Canadian Dollar strengthens mildly in early US session and is trading as the strongest one for today so far. Recovery in oil price has been supporting the Loonie through the day. And, further lift is given by stronger than expected CPI reading. Euro is following as the second strongest, partly thanks to recovery in EUR/GBP.

Meanwhile, Sterling is paring some of this week’s Brexit chaos gains, also pressured by way worse than expected retail sales. Yen is the second weakest on return of risk appetite, on optimism on a US-China trade deal. For the week, Sterling remains the strongest one, followed by Canadian and then Dollar. Swiss Franc is the weakest, followed by Kiwi and then Yen.

Technically, a focus before weekly close is on 1.3180 temporary low in USD/CAD. Break will resume the decline from 1.3664 to 1.3118 fibonacci level. 0.9963 in USD/CHF and 1.1340 and EUR/CHF will also be watch for confirming near term bullish reversals in the pairs. DOW futures point to another day of rally in US stocks. That could push Yen crosses higher too.

In other markets, FTSE is currently up 1.76%. DAX is up 2.05%. CAC is up 1.65%. German 10 year yield is up 0.0148 at 0.26. Earlier in Asian, Nikkei rose 1.29%. Hong Kong HSI rose 1.25%. China Shanghai SSE rose 1.42%. Singapore Strait Times rose 0.31%. Japan 10 year JGB yield rose 0.0019 to 0.013.

Canadian Dollar rises mildly after stronger than expected CPI data.

Headline CPI dropped -0.1% mom in December versus expectation of -0.3%. Annually, CPI accelerated to 2.0% yoy, up from 1.7% yoy and beat expectation of 1.8% yoy.

Core CPI readings were steady. CPI core-common was unchanged at 1.9% yoy. CPI core-median dropped from 1.9% yoy to 1.8% yoy. CPI core-trimmed was unchanged at 1.9% yoy.

Sterling dips after poor December UK retail sales

Sterling weakens notably after rather poor December UK retail sales data. Retail sales including auto fuel dropped -0.9% mom versus expectation of -0.7%. Retail sales excluding auto fuel dropped -1.3% mom versus expectation of -0.5% mom. Also, for the three months to December, compared with the previous three months, retail sales including auto fuel dropped -0.2%. Retail sales excluding auto fuel dropped -0.4%

Also released in European session, Eurozone current account surplus narrowed to EUR 20.3B in November. Swiss PPI slowed to 0.4% yoy in December.

EU: UK will still need to elect MEP if it leaves after July 2

European Commission spokesman Margaritis Schinas once again told a regular news briefing that there is no request for Article 50 extension from the UK yet. But he pointed out that if the UK is going to leave after July 2, Britons will need to elect their representatives to the next European Parliament.

He said, “We … as the guardian of EU treaties, suggest caution with any suggestion that the right of EU citizens to vote in the European Parliament elections, according to the rules that are applicable, could be called into question”.

And, “we have a legally composed European Parliament which requires directly elected MEPs from all member states at the latest on the first day of the new term of the new parliament, which this time is the second of July.”

European Commission publishes draft trade negotiating mandates with the US

European Commission publishes draft negotiating mandates with the US today. The negotiating directives cover two potential agreements with the U.S:

- A trade agreement strictly focused on the removal of tariffs on industrial goods, excluding agricultural products;

- A second agreement, on conformity assessment, that would help address the objective of removing non-tariff barriers, by making it easier for companies to prove their products meet technical requirements on both sides of the Atlantic.

EU Commissioner for Trade Cecilia Malmström said in the statement: “Today’s publication of our draft negotiating directives is part of the implementation of the July joint statement of Presidents Juncker and Trump. Ambassador Lighthizer and I have already met several times in the Executive Working Group and I have made it very clear that the EU is committed to upholding its side of the agreement reached by the two Presidents. These two proposed negotiating directives will enable the Commission to work on removing tariffs and non-tariff barriers to transatlantic trade in industrial goods, key goals of the July Joint Statement.”

