Sterling drops broadly today after two BoE policy makers surprisingly voted for a rate cut, even though the central eventually stood pat. Following the Pound, Yen is the second weakest as risk appetite returns. Market sentiments were lifted after China said they agreed on phased rollback of tariffs with US for phase one trade agreement. Australian Dollar is currently the strongest one, followed by Canadian.

Technically, while the Pound weakens today, GBP/USD, GBP/JPY and EUR/GBP are still considered in consolidation pattern. Selloff in GBP/USD and GBP/JPY should be contained above 1.2582 and 135.74 support respectively. EUR/GBP’s rebound should also be limited below 0.8811. While USD/JPY and EUR/JPY rebounds, they’re still bounded below 109.28 and 121.46 temporary tops. more consolidations could be seen before a breakout.

In Europe, FTSE is currently up 0.44%. DAX is up 0.74%. CAC is up 0.23%. German 10-year yield is up 0.0578 at -0.274, back above -0.3 handle. Earlier in Asia, Nikkei rose 0.11%. Hong Kong HSI rose 0.57%. China Shanghai SSE closed flat. Singapore Strait Times rose 0.71%. Japan 10-year JGB yield closed flat at -0.086.

BoE kept bank rate at 0.75%, Haskel and Saunders voted for rate cut

BoE left Bank Rate unchanged at 0.75% as widely expected while asset purchase target is held at GBP 435B. However, the vote on policy rate was no unanimous, by 7-2. Two members (Jonathan Haskel and Michael Saunders) voted against the proposition, preferring to reduce Bank Rate by 25 basis points to 0.50%.

However, the accompanying statement still noted that provided that risks on Brexit and global growth do not materialize, and the economy recovers broadly in line with latest projections, “some modest tightening of policy, at a gradual pace and to a limited extent, may be needed to maintain inflation sustainably at the target.”

In the new economic projections published in the Monetary Policy Report, BoE projects GDP growth to pick up from 1.0% in 2019 Q4, to 1.5% in 2020 Q4, 1.8% in 2021 Q4 and 2.1% in 2022 Q4. Inflation is forecast to remain subdued at 1.4% in 2019 Q4 , and 1.5% in 2020 Q4. Though, CPI could finally hit target at 2.0% in 2021 Q4 and then 2.2% in 2022 Q4.

The path of Bank Rate implied for forward market interest rate would drop from 0.7% to 0.5% in 2020 Q4, and stay there throughout the projection horizon.

EU downgrades Eurozone growth forecast, protracted period of subdued growth and muted inflation

In the latest economic projections released today, European Commission downgraded growth forecasts as “the external environment has become much less supportive and uncertainty is running high”. And, this is “particularly affecting the manufacturing sector, which is also experiencing structural shift”. European economy looks to be “heading towards a protracted period of more subdued growth and muted inflation.”

Eurozone GDP is forecast to grow by 1.1% in 2019 (down from summer forecast of 1.2%), 1.2% in 2020 (down from 1.4%) and 1.2% in 2021. For EU as a whole, GDP is expected to grow 1.4% in 2019, 2020 (down from 1.6%) and 2021. Eurozone HICP is forecast at 1.2% in 2019, rising to just 1.3% in 2021.

Valdis Dombrovskis, Vice-President said: “We could be facing troubled waters ahead: a period of high uncertainty related to trade conflicts, rising geopolitical tensions, persistent weakness in the manufacturing sector and Brexit.” Pierre Moscovici, Commissioner for Economic and Financial Affairs, Taxation and Customs, said: “The challenging road ahead leaves no room for complacency. All policy levers will need to be used to strengthen Europe’s resilience and support growth.”

ECB bulletin: Extra Eurozone exports stagnated, intra Eurozone trade weakened further

ECB Monthly Bulletin noted that global survey indications suggest “subdued” economic activity, “but stabilizing”. Risks to global outlook “remain to the downside” amid a “further escalation of trade disputes, high uncertainty related to Brexit and a potentially slower recovery in a number of emerging market economies.” Also, global trade momentum is “expected to remain muted”, as higher tariffs are set to come fully into effect at the end of the year.

Domestically, recent data continue to point to “positive but moderate employment growth” in Eurozone. Rising employment should support household income and consumer spending. Business investment is expected to “remain subdued” in the context of “elevated uncertainty and low profit margins”. Extra Eurozone exports “stagnated” while intraday Eurozone trade “weakened further”. Incoming data point to “moderate but positive” growth in H2. Risks remain on the downside.

