Sterling remains the overwhelmingly weakest one on no-deal Brexit concerns. New Prime Minister Boris Johnson is pushing EU to re-open Brexit negotiation. But there is no sign from EU on a position shift yet. Australian and New Zealand Dollars are the next weakest as markets turn into risk averse mode. On the other hand, Swiss Franc is the strongest one, followed Euro. Dollar is mixed as today’s US core PCE inflation reading is not enough to alter Fed’s decision to cut interest rate tomorrow.

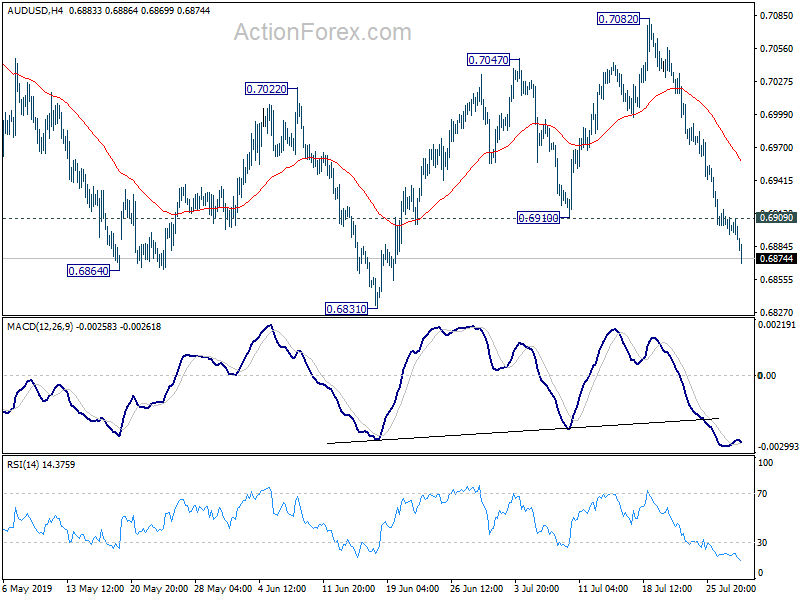

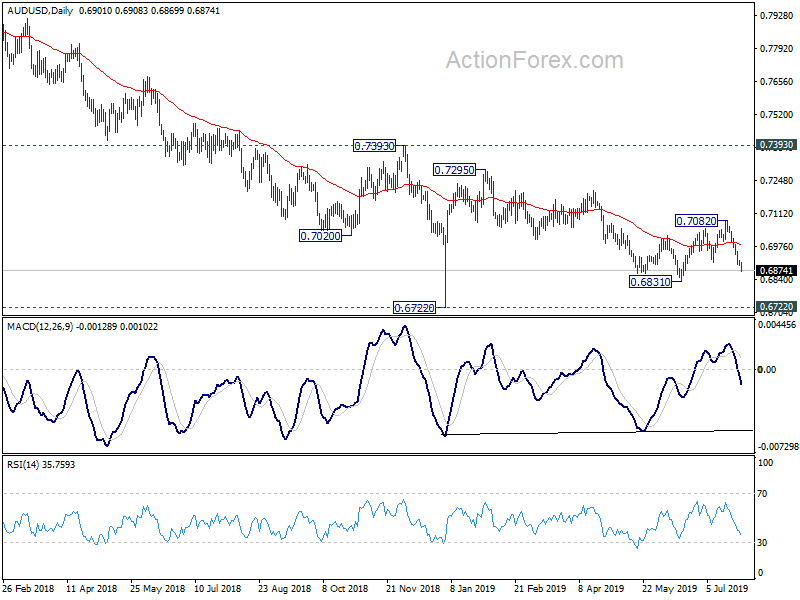

Technically, selloff in Australian Dollar intensifies in early US session on risk aversion. AUD/USD is on track to retest 0.6831 support. EUR/AUD is pressing 1.6231 resistance and break will confirm completion of corrective fall from 1.6448 at 1.5894. Further rise could then be seen back to retest 1.6448.

In other markets, US stocks open mildly lower with DOW down -0.30% at the time of writing. 10-year yield is flat at 2.066. In Europe, FTSE is down -0.41%. DAX is down -2.23%. CAC is down -1.62%. German 10-year yield is down -0.0053 % -0.394. Earlier in Asia, Nikkei rose 0.43%. Hong Kong HSI rose 0.14%. China Shanghai rose 0.39%. Singapore Strait Times rose 0.12%. Japan 10-year JGB yield dropped -0.0044 to -0.151.