In a press conference, Malmström added “We are prepared to put our vehicles tariffs on the negotiating table (..) if the U.S. agree to work together toward zero tariffs on industrial goods.” But still, EU was ready to retaliate if the U.S. imposed car import tariffs.

Germany and China signed pacts to deepen financial sector cooperation

Germany and China pledged to deepening cooperation in the finance sector and fight trade protectionism during Finance Minister Olaf Scholz’s two-day visit to Beijing. And three pacts are signed, including agreements with the China Banking and Insurance Regulatory Commission and China’s Securities Regulatory Commission.

Ahead of today’s meeting with Chinese Vice Premier Liu He, Scholz said “it is important that, contrary to recent trends that we can observe elsewhere, we are seeing progress in our cooperation”. And, “we have a lot of common interests in financial matters, and then we need to bring different perspectives together. I believe that is the very important task of this financial dialogue.”

Japan core CPI slowed more than expected to 0.7% in Dec

In December, Japan all item CPI slowed to 0.3% yoy, down from 0.8% yoy and matched expectation. Core CPI, all item ex-fresh food, slowed to 0.7% yoy, down from 0.9% yoy and missed expectation of 0.8% yoy. Core-core CPI, al item ex-fresh food, energy, stayed unchanged at 0.3% yoy.

The data showed that even discounting the fall in energy prices, consumer inflation stayed week. And apparently, the recovery is not passed on to consumers. And business remained reluctant to raise prices.

The data added to the case for BoJ to cut inflation forecasts next week. Back in October, BoJ projects core CPI to hit 1.4% in fiscal 2019 and then 1.5% in fiscal 2020. Such projections would be trimmed to reflect the decline in oil as well as global slowdown.

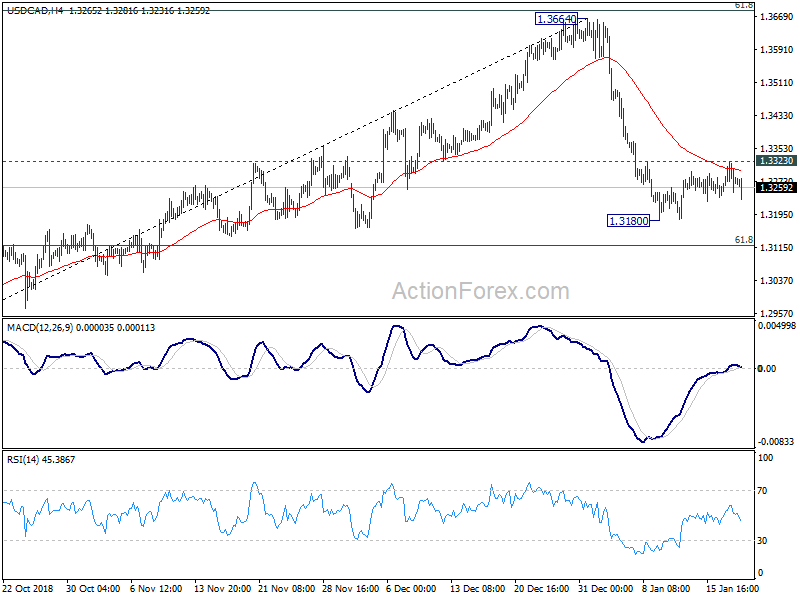

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.3245; (P) 1.3283; (R1) 1.3317; More…

USD/CAD dips notably today but stays above 1.3180 temporary low. Intraday bias remains neutral first. With 1.3323 resistance intact, further decline is expected. On the downside, break of 1.3180 will resume the fall from 1.3664 and target 61.8% retracement of 1.2781 to 1.3664 at 1.3118. We’ll start to look for bottoming sign below there. On the upside, above 1.3323 will suggest short term bottoming and turn bias back to the upside for stronger rebound.

