Australian Dollar drops broadly after RBA cut interest rate as widely expected. The central bank also maintains easing bias, suggesting that the easing cycle might not be over yet. Poor housing data also weight on sentiments. New Zealand Dollar is following as second weakest and then Japanese Yen. On the other hand, Dollar is currently the strongest one, followed by Canadian and then Sterling.

Technically, USD/CHF’s break of 0.9975/83 resistance zone is a solid sign of near term bullishness. Further rally should be seen towards 1.0237 high. EUR/USD is extending medium term down trend to 1.0813 fibonacci level. AUD/USD is on track to retest 0.6677 low. Decisive break there will resume medium term down trend too.

In Asia, China and Hong Kong are on holiday. While China is celebrating its 70th anniversary, large scale protest continues in Hong Kong, with a peaceful march involving hundreds of thousands of people. Nikkei is currently up 0.72%. Singapore Strait Times is up 1.04%. Overnight, DOW rose 0.36%. S&P 500 rose 0.50%. NASDAQ rose 0.75%. 10-year yield was flat at 1.675.

RBA cut to 0.75%, maintains easing bias

RBA cut cash rate by -25bps to 0.75% as widely expected. The central bank also maintained easing bias. It noted that “the Board will continue to monitor developments, including in the labour market, and is prepared to ease monetary policy further if needed to support sustainable growth in the economy, full employment and the achievement of the inflation target over time.”

In the accompanying statement, RBA also noted that risks global outlook are “tilted to the downside” as US-China disputes are “affecting international trade flows and investment”. Domestically, 1.4% GDP growth in Q2 was “weaker-than-expected”, but appeared to have reached a “gentle turning point”. Forward looking indicators suggest employment is likely to “slow from its recent fast rate” while wages growth remains “subdued”. “Taken together, recent outcomes suggest that the Australian economy can sustain lower rates of unemployment and underemployment.” Inflation also remained “subdued” and is “likely to be the case for some time yet”.

Australia AiG manufacturing rose to 54.7, employment and new orders accelerate

Australia AiG Performance of Manufacturing Index rose 1.6 pts to 54.7 in September, suggesting faster growth across the sector. Employment and new orders accelerate, driven by continued strength in the ‘food & beverages’ sector along with a resurgence in ‘machinery & equipment’ manufacturing. Manufacturers servicing the mining and defence sectors reported buoyant conditions. Weakness remains in the ‘metals’ and ‘TCF, paper & printing’ sectors while the ‘building materials, wood, furniture & other’ manufacturing sector reported slower conditions.

Also released, Australian building permits dropped -1.1% mom in August, well below expectation of 2.5% mom rise.

Japan Tankan large manufacturing index dropped to lowest since 2013, but beat expectations

Japan Tankan large manufacturing index dropped to 5 in Q3, down from 7 but beat expectation of 2. That’s the third straight quarter of decline and was the lowest level since June 2013. Large manufacturing outlook also dropped to 2, down from 7 but beat expectation of 1. Non-manufacturing index dropped to 21, down from 23 and beat expectation of 20. Non-manufacturing outlook dropped to 15, down from 17, but missed expectation of 16. Large all industry capex rose 6.6%, slowed from 7.4% and missed expectation of 7.0%.

The data suggested that business confidence worsened as global slowdown and trade tensions weighed. Yet, the deteriorations were not as bad as expected and capital expenditure were still holding up. The data could be neutral to BoJ’s policy. That is, they might not add enough pressure to additional easing from the central bank.

Also released, unemployment rate was unchanged at 2.2% in September, better than expectation of 2.3%.

Japan PMI manufacturing finalized at 48.9, manufacturing and exports drag on Q3 GDP

Japan PMI Manufacturing was finalized at 48.9 in September, down from 49.3 in August. That’s also the lowest level since February. Output reduced as deterioration in demand extends into September. Firms link export weakness to lower sales to China, US and Europe. Business expectations remain historically subdued.

Joe Hayes, Economist at IHS Markit, said: Crucially, the stronger deterioration comes ahead of the consumption tax hike, and suggests that manufacturing and exports are both likely to have been drags on third quarter GDP. Japan continues to suffer from the trade-led global growth slowdown… Strength in the trade-weighted yen so far this year has also meant that the currency has not been able to mitigate the impact of the global trade slowdown. To that end, the service sector’s ability to weather the sales tax hike in the fourth quarter will be crucial to keeping the economy afloat into the year-end.”

Looking ahead

Eurozone CPI will be a focus while PMI manufacturing final will be featured. UK will release PMI manufacturing. Swiss will release SVME PMI and retail sales. Later in the day, US ISM manufacturing will be the major focus while Canada GDP will also be released.

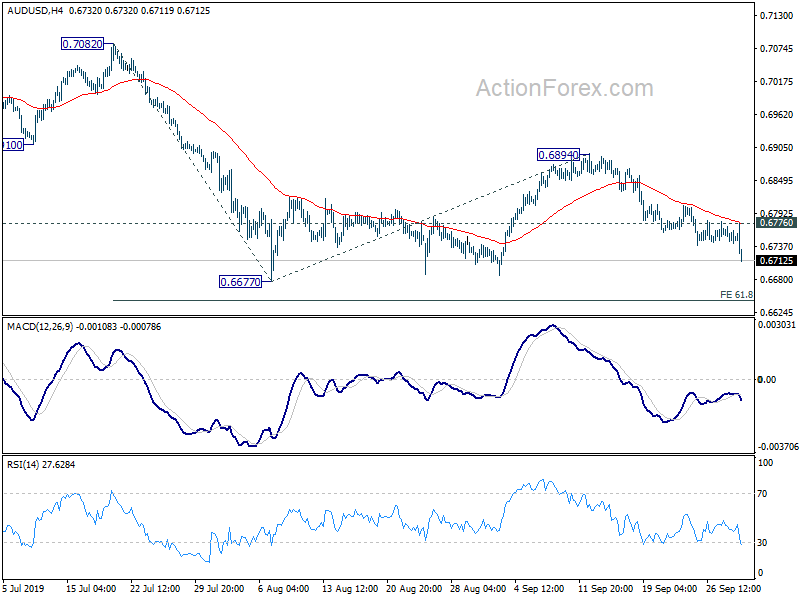

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.6737; (P) 0.6754; (R1) 0.6766; More…

