 month low. Markit noted that “It was in Germany where the euro area’s growth slowdown was centred, with latest data showing the weakest expansion here in nearly four years.”

Williamson at Markit noted that the PMIs point to “modest GDP growth of approximately 0.3% in the fourth quarter, suggesting the region remains stuck in a soft-patch.” And, “hardest hit has been Italy” suggesting “the economy is on course to contract again in the fourth quarter”, Also, “with Germany reporting the weakest growth for nearly four years, the survey raises question marks about the extent to which GDP will rebound in the fourth quarter.”

Italy PM Conte will tweak budget without backtracking

Italian Prime Minister Giuseppe Conte was quoted by la Repubblica daily that “if I have the chance to reduce the economic impact of some measures I’m here.” He added, “I’m the one who is entitled to speak with the European Commission … and I never halted discussions. Right now if I can recover some funds, tweak the final figure, change a few little things, it doesn’t mean I’m backtracking.”

European Budget Commissioner Guenther Oettinger repeated the urge for Italy to comply with EU rules. He said in a German radio interview that “We hope that a draft will come today that corresponds to the criteria for all euro countries”. But he sounded tough and indicated that even bring down deficit target from the current plan’s 2.4% to 2.2% of GDP, that “would be against all the commitments”.

BoJ Wakatabe: Inflation only halfway to target, may revert to deflation

BoJ Deputy Governor Masazumi Wakatabe said today that the first characteristic of the current economy is it’s being “widespread”. And it’s “bring about benefits to a wide range of economic entities.” And, the second characteristic is that “inflation rate turning positive”, “which is different from the case in the mid-2000s”.

On outlook, he reiterated the bank’s rhetorics that the economy is expected to continue on an “expanding trend”. But he also noted various risks including US-China trade friction. On prices, he said CPI is likely to “increase gradually” as the economic expansion continues.

Though, Wakatabe also warned that for now, inflation remained at around 1%, “only halfway” to 2% target. And, “in a case where downward pressure is exerted on the economy again, it may revert to deflation. Thus, it’s appropriate to continue with the “large-scale monetary easing”.

Australia GDP grew merely 0.3% in Q3, Aussie pressured broadly

Australia GDP grew merely 0.3% qoq in Q3, just half of expectation of 0.6% qoq. That’s also a sharp slow down from Q2’s 0.90%. On annual basis, GDP growth slowed to 2.8% yoy, well below expectation of 3.4% yoy. In November Monetary Policy Statement, RBA projected GDP growth to be at 3.5% in 2018. And it’s now highly likely to miss such projection. Based on the steep slowdown in momentum, it’s getting doubtful if 2019 forecast of 3.25% growth would be met. And, RBA might need to revise down its projections in the next MPS in February. But after all, the slowdown will firm up the case for RBA to continue to stand pat throughout 2019, and probably deeper into 2020.

Also from Australia, AiG performance of services index rose to 55.1, up from 51.1. From China, Caixin PMI services rose to 53.8, up from 50.8 and beat expectation of 50.8.

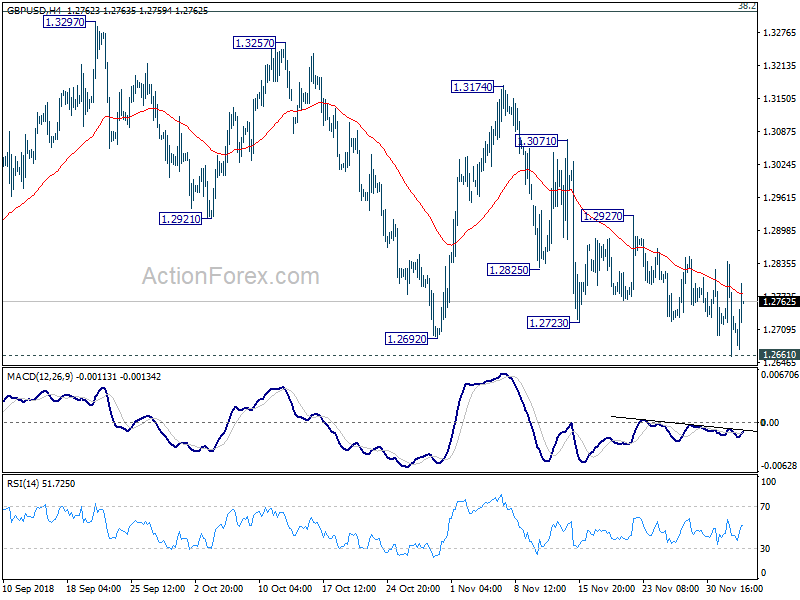

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2636; (P) 1.2738; (R1) 1.2817; More…

