European majors are generally under pressure today. Weak economic data from Eurozone and UK is one of the factors. Stocks are indifferent to the data though, and rise broadly probably on expectation that loose monetary policy will stay longer. Selloff in Swiss Franc is also apparent, in particular with USD/CHF and EUR/CHF taking out near term resistance. On the other hand, Australian Dollar maintains post RBA gains and is trading as the strongest ones for today with New Zealand Dollar. Greenback is also trying to extend recent rebound.

Technically, USD/CHF has taken out 0.9994 resistance to resume rise from 0.9716 already. EUR/CHF also broke 1.1429 to resume rise from 1.1181. GBP/USD’s break of 1.3012 minor support is the first sign of bearish reversal on rejection by 1.3174 key resistance. Focus will turn to 1.1407 minor support in EUR/USD to confirm Dollar’s underlying strength. Despite today’s rebound, AUD/USD is help below 0.7295 resistance and EUR/AUD is kept above 1.5721 support. Aussie bulls are not that committed.

In other markets, FTSE is currently up 1.23%. DAX is up 1.05%. CAC is up 1.00%. German 10-year yield is up 0.0101 at 0.189, but stays below 0.2 handle. Earlier in Asia, Nikkei closed down -0.19%. Japan 10-year JGB yield rose 0.0036 to -0.008, staying negative. China, Hong Kong and Singapore are on lunar new year holiday.

UK PM May to meet EU Juncker on Thursday, Irish backstop plan awaited

UK Prime Minister Theresa May will travel to Brussels on Thursday to meet European Commission Jean-Claude Juncker. Obviously Brexit withdrawal agreement and Irish backstop will be the purpose.

Ahead of that, European Commission spokesman Margaritis Schinas said “the European Union’s position is clear.” And, “we are expecting, waiting once again to hear what the prime minister has to tell us.”

German Merkel: It’s humanly possible to solve a precise problem of Brexit Irish backstop

German Chancellor Angela Merkel indicated that there is still time to find a solution for Brexit before the March 29 deadline. She said in a conference in Tokyo that “from a political point of view, there is still time.” But she added “it would be very important to know what exactly the British side envisages in terms of its relationship with the EU.”

Also, on the specific problem of Irish backstop, Merkel said “It should be humanly possible to find a solution to such a precise problem. But this depends … on the kind of trade deal that we forge with each other.”

UK PMI services dropped to 50.1, Brexit uncertainty coincides with wider global slowdown

UK PMI Services dropped to 50.1 in January, down from 51.2 and missed expectation of 51.1. That’s the lowest level for two-and-a-half year and the second-weakest since December 2012. Markit also noted that business activity stagnates amid modest drop in new work. Staffing levels decline for the first time since December 2012. And, strong input cost inflation persists at start of 2019.

Chris Williamson, Chief Business Economist at IHS Markit, said “he UK economy is at risk of stalling or worse as escalating Brexit uncertainty coincides with a wider slower slowdown in the global economy.” And, GDP has likely “stagnated at the start of 2019 after eking out modest growth of just 0.1% in the fourth quarter.”

Also, “companies are becoming increasingly risk averse and eager to reduce overheads in the face of weakened customer demand and rising political uncertainty. Such worries were in turn most commonly linked to heightened Brexit anxiety, though wider global political and economic factors were also seen to have been taking their toll on demand.”

Eurozone PMI composite finalized at 5.5 year low, Q1 to be worst quarter since 2013

Eurozone PMI Services was finalized at 51.2, revised up from 50.8. That’s unchanged from the 49-month low recorded in December. PMI Composite was finalized at 51.0, lowest in five-and-a-half years. Among the countries, France PMI composite dropped to 48.2, 50-month low. Italy was at 48.8, 52-month low. Germany recovered to 52.1, a 2-month high. But Ireland dropped to 53.3, 67-month low.

