Sterling rises broadly today as MPs are expected to back to work on blocking no-deal Brexit after Supreme Court ruling. Meanwhile, Australian Dollar is lifted by RBA Governor’s refrain from signaling an imminent rate cut next week. New Zealand Dollar follows higher too. On the other hand, Yen and Dollar turn softer today. Euro is mixed, unmoved by slight improvement in German business confidence.

Technically, Sterling’s recovery, while notably, doesn’t push it through this week’s range against Dollar, Euro and Yen. Intraday bias in GBP/USD and GBP/JPY will stay neutral as long as 1.2582 and 135.74 temporary tops hold, respectively. Intraday bias in EUR/GBP also stays neutral as long as 0.8687 temporary low holds. Other major forex pairs and crosses are staying in consolidations in general.

In Europe, FTSE is down -0.44%. DAX is flat. CAC is up 0.18%. German 10-year yield is up 0.002 at -0.576. Earlier in Asia, Nikkei rose 0.09%. Hong Kong HSI rose 0.22%. China Shanghai SSE rose 0.28%. Singapore Strait Times rose 0.39%. Japan 10-year JGB yield dropped -0.0209 to -0.239.

Sterling rebounds as UK Supreme Court rules Johnson’s parliament suspension unlawful

Sterling rebounds notably after UK’s Supreme Court ruled that Prime Minister Boris Johnson’s move to shut down the parliament was unlawful. And Supreme Court President Brenda Hale said both houses should return as soon as possible. The ruling gave MPs a boost to continue with their work to block no-deal Brexit on October 31.

Hale said, “The decision to advise Her Majesty to prorogue parliament was unlawful because it had the effect of frustrating or preventing the ability of parliament to carry out its constitutional functions without reasonable justification.” “Parliament has not been prorogued. This is the unanimous judgment of all 11 justices,” she added. “It is for parliament, and in particular the speaker and the Lords speaker, to decide what to do next.”

Speaker of the House of Commons John Bercow called for Parliament to reconvene. “As the embodiment of our Parliamentary democracy, the House of Commons must convene without delay,” Bercow said in a statement. ” To this end, I will now consult the party leaders as a matter of urgency.”

Johnson responded by insisting that “as the law stands, we leave on October 31 and I am very hopeful that we will get a deal and I think what the people of the country want is to see parliamentarians coming together working in the national interest to get this thing done and that is what we are going to do.”

German Ifo recovered to 94.6, downturn taking a breather

Germany Ifo Business Climate rose to 94.6 in September, up from 94.3 and beat expectation of 94.5. Expectation Index dropped to 90.8, down from 91.3, missed expectations of 91.9. Current Assessment Index rose to 98.5, up from 97.3 and beat expectation of 97.0. Ifo noted that “the downturn is taking a breather” but “outlook for the coming months deteriorated again”.

Looking at the details, Manufacturing Index dropped from -6.0 to -6.4. Service Index rose from 13.0 to 16.6. Trade Index dropped from -2.4 to -3.7. Construction Index rose from 21.5 to 22.2. Ifo warned that manufacturing has “only one direction: downward” and “trade took another slide”.

Bank of Spain slashes 2019 growth forecasts to 2% on weak investment and consumption

Bank of Spain lowered 2019 growth forecasts to 2.0%, sharply lower than June’s projection of 2.4%. For 2020, growth projection was downgraded to 1.7%, from 1.9%. For 2021, growth forecast was also downgraded to 1.6%, from 1.7%. Weaker investment and private consumption were the main factor for the downgrades.

Meanwhile, the central bank also noted risks including European slowdown, Brexit, US-China trade tension as well as domestic political uncertainties. Spain is going to have the fourth parliamentary elections in four years on November 10.

Oscar Arce, the Bank of Spain’s director general for economics, statistics and research said, “Also worth mentioning as a possible risk element is the continuation of uncertainty on the domestic front about the course of main economic policies in this country in the future.”

Aussie recovers as RBA Lowe refrains from signaling imminent rate cut

Australian Dollar recovers after RBA Governor Philip Lowe refrained from signaling an imminent rate cut at next week’s meeting. In a speech, he just noted that “at our Board meeting next week, we will again take stock of the evidence”. And, “the Board is prepared to ease monetary policy further if needed to support sustainable growth in the economy, make further progress towards full employment, and achieve the inflation target over time.”

Low added that the back-to-back rate cuts in June and July were taken to “help make more assured progress towards full employment and the inflation target.” He did acknowledged that “further monetary easing may well be required”. However, “while we are at a gentle turning point and expect growth to up, the strength and durability of this -up remains to be seen.”

BoJ Kuroda: Need to be increasingly vigilant to global slowdown

BoJ Governor Haruhiko Kuroda warned in a speech that “as risks regarding overseas economy are heightening, we need to be increasingly vigilant to the chance the overseas slowdown could affect Japan’s economy and inflation.” Also, “the situation has been changing rapidly, with investors’ risk aversion abating somewhat due to expectations for progress in the U.S.-China trade negotiations.”

Policymakers will scrutinize upcoming economic data at the next policy meeting on October 30-31. Kuroda emphasized that BOJ does not have any preconception at this point” on what policy steps it could take at the meeting. Though, he also acknowledged the need to main the yield curve control policies sustainable. He said “if the current low-interest rate environment is prolonged further, it will become necessary to pay closer attention to the cost of our policy.”

Japan PMI manufacturing dropped to 48.9, strong external headwinds

Japan PMI Manufacturing dropped to 48.9, down from 49.3 and missed expectation of 49.5. That’s also the lowest reading since June 2016. PMI Services dropped to 52.8, down from 53.3. PMI Composite dropped to 51.5, down from 51.9.

