Yen, Swiss Franc and Dollar continue to regain some grounds today as markets reassess US-China trade negotiations developments. New Zealand Dollar, Sterling and Australian Dollar are generally softer too. But overall trading is rather subdued with Japan, US and Canada on holiday. Today’s price actions are, for now, generally seen as consolidative. That is, Sterling strength and Yen weakness are expected to resume after traders are back.

Technically, some consolidations are likely in Sterling pairs for now. But GBP/USD’s retreat should be held well above 1.2195 support. GBP/JPY should be held well above 130.42 support. EUR/GBP should be capped well below 0.9019 resistance. EUR/USD and AUD/USD are two pairs to watch ahead. Both are seen as in corrective recoveries, which appear to lose upside momentum. Break of 1.0941 support in EUR/USD and 0.6710 support in AUD/USD should bring retest of recent lows.

In Europe, currently, FTSE is down -0.49%. DAX is down -0.46%. CAC is down -0.56%. German 10-year yield is down -0.024 at -0.463. Earlier in Asia, Hong Kong HSI rose 0.81%. China Shanghai SSE rose 1.15%. Singapore Strait Times rose 0.34%. Japan was on holiday.

US Mnuchin: If there is no trade deal with China, tariffs would go in place

US Treasury Secretary Steven Mnuchin told CNBC today that he expected President Donald Trump and Chinese President Xi Jinping will be able to finish the trade agreement during their anticipated meeting in Chile on November 16-17. He also echoed Trump’s comments last week and said recent round of discussions covered intellectual property rights, financial services including currency and foreign exchange, and “very significant structural issues” dealing with agriculture. Though, Mnuchin also warned, “I have every expectation if there’s not a deal those tariffs would go in place”, referring to the next round of tariffs scheduled to mid-December.

On the other hand, Chinese media sounded much less enthusiastic, as Trump. On Sunday, China Daily said, “while the negotiations do appear to have produced a fundamental understanding on the key issues and the broader benefits of friendly relations, the Champagne should probably be kept on ice, at least until the two presidents put pen to paper.” It also warned, “as based on its past practice, there is always the possibility that Washington may decide to cancel the deal if it thinks that doing so will better serve its interests.”

Eurozone industrial production rose 0.4% mom, above expectation of 0.3% mom

Eurozone industrial production rose 0.4% mom in August, above expectation of 0.3% mom. Annually, Eurozone industrial production dropped -2.8% yoy. Production of capital goods rose by 1.2% mom and intermediate goods by 0.3% mom, while production of non-durable consumer goods fell by -0.3% mom, and durable consumer goods and energy by -0,4% mom.

EU28 industrial production came in at 0.1% mom, -2.0% yoy. Among Member States for which data are available, the highest increases in industrial production were registered in Malta (5.6% mom), Estonia (3.9% mom) and Latvia (3.0% mom). The largest decreases were observed in Croatia (-3.0% mom), Slovakia (-2.6% mom) and Lithuania (-2.4% mom).

ECB de Guindos didn’t foresee recession in Eurozone

ECB Vice President Luis de Guindos said he didn’t foresee Eurozone entering into recession. However, low growth could extend for a longer time. Meanwhile, latest news regarding US-China trade negotiations were positive. De Guindos also warned that low profitability of banks would lead to low valuation, “making the inevitable consolidation of the sector very difficult.” Low profitability of Eurozone banks was also related to costly structures and excess capacity.

Separately over the weekend, ECB policymaker Robert Holzmann complained that the current ECB monetary policy is “wrong” and “a different policy is needed in the future”. He added that ECB should think about lowering inflation target, temporarily, from 2% to 1.5%. Also, “I am convinced that she has heard the dissenting voices, that she will take them seriously and will try to find a new approach here.”

Germany’s Economy Ministry expects stagnation but not recession

Germany’s Economy Ministry said “the export-oriented German industry is facing weak global trade, stagnating global manufacturing and falling demand for cars.” However, “a stronger slowdown or a pronounced recession are not to be expected at the moment”. Instead, “the German economy remains in stagnation. Economic activity is stuck at the existing level.”

So far, growth in services and construction has largely offset the recession in manufacturing sector. But, considering recent indicators, there are increasing signs of spill over, which could further drag the labor market overall.

The government is expected to publish new economic forecasts this week. In April, it predicted growth of 0.5% for 2019 and 1.5% for 2020. There is some room for downside recession in 2020’s figure.