Chris Williamson, Chief Business Economist at IHS Markit said, “the eurozone has started 2019 on flat note, with growth close to stagnation amid falling demand for goods and services.” And, “GDP is growing at a quarterly rate of just 0.1%, setting the scene for the region’s worst quarter since 2013.” And that would also mean ECB’s projection of 1.5% GDP growth in 2019 is “likely to be revised lower” and “lead to more dovish signals from the ECB”.

Also, “The survey indicates that political uncertainty, both global and local, is increasingly taking a toll on growth, dampening demand and driving increased risk aversion. Add in rising global trade tensions, Brexit uncertainty, the ‘yellow vest’ protests in France and a spluttering auto sector, it’s clear that the business environment is at its most challenging since the height of the region’s debt crisis.”

Also from Eurozone, retail sales dropped -1.6% mom in December, matched expectations.

RBA downgrades growth and inflation forecast, cites increased risks

Australian Dollar jumps after RBA left cash rate unchanged at 1.50% as widely expected. The conclusion of the statement was kept totally unchanged. And most importantly, RBA maintained “further progress in reducing unemployment and having inflation return to target is expected, although this progress is likely to be gradual.”

There are some dovish tweaks in the statement, including mentioning of increased risks, downgrade of growth and inflation forecasts. But for now, the statement still suggests the next move is a hike rather than a cut. Just that it may take longer to happen.

Globally, RBA said growth “remains reasonable” but “downside risks have increased”. In particular “trade tensions are affecting global trade and some investment decisions”. Headline inflation also “moved lower” due to fall in oil prices. Regarding financial markets, RBA also noted government bond yields have declined in most countries including Australia. Australia’s terms of trade are “expected to decline over time”

Domestically, RBA expects Australian economy to growth by around 3% in 2019 and a little less in 2020. That’s a downward revision from prior expectation of growth at 3.5% in 2019. Further than that, RBA acknowledged weaker than expected growth in Q3 and said “some downside risks have increased”. And, “the main domestic uncertainty remains around the outlook for household spending and the effect of falling housing prices in some cities.”

On inflation, RBA now expects underlying inflation to hit 2% in 2019 and 2.25% in 2020. Headline inflation is also expected to decline in the near term due to petrol prices. That’s also a downgrade as in previously, RBA expected inflation to hit 2.25% in 2019 and a bit higher in 2020.

Also from Australia, AiG performance of services dropped sharply from 52.1 to 44.3 in January. Retail sales dropped -0.4% mom in December versus expectation of 0.0%. Trade surplus widened to AUD 3.68B in December versus expectation of AUD 2.25B.

