Yen and Gold surge today as global sentiments are weighed down by new US sanctions on Iran. In particular, Gold hits as high as 1439 and is currently up more than 1%. Nevertheless, New Zealand Dollar outshines Yen and is currently the strongest one for today. Kiwi is boosted by record exports in May, which solidify the case for RBNZ to stand pat tomorrow. Sterling is the second strongest for now, helped by pull back in EUR/GBP.

Technically, a major focus will be on whether Dollar could stage a recovery from the current point. EUR/USD is now close to close to 1.1142 fibonacci projection level, and a retreat is due. While GBP/USD edges higher today, it’s feeling heavy ahead of 1.2840 fibonacci resistance. On the other hand, USD/JPY’s downside momentum remains solid and could fall further towards 104.69 before trading to bottom. Trade development and Fed Chair Jerome Powell’s comment might help decide the direction.

In other markets, Nikkei closed down -0.52%. China Shanghai SSE closed down -0.87%. Hong Kong HSI is down -1.19%. Singapore Strait Times is down -0.20%. Japan 10-year JGB yield is up 0.0001 at -0.151. Overnight, DOW rose 0.03%. S&P 500 dropped -0.17%. NASDAQ dropped -0.32%. 10-year yield dropped -0.047 to -2.021. staying above 2% handle.

Trump puts sanctions on Iranian supreme leader and officials

Trump signed an executive order imposing sanctions on Iranian Supreme Leader Ayatollah Ali Khamenei and other top Iranian officials. He condemned Khamenei as “the hostile conduct of the regime” in the Middle East.

The sanctions will “deny the Supreme Leader and the Supreme Leader’s office, and those closely affiliated with him and the office, access to key financial resources and support.” They could lock up billions of dollars more in Iranian assets. They were in part a response to downing of a US drone by Iran last week.

Iranian Foreign Ministry responded: “Imposing useless sanctions on Iran’s Supreme Leader Khamenei and the commander of Iran’s diplomacy is the permanent closure of the path of diplomacy. Trump’s desperate administration is destroying the established international mechanisms for maintaining world peace and security.”

Chinese Liu had phone call with Lighthizer & Mnuchin, agreed to maintain communications

The Chinese Ministry of Commerce confirmed that Vice Premier Liu He had a phone call with US Trade Representative Robert Lighthizer and Treasury Secretary Steven Mnuchin on Monday. During the call, both sides exchanged opinions on trade and agreed to maintain communications. Works are believed to be carried out ahead of the meeting between Trump and Xi on the second day of the June 28-29 G20 summit in Osaka, Japan. For now, there is no indications on how the two sides could close the wide gap in their bottom lines.

Reuters reported, citing an unnamed US senior officials that “it’s really just an opportunity for the president to maintain his engagement as he has very closely with his Chinese counterpart.”. And, Trump is “quite comfortable with any outcome.” Another unnamed official said “the president has been quite clear that he needs to see structural real reform in China across a number of issues and a number of sectors, and nothing about that has changed.” And, “the fact that talks broke down in May hasn’t changed that as the ultimate goal”.

Separately, Japanese Economy Minister Toshimitsu Motegi said he’ll meet Lighthizer this week. He’d announce details including the date and location of the talks once they were set.

BoJ April Minutes: Clarifications on forward guidance added to strengthen public confidence on persistent easing stance

The Minutes of April 24-25 BoJ meeting showed that some members suggested clarifications on the forward guidance, “with the aim of strengthening public confidence in its monetary easing stance”. That came as “many members” recognized the “high uncertainties” regarding economic outlook and prices. And, it was likely to “still take time to achieve 2 percent inflation”.

In the statement after that meeting, BoJ added: “The Bank intends to maintain the current extremely low levels of short- and long-term interest rates for an extended period of time, at least through around spring 2020, taking into account uncertainties regarding economic activity and prices including developments in overseas economies and the effects of the scheduled consumption tax hike.”

One member said “at least through around spring 2020” as providing a specific time frame with open-ended elements. Some members also noted that clarifying the meaning of “for an extended period of time” implied a fairly long period of time was necessary.

Also from Japan, corporate service price index rose 0.8% yoy in May, below expectation of 1.0% yoy.

New Zealand exports jumped to record high, trade surplus at NZD 264M

In May, New Zealand good export rose 8.5% yoy to NZD 5.8B, hitting a record high. Import rose 7.6% yoy to NZD 5.5B. Trade surplus came in at NZD 264m, above expectation of NZD 200m. In particular, exports to China rose 29% yoy to NZD 1.5B led by rises in milk powder, beef, food preparations and logs. Strong terms of trade reaffirms RBNZ’s stance to stand pat tomorrow. Yet, the central bank will likely maintain openness to further rate cut later in the year.

Looking ahead

UK will release CBI reported sales. US will release house price index, S&P Case-Shiller house price and new home sales. But major focus will be on Conference Board consumer confidence. Also, Fed Chair Jerome Powell will speak again today.