China imports and exports contracted deeply in Sept

China’s September trade data were rather poor. In particular, imports dropped -8.5% yoy versus expectation of -5.2% yoy,. suggesting weak domestic demand. Exports also contracted -3.2% yoy versus expectation of -3.0% yoy. Trade surplus widened to USD 39.7B. But year-to September, exports just dropped -0.1% yoy while imports dropped -5.0% yoy.

In USD term, in September: Total trade dropped -5.7% yoy to USD 396.6B. Exports dropped -3.2% yoy to USD 218.1B. Imports dropped -8.5% yoy to USD 178.5B. Trade surplus came in at USD 39.7B.

Year-to-September: Total trade dropped -2.4% yoy to USD 3351.8B. Exports dropped -0.1% yoy to USD 1825.1B. Imports dropped -5.0% yoy to USD 1526.7B. Trade surplus was at USD 298.4B.

With US, Year-to-September: Total trade dropped -14.8% yoy to USD 402.7B. Exports to US dropped -10.7% yoy to USD 312.0B. Imports from US dropped -26.4% yoy to USD 90.7B. Trade surplus was at USD 221.3B.

With EU, Year-to September: Total trade rose 3.2% yoy to USD 522.5B. Exports rose 5.1% yoy to USD 316.8B. Imports rose 0.3% yoy to USD 205.8B. Trade surplus was at USD 111.0B

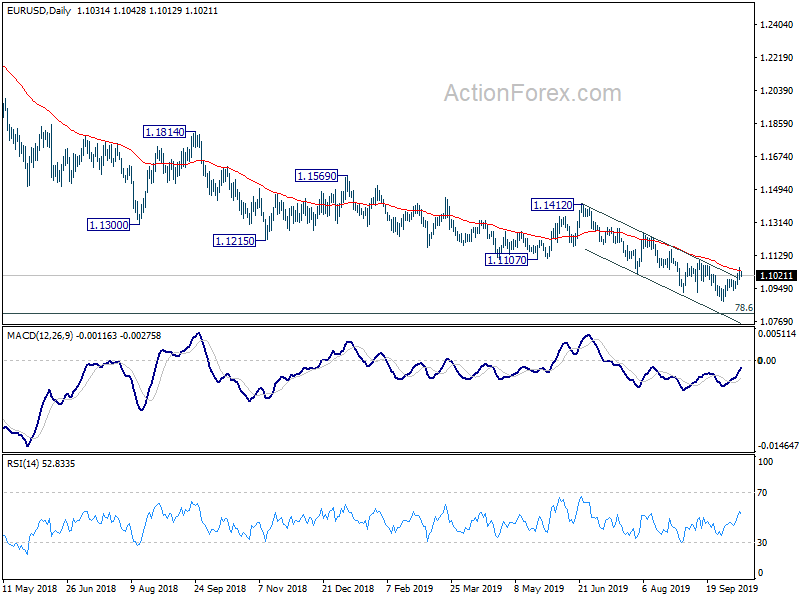

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1004; (P) 1.1034; (R1) 1.1066; More…

No change in EUR/USD’s outlook as corrective recovery from 1.0879 could still extend. But upside should be limited by 1.1109 resistance to bring down trend resumption. On the downside, break of 1.0941 minor support should confirm completion of the recovery and turn bias to the downside for retesting 1.0879 low first. However, firm break of 1.1109 will be an early sign of medium term bottoming and target 1.1412 key resistance next.

In the bigger picture, down trend from 1.2555 (2018 high) is in progress. Prior rejection of 55 week EMA also maintained bearishness. Further fall should be seen to 78.6% retracement of 1.0339 to 1.2555 at 1.0813. Decisive break there will target 1.0339 (2017 low). On the upside, break of 1.1412 resistance is needed to confirm medium term bottoming. Otherwise, outlook will stay bearish in case of rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 3:00 | CNY | Trade Balance USD Sep | 39.7B | 35.1B | 34.8B | |

| 3:00 | CNY | Imports Y/Y Sep | -8.50% | -5.20% | -5.60% | |

| 3:00 | CNY | Exports Y/Y Sep | -3.20% | -3.00% | -1.00% | |

| 3:00 | CNY | Trade Balance CNY Sep | 275B | 254B | 240B | |

| 3:00 | CNY | Exports Y/Y CNY Sep | -0.70% | 2.60% | ||

| 3:00 | CNY | Imports Y/Y CNY Sep | -6.20% | -2.60% | ||

| 9:00 | EUR | Industrial Production M/M Aug | 0.40% | 0.30% | -0.40% |

{kind=link}