Dollar and Yen are generally softer today following notable rebound in German and US treasury yields. ECB meeting accounts confirmed the divided opinion among policy makers on the stimulus package, in particular QE. That gives a strong support in both Euro and German bund yields. Meanwhile, solid core CPI from US also support US yields. Yet, markets are cautiously awaiting top-level US-China trade talks, which finally starts today.

Chinese Vice Premier Liu He was quoted saying that the team came with “great sincerity, willing to cooperate with the U.S. on the trade balance, market access and investor protection”. He also hoped to prevent further escalation in trade tensions. But there were also reports noting that China is not going to offer any resolution to core issues, including intellectual property theft, forced technology transfer, subsidies to state-owned enterprises and enforcement of the agrement. It remains to be seen whether the two day meetings would end with some progress or just an old deadlock.

In other markets, DOW open up and is trading up 0.7% at the time of writing. FTSE is up 0.21%. DAX is flat. CAC is up 0.37%. German 10-year yield is up 0.0698 at -0.476. Earlier in Asia, Nikkei rose 0.45%. Hong Kong HSI rose 0.10%. China Shanghai SSE rose 0.78%. Singapore Strait Times dropped -0.01%. Japan 10-year JGB yield dropped -0.0067 to -0.212.

US CPI unchanged at 1.7%, core CPI unchanged at 2.4%

In September, US CPI was flat mom versus expectation of 0.1% mom rise. Core CPI rose 0.1% mom versus expectation of 0.2% mom. Annually, headline CPI was unchanged at 1.7% yoy, below expectation of 1.8% yoy. Core CPI was also unchanged at 2.4%, matched expectations.

Initial jobless claims dropped -10k to 210k in the week ending October 5, below expectation of 217k. Four-week moving average of initial claims rose 1k to 213.75k. Continuing claims rose 29k to 1.684m in the week ending September 28. Four-week moving average of continuing claims rose 2.5k to 1.665m.

ECB accounts: A number of reservations expressed about elements of stimulus package

Accounts of September 11-12 ECB policy meeting showed rather wide division in opinion regarding the new stimulus package. That was inline with comments from ECB officials after that meeting. The accounts noted, “a number of reservations were expressed about individual elements of the proposed policy package”. Also, “although the rational for a comprehensive package was widely shared, members assessed the case for specific elements differently, with some measures seen as substitutes rather than compliments.”

In particular, while here was a “clear majority” favoring restart of QE, “a number of members assessed the case for renewed net asset purchases as not sufficiently strong”. QE was deemed to be a “less efficient instrument, or “an instrument of last resort”. The cut in deposit rate to -0.5% was passed by a “very large majority”. But, “lower money market trading volumes for longer tenors suggested that the conviction about cuts significantly deeper into negative territory was not broad-based and uncertainty over the future path of short-term policy rates remained elevated.”

UK GDP contracted -0.1% mom, production shrank sharply

UK GDP contracted -0.1% mom in August, below expectation of 0.0% mom. Looking at the details, Services was flat mom. Production dropped sharply by -0.6% mom. Manufacturing contracted -0.7% mom. Construction rose 0.2% mom. Agriculture dropped -0.1% mom. In the three months to August, rolling GDP grew 0.3%, but that’s mainly because of the growth back in July. Services was the main drive in the three-month GDP growth, up 0.4% 3mo3m. Production contracted -0.4$ 3mo3m. Construction grew 0.1% 3mo3m.

Also from UK, manufacturing production dropped -0.7% mom, 1.7% yoy in August, much worse than expectation of -0.1% mom, -0.7% yoy. Industrial production dropped -0.6% mom, -1.8% yoy, also much worse than expectation of -0.1% mom, -1.1% yoy. Goods trade deficit widened slightly to GBP -9.8B.

NIESR: UK GDP to grow 0.5% in Q3, 0.3% in Q4

NEISR said that UK economy is on course to grow by 0.5% in Q3, then slow to 0.3% in Q4. And that would be consistent with 1.3% GDP in 2019 as a whole, just slightly down fro 1.3% in 2018.

