Global equities tumbled broadly while treasury yields surged as investors are preparing themselves to enter into an era of monetary stimulus removal. DOW lost -0.78% to close at 21287.03, S&P 500 down -0.86% to 2419.70, and NASDAQ dropped -1.44% to 6144.35. That was preceded by the -0.51% fall in FTSE, -1.83% fall in DAX and -1.88% fall in CAC. US 10 year yields followed global yields higher and closed up 0.046 at 2.267, breaking 2.229 near term resistance. In Asian markets, Nikkei followed by losing -1.06% to 20006.88, just barely hold on to 20000 handle. In currency markets, Yen and Dollar recovered mildly but are still set to end the week as the weakest major currencies. Sterling, Canadian and Euro remained the strongest ones and supported by respective hawkish central banks.

We’ve pointed out in Wednesday’s report that NASDAQ is starting the third leg of the correction pattern from 6341.70. And it’s happening now despite Thursday’s recovery. Focus stays on 55 day EMA (now at 6119.60). Sustained break there will also have medium term channel support taken out. That will bring deeper fall to 38.2% retracement of 5034.31 to 6341.70 at 5842.31. Such development will also drag on other indices. DOW also looks vulnerable considering bearish divergence condition in daily MACD. Near term focus is also on 55 day EMA (now at 12075.12). Firm break there would bring deeper pull back to 20379.55 support.

US economy clouded by political drama

Outlook of the US economy and markets are clouded by political drama. There are just so many distractions that doubts are high on whether US President Donald Trump can push through his economic policies. The so called "watered-down" travel ban 2.0n took effect yesterday. But just an hour ahead of that, the state of Hawaii filed an emergency motion in the federal court to contest the plan. Meanwhile, it seems like Senate Republicans are still working on voting on the healthcare act before the Fourth of July recess. But, no good news is heard by the market regarding this so far. And businesses and investors are awaiting the completion of the healthcare act so that Trump administration can finally start working on passing the tax reforms.

On the data front

In Japan, National CPI core rose to 0.4% yoy in May, up from 0.3% yoy and met expectations. But that’s still way off BoJ’s 2% target. Tokyo CPI core, on the other hand, dropped to 0.0% yoy in June, down from 0.1% yoy and missed expectation of 0.2% yoy. Also from Japan, unemployment rate rose to 3.1% in May, household spending dropped -0.1% yoy, industrial production dropped -3.3% mom, housing starts dropped -0.3% yoy. Saying in Asia pacific, New Zealand building permits rose 7.0% mom in May.

Elsewhere, German retail sales rose 0.5% mom in May. UK Gfk consumer confidence dropped to -10 in June. Swiss KOF leading indicator, German unemployment and UK Q1 GDP final will be released in European session. But main focus will be on Eurozone CPI flash. Later in the day, Canada will release GDP, IPPI and RMPI. US will release personal income and spending and Chicago PMI.

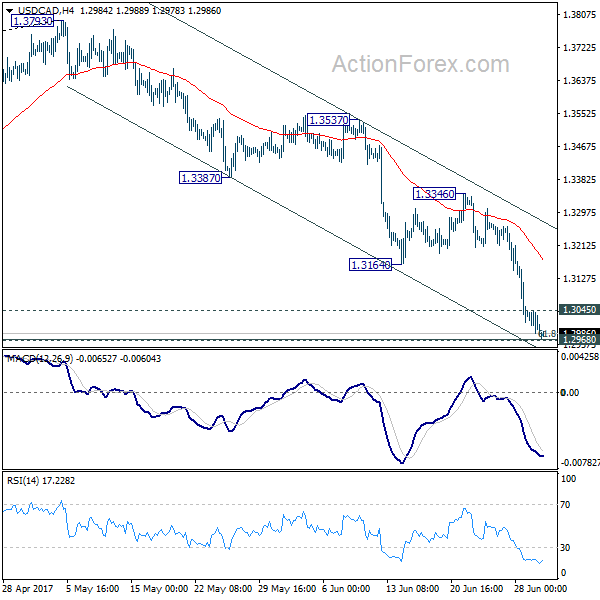

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2978; (P) 1.3010; (R1) 1.3035; More….

USD/CAD fall continues and reaches as low as 1.2971 so far, just inch above 1.2968 cluster support, 61.8% retracement of 1.2460 to 1.3793 at 1.2969. There is no sign of bottoming yet and intraday bias remains on the downside. As noted before, corrective rise from 1.2460 has completed at 1.3793. Sustained break of 1.2968/69 will pave the way to retest 1.2460 low. On the upside, above 1.3045 minor resistance will argue that a short term bottom could be in place after drawing support from 1.2968/69. In such case, intraday bias will be turned back to the upside for recovery back to 1.3164 support turned resistance.