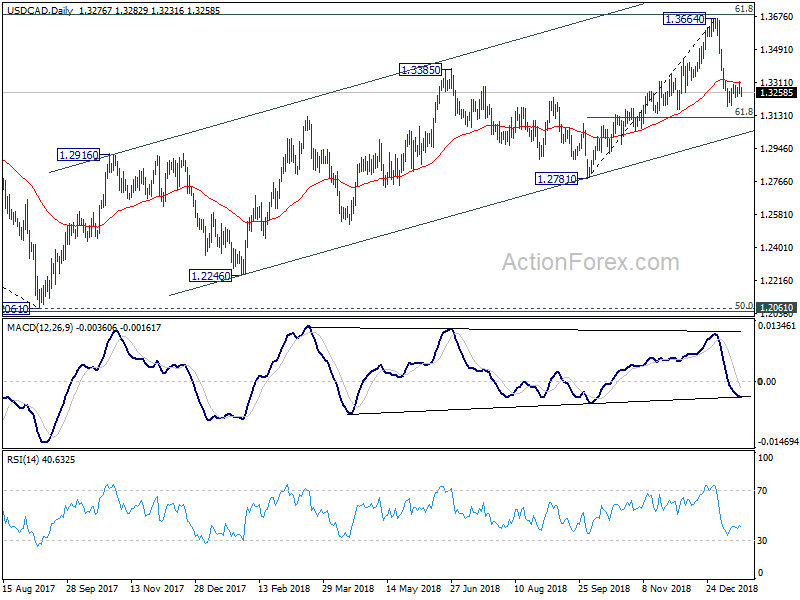

In the bigger picture, the medium term rise from 1.2061 (2017 low) might continue further. But the structure of such rise is not clearly impulsive so far. Hence, we’d stay cautious on strong resistance from 61.8% retracement of 1.4689 (2016 high) to 1.2061 at 1.3685 and 1.3793 resistance to limit upside, and bring medium term topping. But in any case, medium term outlook will stay bullish as long as channel support (now at 1.2993) holds. Sustained break of 1.3793 will pave the way to retest 1.4689 (2015 high).

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:30 | NZD | BusinessNZ Manufacturing PMI Dec | 55.1 | 53.5 | 53.7 | |

| 23:30 | JPY | National CPI Core Y/Y Dec | 0.70% | 0.80% | 0.90% | |

| 04:30 | JPY | Industrial Production M/M Nov F | -1.00% | -1.10% | -1.10% | |

| 07:30 | CHF | Producer & Import Prices M/M Dec | -0.60% | -0.20% | -0.30% | |

| 07:30 | CHF | Producer & Import Prices Y/Y Dec | 0.60% | 1.40% | ||

| 09:00 | EUR | Eurozone Current Account (EUR) Nov | 20.3B | 24.1B | 23.0B | 26.8B |

| 09:30 | GBP | Retail Sales Ex Auto Fuel M/M Dec | -1.30% | -0.50% | 1.20% | 1.00% |

| 09:30 | GBP | Retail Sales Ex Auto Fuel Y/Y Dec | 2.60% | 4.00% | 3.80% | 3.50% |

| 09:30 | GBP | Retail Sales Inc Auto Fuel M/M Dec | -0.90% | -0.70% | 1.40% | 1.30% |

| 09:30 | GBP | Retail Sales Inc Auto Fuel Y/Y Dec | 3.00% | 3.50% | 3.60% | 3.40% |

| 13:30 | CAD | International Securities Transactions (CAD) Nov | 9.45B | 2.05B | 3.98B | 3.97B |

| 13:30 | CAD | CPI M/M Dec | -0.10% | -0.30% | -0.40% | |

| 13:30 | CAD | CPI Y/Y Dec | 2.00% | 1.80% | 1.70% | |

| 13:30 | CAD | CPI Core – Common Y/Y Dec | 1.90% | 1.80% | 1.90% | |

| 13:30 | CAD | CPI Core – Median Y/Y Dec | 1.80% | 1.90% | 1.90% | |

| 13:30 | CAD | CPI Core – Trimmed Y/Y Dec | 1.90% | 1.80% | 1.90% | |

| 14:15 | USD | Industrial Production M/M Dec | 0.20% | 0.60% | ||

| 14:15 | USD | Capacity Utilization Dec | 78.40% | 78.50% | ||

| 15:00 | USD | U. of Mich. Sentiment Jan P | 96.1 | 98.3 |

{kind=link}