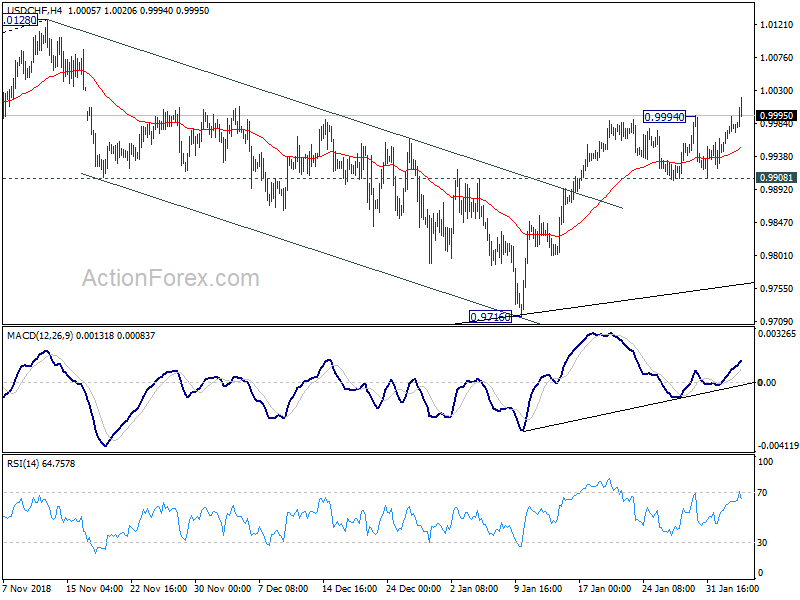

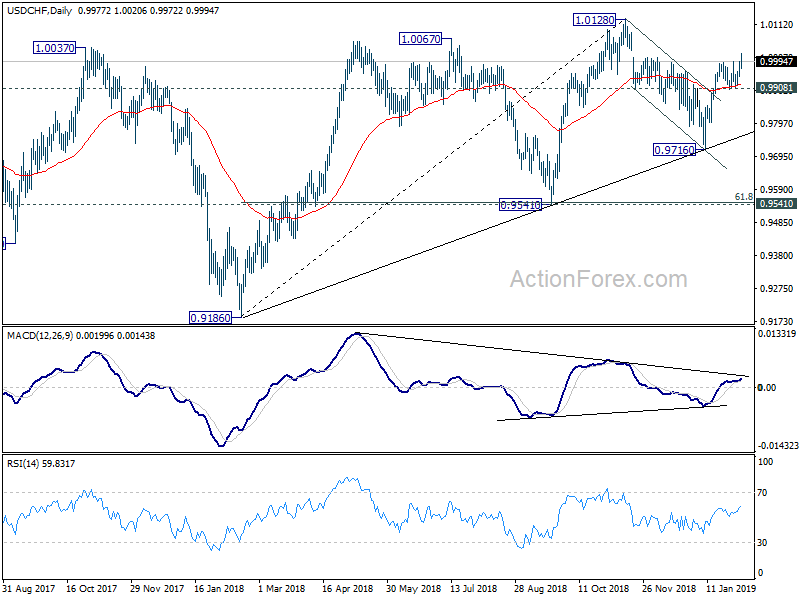

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9948; (P) 0.9971; (R1) 1.0003; More….

USD/CHF’s rise break of 0.9994 resistance suggests that rise from 0.9716 has resumed. Intraday bias is back on the upside. Outlook is unchanged that corrective decline from 1.0128 should have completed at 0.9716 already, after hitting trend line support. Further rally should now be seen back to retest 1.0128. On the downside, break of 0.9908 is needed to indicate completion of the rebound. Otherwise, outlook will stay cautiously bullish in case of retreat.

In the bigger picture, USD/CHF drew strong support from medium term trend line and rebounded. That suggests rise from 0.9186 is still in progress. Further break of 1.0128 will confirm up trend resumption and target 1.0342 key resistance. Nevertheless, break of 0.9716 will dampen this bullish view and at least bring deeper fall to 0.9541 key support.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:30 | AUD | AiG Performance of Service Index Jan | 44.3 | 52.1 | ||

| 0:01 | GBP | BRC Retail Sales Monitor Y/Y Jan | 2.10% | -0.20% | -0.70% | |

| 0:30 | AUD | Trade Balance (AUD) Dec | 3.68B | 2.25B | 1.93B | 2.26B |

| 0:30 | AUD | Retail Sales M/M Dec | -0.40% | 0.00% | 0.40% | 0.50% |

| 3:30 | AUD | RBA Rate Decision | 1.50% | 1.50% | 1.50% | |

| 8:45 | EUR | Italy Services PMI Jan | 49.7 | 50 | 50.5 | |

| 8:50 | EUR | France Services PMI Jan F | 47.8 | 47.5 | 47.5 | |

| 8:55 | EUR | Germany Services PMI Jan F | 53 | 53.1 | 53.1 | |

| 9:00 | EUR | Eurozone Services PMI Jan F | 51.2 | 50.8 | 50.8 | |

| 9:30 | GBP | Services PMI Jan | 50.1 | 51.1 | 51.2 | |

| 10:00 | EUR | Eurozone Retail Sales M/M Dec | -1.60% | -1.60% | 0.60% | 0.80% |

| 14:45 | USD | US Services PMI Jan F | 54.2 | 54.2 | ||

| 15:00 | USD | ISM Non-Manufacturing/Services Composite Jan | 57 | 57.6 |

{kind=link}