Joe Hayes, Economist at IHS Markit, said: “The resilience of Japan’s service sector to the struggles of the country’s manufacturers continued to shine through during September. As a result, it’s looking like Japan will boast what will be a robust rate of growth in the current climate for the third quarter”.

However, “anecdotal evidence further highlighted the strong external headwinds Japanese manufacturers were faced with, namely US-China trade tensions, the Hong Kong protests, Brexit and the diplomatic dispute between Japan and South Korea”. Q4 would be challenging for both businesses and consumers with the planned sales tax hike.

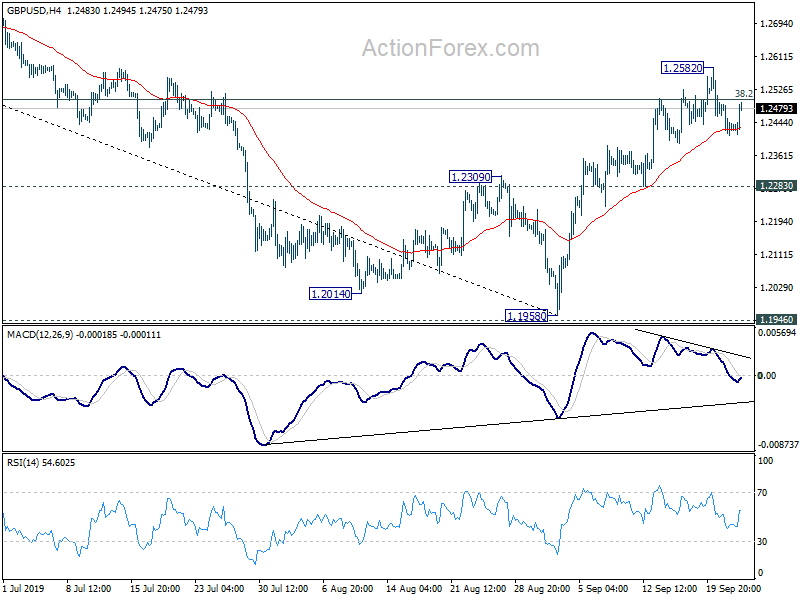

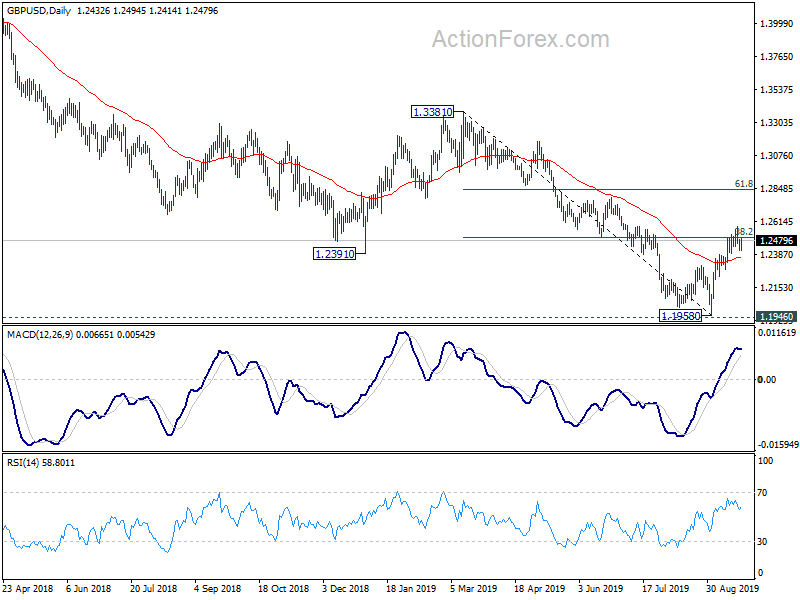

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2401; (P) 1.2446; (R1) 1.2479; More….

GBP/USD drew support from 4 hour 55 EMA and recovered. But upside is limited below 1.2582 temporary top. Intraday bias remains neutral first. On the upside, break of 1.2582 and sustained break of 38.2% retracement of 1.3381 to 1.1958 at 1.2502 will pave the way to 61.8% retracement at 1.2837. However, break of 1.2283 will suggest that rebound from 1.1958 has completed. Intraday bias will be turned back to the downside or retesting 1.1958 low.

In the bigger picture, we’d remain cautious on medium term bottoming around 1.1946 (2016 low). Sustained trading above 55 week EMA (now at 1.2758) will extend the consolidation pattern from 1.1946 with another rise to 1.4376 resistance. Nevertheless, decisive break of 1.1946 will resume down trend from 2.1161 (2007 high) to 61.8% projection of 1.7190 to 1.1946 from 1.4376 at 1.1135.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 00:30 | JPY | Manufacturing PMI Sep | 48.9 | 49.5 | 49.3 | |

| 05:00 | JPY | Leading Index Jul | 93.7 | 93.6 | 93.6 | |

| 08:00 | EUR | German Ifo Business Climate Sep | 94.6 | 94.5 | 94.3 | |

| 08:00 | EUR | German Ifo Expectations Sep | 90.8 | 91.9 | 91.3 | |

| 08:00 | EUR | German Ifo Current Assessment Sep | 98.5 | 97 | 97.3 | |

| 08:30 | GBP | Public Sector Net Borrowing (GBP) Aug | 5.8B | 6.7B | -2.0B | |

| 13:00 | USD | House Price Index M/M Jul | 0.40% | 0.30% | 0.20% | |

| 13:00 | USD | S&P/CS HPI Composite – 20 Y/Y Jul | 2.00% | 2.20% | 2.10% | 2.20% |

| 14:00 | USD | CB Consumer Confidence Sep | 133.8 | 135.1 |

{kind=link}