GBP/USD breached 1.2661 briefly but quickly recovered. Intraday bias is turned neutral again. On the downside, sustained break of 1.2661 low will resume larger down trend from 1.4376. Next target will be 1.1946. On the upside, break of 1.2927 will extend the consolidation from 1.26661 with another rise. But even in case of strong rebound, upside should be limited by 1.3316 fibonacci level to bring down trend resumption eventually.

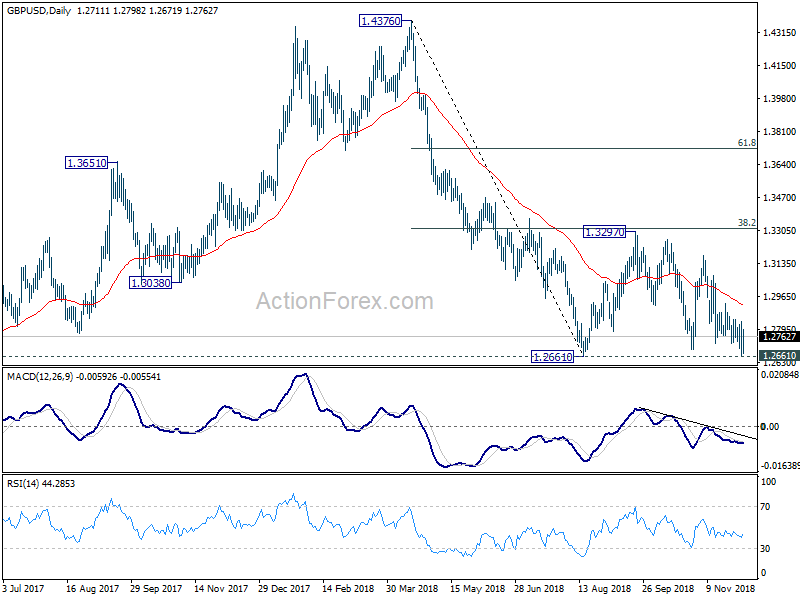

In the bigger picture, whole medium term rebound from 1.1946 (2016 low) should have completed at 1.4376 already, after rejection from 55 month EMA. The structure and momentum of the fall from 1.4376 argues that it’s resuming long term down trend. And this will be the preferred case as long as 38.2% retracement of 1.4376 to 1.2661 at 1.3316 holds. However, firm break of 1.3316 would bring stronger rebound to 61.8% retracement at 1.3721. And, the eventual depth of the fall from 1.4376, and the chance of hitting 1.1946 low, will depend on the strength of the interim corrective rebound from 1.2661.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:30 | AUD | AiG Performance of Service Index Nov | 55.1 | 51.1 | ||

| 0:30 | AUD | GDP Q/Q Q3 | 0.30% | 0.60% | 0.90% | |

| 0:30 | AUD | GDP Y/Y Q3 | 2.80% | 3.30% | 3.40% | 3.10% |

| 1:45 | CNY | Caixin PMI Services Nov | 53.8 | 50.8 | 50.8 | |

| 8:45 | EUR | Italy Services PMI Nov | 50.3 | 49.2 | 49.2 | |

| 8:50 | EUR | France Services PMI Nov F | 55.1 | 55 | 55 | |

| 8:55 | EUR | Germany Services PMI Nov F | 53.3 | 53.3 | 53.3 | |

| 9:00 | EUR | Eurozone Services PMI Nov F | 53.4 | 53.1 | 53.1 | |

| 9:30 | GBP | Services PMI Nov | 50.4 | 52.5 | 52.2 | |

| 10:00 | EUR | Eurozone Retail Sales M/M Oct | 0.30% | 0.20% | 0.00% | -0.50% |

| 15:00 | CAD | BoC Rate Decision | 1.75% | 1.75% | ||

| 19:00 | USD | Fed’s Beige Book |

{kind=link}