European majors are trading generally higher today, as led by Swiss Franc. Euro is also strong but to a lesser extend while Sterling just follows. On the other hand, Dollar is under some selling pressure, in particular after much weaker than expected manufacturing. It’s yet another piece of data that points to slow down in the US. But for now, loss in the greenback is still limited, as traders are cautious ahead of FOMC rate decision, statement, and economic projections to be released on Wednesday.

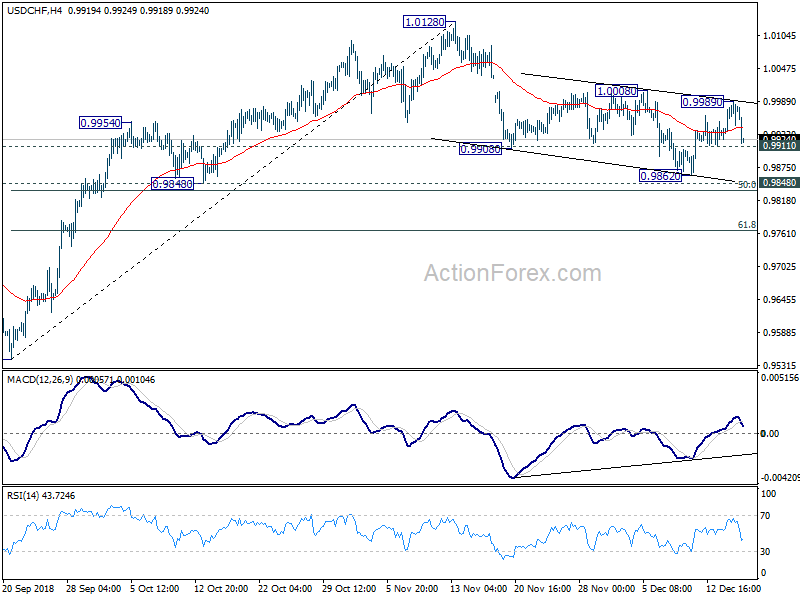

Technically, though, today’s sharp fall in USD/CHF suggests that rebound from 0.9862 has possibly completed at 0.9989. 0.9911 minor support is now in focus and break will probably extend the correction from 1.0128 with another taken on 0.9484 key support. Meanwhile, USD/JPY’s pull back from 113.70 is also extending lower and on acceleration it would head back to 112.23 support.

In other markets, major European indices are all trading in red at the time of writing. FTSE is down -0.69%, DAX is down -0.94% and CAC is down -0.85%. German 10 year bund yield is up 0.010 at 0.258. Italian 10 year yield is up 0.014 at 2.958. German-Italian spread is now down to 269. Earlier today, Nikkei closed up 0.62%, Singapore Strait Times rose 1.21%. But Hong Kong HSI dropped -0.03% while China Shanghai SSE rose 0.16% only. Japan 10 year JGB yield rose 0.0006 to 0.035.

Released in US, Empire State manufacturing index dropped sharply to 10.9 in December, down from 23.3 and missed expectation of 20.1. That’s also the lowest level since May 2017. Another point to note is that 6-month forward looking indicator also dropped to 30.6, down fro 33.6. Growth was “noticeably slower than in recent months” with deteriorating optimism.

Eurozone CPI finalized at 1.9%, core at 1.0% in November

Eurozone CPI was finalized at 1.9% yoy in November, down from 2.2% yoy in October. Nevertheless, it’s still notable improvement from 1.5% yoy in November 2017. Forex CPI was finalized at 1.0% yoy. European Union inflation was finalized at 2.0% yoy, down from 2.2% yoy. That compared to 1.8% yoy back in November 2017. Among EU member states, inflation was highest in Romania, Hungary and Estonia at 3.2%. Lowest inflation was recorded in Denmark at 0.7%.