US core PCE rose to 1.6%, not enough to change Fed’s decision

In June, personal income rose 0.4%, above expectation of 0.3%. Personal spending rose 0.3%, matched expectations. Headline PCE was unchanged at 1.4% yoy, missed expectation of 1.5% yoy. Core PCE inflation accelerated to 1.6% yoy, up from 1.5% yoy, but missed expectation of 1.7% yoy.

The lack up materialistic acceleration in core inflation does nothing to alter FOMC policymakers’ mind regarding tomorrow’s rate decision. For now, Fed is still generally expected to cut interest rate by -0.25bps to 2.00-2.25%. The main question is whether Fed would explicitly say that it’s a one-off, or it’s a start of a policy easing cycle.

Also from the US, S&P Case-Shillar 20-cities house price rose 2.% yoy in May, matched expectations. Pending home sales rose 2.8% mom in June, above expectation of 0.3% mom. Consumer confidence improved to 135.7, up from 124.3, beat expectation of 125.0.

Eurozone confidence indicators deteriorated in July

Eurozone economic confidence dropped to 102.7 in July, down from 103.3 but matched expectation. Industrial confidence dropped to -7.4, missed expectation of -6.7. Services confidence dropped to 10.6, missed expectation of 10.7. Consumer confidence was finalized at -6.6. Business climate indicator dropped to -0.12, missed expectation of 102.7.

German CPI accelerated, consumer confidence dropped slightly

German CPI rose 0.5% mom in July, above expectation of 0.5% mom. Annually, CPI accelerated to 1.7% yoy, beat expectation of 1.5% yoy.

Gfk consumer confidence for August dropped -0.1 to 9.7, matched expectations. Economic expectations dropped from 2.4 to -3.7. Income expectations improved from 45.5 to 50.8. Propensity to buy dropped from 53.7 to 46.3. Gfk noted that “It is apparent that the global economic slowdown, trade conflict and Brexit discussions are having an ever increasing impact on consumer confidence. Thus, economic expectations continue to decline and the propensity to buy has dropped off slightly as well.”

Economic expectation fell below its long-standing average of 0 for the first time since March 2016. It’s also the lowest reading since November 2015. Gfk said: “The trade war with the US, ongoing Brexit discussions and the global economic slowdown continue to drive fears of a recession. Employees in export-driven sectors in particular, such as the automotive industry and its suppliers, are most immediately affected by this. In addition, reports of downsizing add to employees’ fears of losing their jobs.”

French GDP grew 0.2% qoq in Q2, missed expectation

French GDP grew 0.2% qoq in Q2, missed expectation of 0.3% qoq, slowed from Q1’s 0.3% qoq. Looking at the details, household consumption expenditure slowed from 0.4% qoq to 0.2% qoq. But total gross fixed capital formation jumped from 0.5% qoq to 0.9% qoq. Final domestic demand excluding inventories accelerated slightly. Imports were stable, slowed from 1.1% qoq to 0.1% qoq. Export growth was unchanged at 0.2% qoq. Foreign trade balance didn’t contribute to GDP growth, at 0.0%.

Swiss KOF rose to 97.1, slightly more favorable signals from manufacturing, and services

Swiss KOF Economic Barometer rose to 97.1 in July, up fro 93.8 and beat expectation of 93.3. KOF said: “Slightly more favourable signals than before are coming from manufacturing, other services, accommodation and food service activities as well as financial and insurance services. Construction is contributing slightly to the positive development. Consumer prospects are practically unchanged. On the other hand, the indicators for demand from abroad have a dampening effect.”

BoJ Kuroda: We went a step forward to additional policy easing

BoJ left monetary policy unchanged today as widely expected. Under the yield curve control framework, short-term policy interest rate is held at -0.10%. 10-year JGB yield will be held at around zero percent with JGB purchases. Monetary base will increase at an annual pace of around JPY 80T. The decisions are made with 7-2 vote with Y. Harada and G. Kataoka dissented again.

In the post policy meeting press conference, BoJ Governor Haruhiko Kuroda indicated that the central bank has already taken a step forward to further monetary easing. And, the tools include cutting short-, long-term interest rates, increasing asset buying or accelerate the pace of base money expansion.

Kuroda said, “today, we went a step forward by saying we’ll take additional easing steps without hesitation if there is a risk the economy will lose momentum for hitting our price target”. And, “previously, we said only that we will consider acting if the economy loses momentum for hitting our price goal.”

Nevertheless, Kuroda also noted “I don’t think Japan has lost momentum to hit the BOJ’s price goal, or that there is an imminent risk of this happening.”. While, policymakers need to pay attention to downside risks, for now, “we expect the economy to continue expanding moderately, and that it is sustaining momentum for hitting our price goal.”