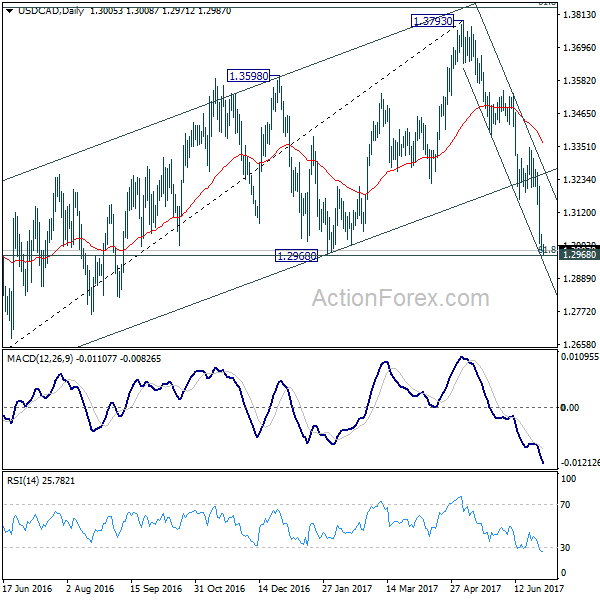

In the bigger picture, price actions from 1.4689 medium term top are seen as a correction pattern. The first leg has completed at 1.2460. Rise from 1.2460 is seen as the second leg and has completed at 1.3793, ahead of 61.8% retracement of 1.4689 to 1.2460 at 1.3838. Break of 1.3222 should now indicate the start of the third leg while further break of 1.2968 should confirm. In that case, USD/CAD should decline through 1.2460 support to 50% retracement of 0.9406 to 1.4869 at 1.2048.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Building Permits M/M May | 7.00% | -7.60% | -7.40% | |

| 23:01 | GBP | GfK Consumer Confidence Jun | -10 | -7 | -5 | |

| 23:30 | JPY | Jobless Rate May | 3.10% | 2.80% | 2.80% | |

| 23:30 | JPY | Household Spending Y/Y May | -0.10% | -0.50% | -1.40% | |

| 23:30 | JPY | National CPI Core Y/Y May | 0.40% | 0.40% | 0.30% | |

| 23:30 | JPY | Tokyo CPI Core Y/Y Jun | 0.00% | 0.20% | 0.10% | |

| 23:50 | JPY | Industrial Production M/M May P | -3.30% | -3.00% | 4.00% | |

| 1:00 | CNY | Manufacturing PMI Jun | 51.7 | 51 | 51.2 | |

| 1:00 | CNY | Non-manufacturing PMI Jun | 54.9 | 54.5 | ||

| 5:00 | JPY | Housing Starts Y/Y May | -0.30% | -0.70% | 1.90% | |

| 6:00 | EUR | German Retail Sales M/M May | 0.50% | 0.30% | -0.20% | |

| 7:00 | CHF | KOF Leading Indicator Jun | 102.5 | 101.6 | ||

| 7:55 | EUR | German Unemployment Change Jun | -10k | -9k | ||

| 7:55 | EUR | German Unemployment Rate Jun | 5.70% | 5.70% | ||

| 8:30 | GBP | Current Account (Pounds) Q1 | -16.5B | -12.1B | ||

| 8:30 | GBP | GDP Q/Q Q1 F | 0.20% | 0.20% | ||

| 8:30 | GBP | GDP Y/Y Q1 F | 2.00% | 2.00% | ||

| 8:30 | GBP | Index of Services 3M/3M Apr | 0.30% | 0.20% | ||

| 9:00 | EUR | Eurozone CPI Estimate Y/Y Jun | 1.20% | 1.40% | ||

| 9:00 | EUR | Eurozone CPI – Core Y/Y Jun A | 1.00% | 0.90% | ||

| 12:30 | CAD | GDP M/M Apr | 0.20% | 0.50% | ||

| 12:30 | CAD | Industrial Product Price M/M May | 0.60% | |||

| 12:30 | CAD | Raw Materials Price Index M/M May | 1.60% | |||

| 12:30 | USD | Personal Income May | 0.30% | 0.40% | ||

| 12:30 | USD | Personal Spending May | 0.10% | 0.40% | ||

| 12:30 | USD | PCE Deflator M/M May | -0.10% | 0.20% | ||

| 12:30 | USD | PCE Deflator Y/Y May | 1.50% | 1.70% | ||

| 12:30 | USD | PCE Core M/M May | 0.10% | 0.20% | ||

| 12:30 | USD | PCE Core Y/Y May | 1.40% | 1.50% | ||

| 13:45 | USD | Chicago PMI Jun | 58 | 59.4 | ||

| 14:00 | USD | U. of Michigan Confidence Jun F | 94.5 | 94.5 |