Intraday bias in AUD/USD remains on the downside as fall from 0.6894 is extending. Decisive break of 0.6677 low will resume larger down trend. Next near term target is 61.8% projection of 0.7082 to 0.667 from 0.6894 at 0.6644 and then 100% projection at 0.6489. On the upside, 0.6776 minor resistance will turn intraday bias neutral first. But risk will stay on the downside as long as 0.6894 resistance holds.

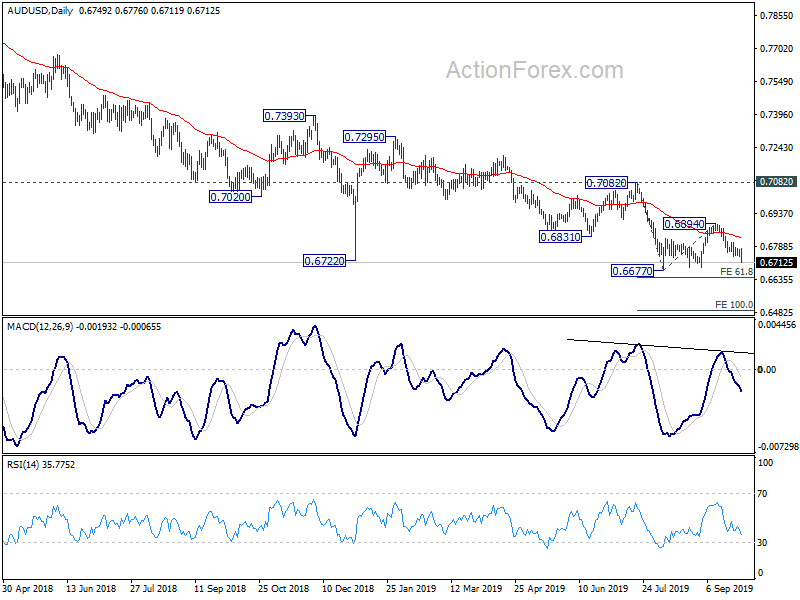

In the bigger picture, decline from 0.8135 (2018 high) is seen as resuming the long term down trend from 1.1079 (2011 high). Next target is 0.6008 (2008 low). On the upside, break of 0.7082 resistance is needed to be the first sign of medium term bottoming. Otherwise, outlook will remain bearish even in case of strong rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:00 | NZD | NZIER Business Confidence Q3 | -35 | -34 | ||

| 22:30 | AUD | AiG Performance of Mfg Index Sep | 54.7 | 53.1 | ||

| 23:30 | JPY | Unemployment Rate Aug | 2.20% | 2.30% | 2.20% | |

| 23:50 | JPY | Tankan Large Manufacturing Index Q3 | 5 | 2 | 7 | |

| 23:50 | JPY | Tankan Large Manufacturing Outlook Q3 | 2 | 1 | 7 | |

| 23:50 | JPY | Tankan Non-Manufacturing Index Q3 | 21 | 20 | 23 | |

| 23:50 | JPY | Tankan Non – Manufacturing Outlook Q3 | 15 | 16 | 17 | |

| 23:50 | JPY | Tankan Large All Industry Capex Q3 | 6.60% | 7.00% | 7.40% | |

| 00:30 | JPY | Jibun Bank Manufacturing PMI Sep F | 48.9 | 48.9 | 48.9 | |

| 01:30 | AUD | Building Permits M/M Aug | -1.10% | 2.50% | -9.70% | |

| 04:30 | AUD | RBA Rate Decision | 0.75% | 0.75% | 1.00% | |

| 06:00 | GBP | Nationwide Housing Prices M/M Sep | 0.10% | 0.00% | ||

| 06:30 | CHF | Real Retail Sales Y/Y Aug | 1.60% | 1.40% | ||

| 07:30 | CHF | SVME – PMI Sep | 46.5 | 47.2 | ||

| 07:45 | EUR | Italy Manufacturing PMI Sep | 47.9 | 48.7 | ||

| 07:50 | EUR | France Manufacturing PMI Sep F | 50.3 | 50.3 | ||

| 07:55 | EUR | Germany Manufacturing PMI Sep F | 41.4 | 41.4 | ||

| 08:00 | EUR | Manufacturing PMI Sep F | 45.6 | 45.6 | ||

| 08:30 | GBP | Manufacturing PMI Sep | 47 | 47.4 | ||

| 09:00 | EUR | CPI Y/Y Sep P | 1.00% | 1.00% | ||

| 09:00 | EUR | CPI – Core Y/Y Sep P | 1.00% | 0.90% | ||

| 12:30 | CAD | GDP M/M Jul | 0.00% | 0.20% | ||

| 13:30 | CAD | Manufacturing PMI Sep | 50.4 | 49.1 | ||

| 13:45 | USD | Manufacturing PMI Sep F | 51 | 51 | ||

| 14:00 | USD | ISM Manufacturing PMI Sep | 50.4 | 49.1 | ||

| 14:00 | USD | ISM Prices Paid Sep | 50.5 | 46 | ||

| 14:00 | USD | Construction Spending M/M Aug | 0.30% | 0.10% |

{kind=link}