Japan industrial production dropped -3.6% in indecisive fluctuations

Japan industrial production dropped sharply by -3.6% mom in June, much worst than expectation of -1.8% mom. That’s also the largest decline since January 2018. Shipments dropped -3.3% mom while inventories rose 0.3% mom.

A Ministry of Economy, Trade and Industry said in the press briefing that the decline was a reversal of the unexpectedly strong production in the preceding months.” He added, “we don’t believe there is a downward trend, though there isn’t an upward trend either”. Production just “fluctuates indecisively”.

Also from Japan, unemployment rate improved to 2.3% in June, down from 2.4%. Number of people in work hit record 67.5m. Ministry of Internal Affairs and Communications said “the jobless rate has been firm and moving narrowly at that level”.

AUD/USD Mid-Day Outlook

Daily Pivots: (S1) 0.6892; (P) 0.6904; (R1) 0.6914; More…

AUD/USD’s fall extends to as low as 0.6869 so far and intraday bias remains on the downside for 0.6831 low. The three wave corrective structure from 0.6831 to 0.7082 suggests that larger decline from 0.7295 is in progress and is possibly resuming. Break of 0.6831 will confirm this bearish case and target 0.6722 low next. On the upside, break of 0.6909 minor resistance will turn intraday bias neutral again.

In the bigger picture, with 0.7393 key resistance intact, medium term outlook remains bearish. The decline from 0.8135 (2018 high) is seen as resuming long term down trend from 1.1079 (2011 high). Decisive break of 0.6826 (2016 low) will confirm this bearish view and resume the down trend to 0.6008 (2008 low). However, firm break of 0.7393 will argue that fall from 0.8135 has completed. And corrective pattern from 0.6826 has started the third leg, targeting 0.8135 again.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Consensus | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Building Permits M/M Jun | -3.90% | 13.20% | 13.50% | |

| 23:30 | JPY | Jobless Rate Jun | 2.30% | 2.40% | 2.40% | |

| 23:50 | JPY | Industrial Production M/M Jun P | -3.60% | -1.80% | 2.00% | |

| 01:30 | AUD | Building Approvals M/M Jun | -1.20% | 0.20% | 0.70% | 0.30% |

| 02:00 | JPY | BOJ Rate Decision | -0.10% | -0.10% | -0.10% | |

| 05:30 | EUR | French GDP Q/Q Q2 P | 0.20% | 0.30% | 0.30% | |

| 06:00 | EUR | German GfK Consumer Confidence Aug | 9.7 | 9.7 | 9.8 | |

| 07:00 | CHF | KOF Leading Indicator Jul | 97.1 | 93.3 | 93.6 | 93.8 |

| 09:00 | EUR | Eurozone Business Climate Indicator Jul | -0.12 | 0.1 | 0.17 | |

| 09:00 | EUR | Eurozone Economic Confidence Jul | 102.7 | 102.7 | 103.3 | |

| 09:00 | EUR | Eurozone Industrial Confidence Jul | -7.4 | -6.7 | -5.6 | |

| 09:00 | EUR | Eurozone Services Confidence Jul | 10.6 | 10.7 | 11 | |

| 09:00 | EUR | Eurozone Consumer Confidence Jul F | -6.6 | -6.6 | -6.6 | -7.2 |

| 12:00 | EUR | German CPI M/M Jull P | 0.50% | 0.30% | 0.30% | |

| 12:00 | EUR | German CPI Y/Y Jull P | 1.70% | 1.50% | 1.60% | |

| 12:30 | USD | Personal Income Jun | 0.40% | 0.30% | 0.50% | 0.40% |

| 12:30 | USD | Personal Spending Jun | 0.30% | 0.30% | 0.40% | 0.50% |

| 12:30 | USD | PCE Deflator M/M Jun | 0.10% | 0.10% | 0.20% | |

| 12:30 | USD | PCE Deflator Y/Y Jun | 1.40% | 1.50% | 1.50% | 1.40% |

| 12:30 | USD | PCE Core M/M Jun | 0.20% | 0.20% | 0.20% | |

| 12:30 | USD | PCE Core Y/Y Jun | 1.60% | 1.70% | 1.60% | 1.50% |

| 13:00 | USD | S&P/Case-Shiller Composite-20 Y/Y May | 2.40% | 2.40% | 2.54% | |

| 14:00 | USD | Pending Home Sales M/M Jun | 2.80% | 0.30% | 1.10% | |

| 14:00 | USD | Consumer Confidence Index Jul | 135.7 | 125 | 121.5 | 124.3 |

{kind=link}