Germany Bundesbank: Noticeable expansion in Q4 despite slow normalization in auto industry

In the latest monthly report, Germany’s Bundesbank warned that it may take more time for the auto industry to recovery from its recent “temporary” slump. It noted that “Normalization in the automotive industry may be slower than initially thought,” And, “the weak order intake from Germany and the slowdown in registration numbers could be an indication that domestic consumers are currently holding back on purchases”. Nevertheless, export orders remained strong and other segments of the economy performed well. In Q4, Bundesbank still expected “noticeable expansion.

Italy coalition government agreed on numbers and contents of 2019 revised budget

In Italy, leaders of the coalition government sounded optimistic that they would eventually avoid disciplinary actions by the EU over its 2019 budget. Leader of the League Matteo Salvini said, after meeting with 5-Star Movement head Luigi Di Maio and Prime Minister Giuseppe Conte, “We have found an agreement on further fiscal reductions that probably will be appreciated by the EU.”

Salvini’s spokeswoman also said that there is “total agreement between Conte, Salvini and Di Maio on the numbers and contents of the proposal to send to Brussels,” regarding 2019 budget plan. And she denied there were tensions within the coalition government and rumors that Prime Minister Giuseppe Conte had threatened to quit. Separately, Di Maio also said the talks with the commission “will allow us to avoid an infraction procedure”.

European Commission spokesman said today that “the dialogue continues between the European Commission and Italy concerning its budgetary plan for 2019”. And, “the Commission will decide on the next steps on the basis of the outcome of this ongoing dialogue.”

US ambassador to WTO: China is incompatible with the open, market-based approach

At the WTO Trade Policy Review of the US, the country’s ambassador Dennis Shea complained that China’s ” state-led, mercantilist approach to the economy and trade” and actions are “incompatible with the open, market-based approach” of the WTO and its members. At the same time, “he further criticized that “the WTO is not well equipped to handle the fundamental challenge posed by China”.

He elaborated and said “China pursues an array of non-market industrial policies and other unfair competitive practices aimed at promoting and supporting its domestic industries while simultaneously restricting, taking advantage of, discriminating against, or otherwise creating disadvantages for foreign companies and their goods and services.”

And, “from forced technology transfer to the creation and maintenance of severe excess industrial capacity to a heavily skewed playing field in China, the results of China’s approach are causing serious harm to the United States and many other WTO Members and their companies and workers.”

On the other hand, he hailed that the US “maintains one of the world’s most open trade regimes that is firmly based in the rule of law and that is a powerful engine for global growth”. The US continues to “seek trade liberalization and will deepen our relationships with countries who share our commitment to fair market competition and reciprocity.”

IMF: Global growth a little slower than October forecast due to trade war

IMF Director of Asia and Pacific department Changyong Rhee indicated that US-China trade war is already having an impact on business confidence and investment in Asia. And there could be global growth forecasts downgrades in the next update in January. In particular, he said Japan and South Korea could be among the those hardest hit due to reliance on exports to China.

He noted that “Investment is much weaker than expected. My interpretation is that the confidence channel is already affecting the global economy, particularly Asian economies”. And, “we see global growth a little bit slower than we forecast in October.” He also added that “Uncertainty is so large … uncertainty means you have upside potential as well as downside risk. At this moment, we believe the downside risk is a little bit higher.”

Regarding China, Rhee said “They aren’t accelerating (stimulus) yet but taking the foot from the brake for the time being. But that doesn’t exclude the possibility that if the trade tension escalates, if growth goes down, they are ready to use stimulus.” But at the same time, IMF is concerned with China’s medium term goals including deleveraging And Rhee urged that “when they actually try to use stimulus, we hope they can use more fiscal policy rather than credit expansion.”

IMF: BoJ should maintain stimulus as side-effects won’t outweigh benefits

IMF mission chief for Japan Paul Cashin said BoJ should maintain its massive stimulus program as “the so-called side-effects are not large enough to outweigh the benefits at present:. He added “the only game in town is achieving the target” of 2% inflation. He warned that “Tightening now is not going to help you get there. They’re very much committed to reaching the target, and we think that’s the right thing to do.”