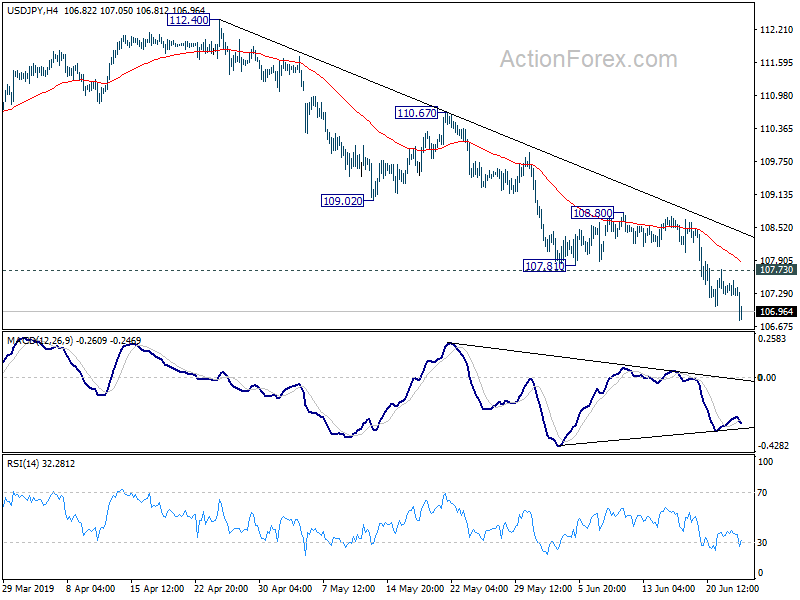

USD/JPY Daily Outlook

Daily Pivots: (S1) 107.19; (P) 107.36; (R1) 107.47; More…

USD/JPY’s decline resumed after brief consolidations and reaches as low as 106.78 so far. Intraday bias is back on the downside. Current fall from 112.40 should target 104.69 low next. On the upside, above 107.73 minor resistance will turn intraday bias neutral again. But outlook will remain bearish as long as 108.80 resistance holds.

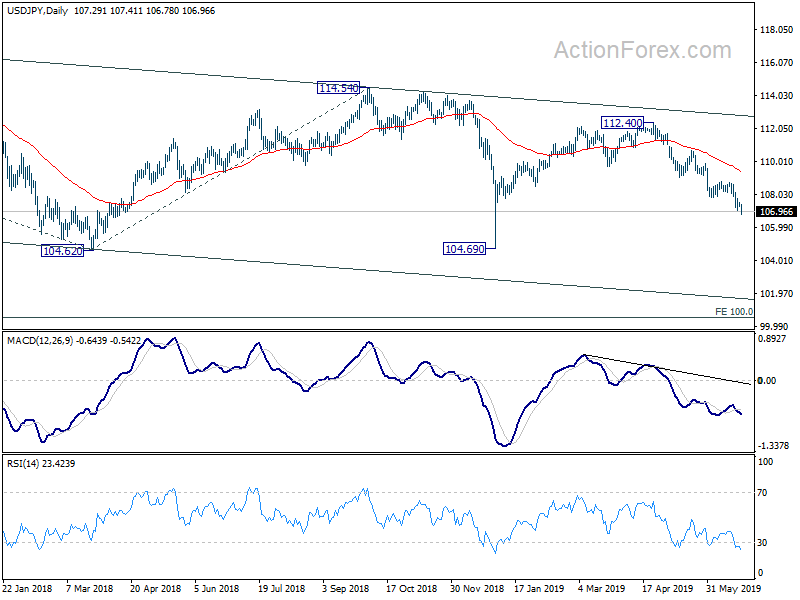

In the bigger picture, decline from 118.65 (Dec 2016) is still in progress, with the pair staying inside long term falling channel. Break of 104.62 will target 100% projection of 118.65 to 104.62 from 114.54 at 100.51. For now, we’d expect strong support above 98.97 (2016 low) to contain downside to bring rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Trade Balance May | 264M | 200M | 433M | 383M |

| 23:50 | JPY | BOJ Minutes Apr | ||||

| 23:50 | JPY | Corporate Service Price Y/Y May | 0.80% | 1.00% | 0.90% | 1.00% |

| 10:00 | GBP | CBI Reported Sales Jun | -3 | -27 | ||

| 12:30 | CAD | Wholesale Trade Sales M/M Apr | 0.30% | 1.40% | ||

| 13:00 | USD | House Price Index M/M Apr | 0.20% | 0.10% | ||

| 13:00 | USD | S&P/Case-Shiller Composite-20 Y/Y Apr | 2.50% | 2.68% | ||

| 14:00 | USD | New Home Sales May | 686K | 673K | ||

| 14:00 | USD | Consumer Confidence Jun | 131 | 134.1 |

{kind=link}