Garry Young, Director of Macroeconomic Modelling and Forecasting: “Despite better than expected GDP data, the underlying pace of growth in the United Kingdom is slow. The strongest source of private sector demand is household consumption, driven by real wage growth, but this is not sustainable without a pick-up in productivity growth, and this seems unlikely in the near term.”

German export shrank as trade war continued to weigh

In August, German exports dropped -3.9% yoy to EUR 101.2B while exports dropped -3.1% yoy to EUR 85.0B. Trade surplus came in at EUR 16.0B. In calendar and seasonally adjusted terms, exports dropped -1.8% mom while imports rose 0.5% mom. Trade surplus narrowed to EUR 18.1B.

The slump in export is seen as another evidence of impact from trade wars, which continued to drag on the economy. Continued weakness in manufacturing and exports point to another quarter of GDP contraction, following Q2’s -0.1% qoq. German economy was likely in recession already.

Elsewhere

Japan bank lending rose 2.0% yoy in September, matched expectations. PPI dropped to -1.1% yoy, but beat expectation of -1.2% yoy. Machinery orders dropped -2.4% mom in August, above expectation of -2.5% yoy. From Australia, home loans rose 1.8% in August, missed expectation of 3.6%. But consumer inflation expectations accelerated to 3.6%, above expectation of 3.2%.

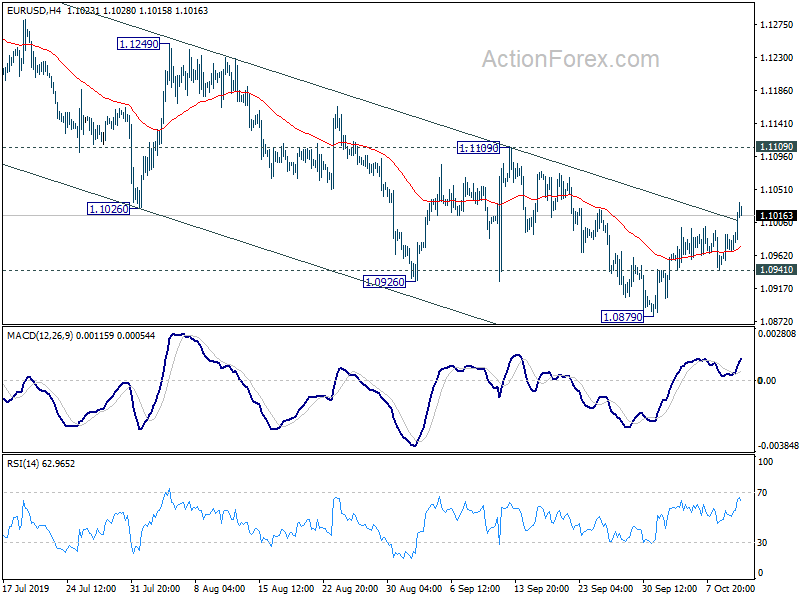

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0951; (P) 1.0971; (R1) 1.0989; More…

EUR/USD’s rebound from 1.0879 extends higher today and further rise could be seen. But still, upside should be limited by 1.1109 resistance to bring larger down trend resumption. On the downside, break of 1.0941 will turn bias back to the downside for retesting 1.0879 low first. However, firm break of 1.1109 will be an early sign of medium term bottoming and target 1.1412 key resistance next.