On to the planned sale tax hike, he said “we’re not against putting them in and some of the revenue can be used for (tax breaks) but only on a temporary, time-bound basis.” He emphasized “equally important is clear communication on what these measures are, when they will begin and what particular tax and subsidies will be involved … because people plan ahead and won’t wait until October to make consumption decisions.”

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9942; (P) 0.9967; (R1) 1.0005; More…

USD/CHF’s pull back from 0.9989 accelerates lower today. Focus is back on 0.9911 minor support. Break there will confirm completion of the rebound from 0.9862. Deeper decline would be seen back to 0.9862. For now, price actions from 1.0128 are viewed as a corrective move. We’d expect strong support from 0.9848 support to bring reversal. On the upside, above 0.9989 will turn bias back to the upside. Break of 1.0008 will target a test on 1.0128 high.

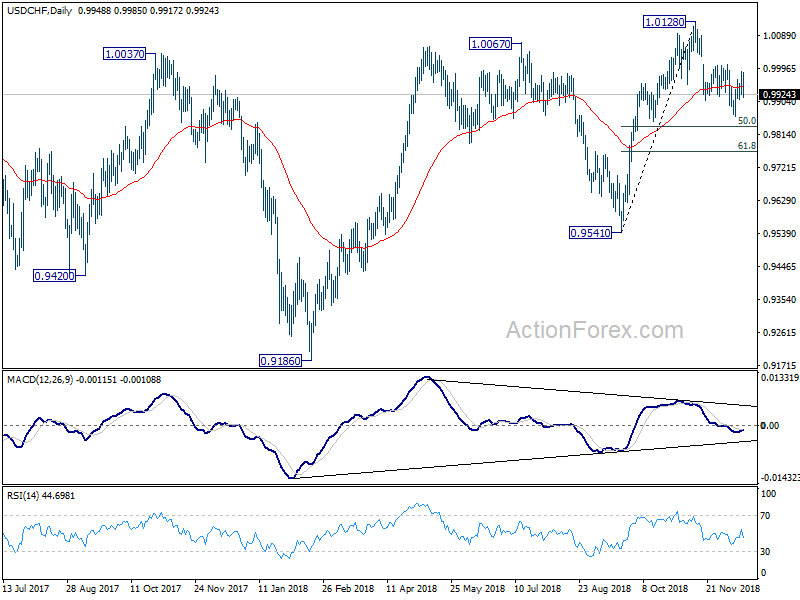

In the bigger picture, current development suggests that the medium term rally from 0.9186 hasn’t completed yet. Break of 1.0128 will target 1.0342 key resistance next (2016 high). On the downside, break of 0.9848 support will dampen this bullish view and turn focus back to 0.9541 key support instead.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 00:01 | GBP | Rightmove House Prices M/M Dec | -1.50% | -1.70% | ||

| 10:00 | EUR | Eurozone Trade Balance (EUR) Oct | 12.5B | 14.2B | 13.4B | |

| 10:00 | EUR | Eurozone CPI M/M Nov | -0.20% | 0.20% | 0.20% | |

| 10:00 | EUR | Eurozone CPI Y/Y Nov F | 1.90% | 2.00% | 2.00% | |

| 10:00 | EUR | Eurozone CPI Core Y/Y Nov F | 1.00% | 1.00% | 1.00% | |

| 13:30 | CAD | International Securities Transactions (CAD) Oct | 3.98B | 6.20B | 7.70B | |

| 13:30 | USD | Empire State Manufacturing Dec | 10.9 | 20.1 | 23.3 | |

| 15:00 | USD | NAHB Housing Market Index Dec | 61 | 60 | ||

| 21:00 | USD | Net Long-term TIC Flows Oct | 30.8B |