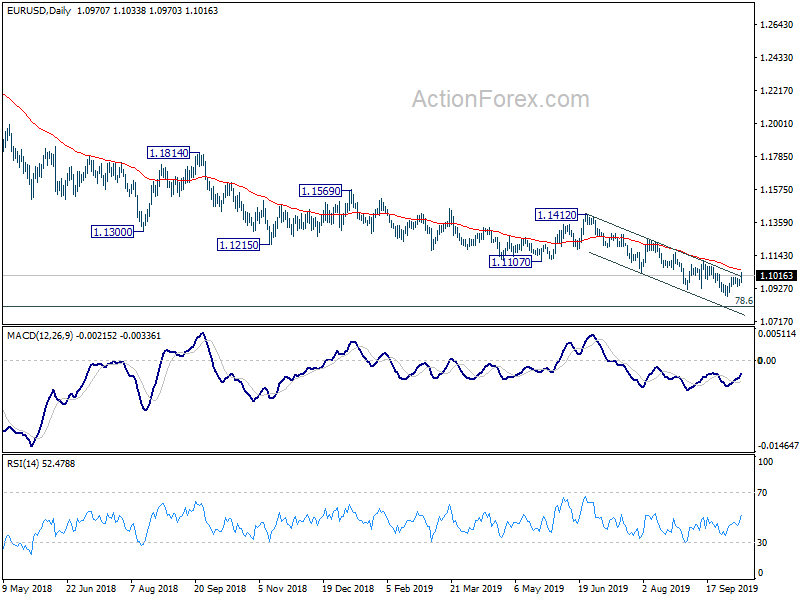

In the bigger picture, down trend from 1.2555 (2018 high) is in progress. Prior rejection of 55 week EMA also maintained bearishness. Further fall should be seen to 78.6% retracement of 1.0339 to 1.2555 at 1.0813. Decisive break there will target 1.0339 (2017 low). On the upside, break of 1.1412 resistance is needed to confirm medium term bottoming. Otherwise, outlook will stay bearish in case of rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | Food Price Index M/M Sep | 0.00% | -0.20% | 0.70% | |

| 23:01 | GBP | RICS Housing Price Balance Sep | -2% | -7% | -4% | |

| 23:50 | JPY | Bank Lending Y/Y Sep | 2.00% | 2.00% | 2.10% | |

| 23:50 | JPY | PPI M/M Sep | 0.00% | -0.10% | -0.30% | |

| 23:50 | JPY | PPI Y/Y Sep | -1.10% | -1.20% | -0.90% | |

| 23:50 | JPY | Machinery Orders M/M Aug | -2.40% | -2.50% | -6.60% | |

| 00:00 | AUD | Consumer Inflation Expectations Oct | 3.60% | 3.20% | 3.10% | |

| 00:30 | AUD | Home Loans Aug | 1.80% | 3.60% | 5.00% | 5.50% |

| 06:00 | EUR | Germany Trade Balance (EUR) Aug | 18.1B | 19.4B | 20.2B | 20.5B |

| 06:45 | EUR | France Industrial Output M/M Aug | -0.90% | 0.40% | 0.30% | |

| 08:00 | EUR | Italy Industrial Output M/M Aug | 0.30% | -1.90% | -0.70% | -0.80% |

| 08:30 | GBP | Manufacturing Production M/M Aug | -0.70% | -0.10% | 0.30% | |

| 08:30 | GBP | Manufacturing Production Y/Y Aug | -1.70% | -0.70% | -0.60% | -0.90% |

| 08:30 | GBP | Industrial Production M/M Aug | -0.6 | -0.10% | 0.10% | |

| 08:30 | GBP | Industrial Production Y/Y Aug | -1.80% | -1.10% | -0.90% | -1.10% |

| 08:30 | GBP | Index of Services 3M/3M Aug | 0.40% | 0.10% | 0.20% | |

| 08:30 | GBP | Goods Trade Balance (GBP) Aug | -9.8B | -10.0B | -9.1B | |

| 08:30 | GBP | GDP M/M Aug | -0.10% | 0.00% | 0.30% | |

| 11:30 | EUR | ECB Monetary Policy Meeting Accounts | ||||

| 12:30 | USD | Initial Jobless Claims (Oct 4) | 210K | 217K | 219K | 220K |

| 12:30 | USD | CPI M/M Sep | 0.00% | 0.10% | 0.10% | |

| 12:30 | USD | CPI Y/Y Sep | 1.70% | 1.80% | 1.70% | |

| 12:30 | USD | CPI Core M/M Sep | 0.10% | 0.20% | 0.30% | |

| 12:30 | USD | CPI Core Y/Y Sep | 2.40% | 2.40% | 2.40% | |

| 12:30 | CAD | New Housing Price Index M/M Aug | 0.10% | 0.00% | -0.10% | |

| 14:30 | USD | Natural Gas Storage | 95B | 112B |

{kind=link}