China said to have agreed plan to reverse tariffs with US

Market sentiments are once again lifted by upbeat news regarding US-China trade negotiations, as China said they’ve agreed with the US on a plan to reverse the tariffs imposed.

China Ministry of Commerce spokesman Gao Feng said, at a regular press briefing, “in the past two weeks, top negotiators had serious, constructive discussions and agreed to remove the additional tariffs in phases as progress is made on the agreement,” spokesman Gao Feng said Thursday..

“If China, U.S. reach a phase-one deal, both sides should roll back existing additional tariffs in the same proportion simultaneously based on the content of the agreement, which is an important condition for reaching the agreement.”

US initial claims dropped to 211k, below expectation of 215k

US initial jobless claims dropped -8k to 211k in the week ending November 2, below expectation of 215k. Four-week moving average of initial claims rose 0.25k to 215.25k. Continuing claims dropped -3k in the week ending October 26 to 1.689m. Four-week moving average of continuing claims was unchanged at 1.687m.

Australia trade surplus widened to AUD 7.18B, construction index improved slightly

In seasonally adjusted terms, Australia trade surplus widened to AUD 7.18B in September, up from AUD 6.62B, beat expectation of AUD 5.10B. Exports rose 3% to AUD 43.2B. Imports rose 3% to AUD 36.0B.

Also released, AiG Performance of Construction index rose to 43.9 in October, up from 42.6. The data reflected less pronounced reductions in activity, new orders and employment. However, highlighting the subdued overall state of business conditions, deliveries from suppliers declined at a steeper rate in the month.

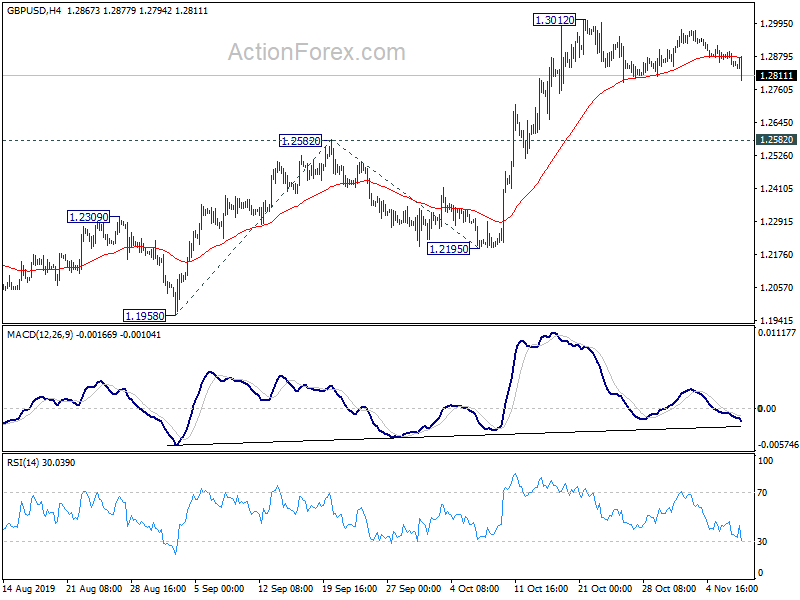

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2835; (P) 1.2866; (R1) 1.2888; More….

GBP/USD drops notably today but it’s still seen as in consolidation from 1.3012. Intraday bias remains neutral for the moment. In case of further pull back, downside should be contained above 1.2582 resistance turned support to bring rise resumption. On the upside, break of 1.3012 will resume the rise from 1.1958 to 161.8% projection of 1.1958 to 1.2582 from 1.2195 at 1.3205 next.

In the bigger picture, current development affirms the case of medium term bottoming at 1.1958, ahead of 1.1946 (2016 low). At this point, rise from 1.1958 is seen as the third leg of consolidation from 1.1946. Further rise would be seen back towards 1.4376 resistance. For now, this will remain the favored case as long as 1.2582 resistance turned support holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:30 | AUD | AiG Performance of Construction Index Oct | 43.9 | 42.6 | ||

| 00:30 | AUD | Trade Balance (AUD) Sep | 7.18B | 5.10B | 5.93B | 6.62B |

| 07:00 | EUR | Germany Industrial Production M/M Sep | -0.60% | -0.30% | 0.30% | 0.40% |

| 08:00 | CHF | Foreign Currency Reserves (CHF) Oct | 779B | 777B | ||

| 08:00 | CNY | Foreign Exchange Reserves M/M Oct | $3.105T | $3.089T | $3.092T | |

| 09:00 | EUR | ECB Economic Bulletin | ||||

| 10:00 | EUR | EU Economic Forecasts | ||||

| 12:00 | GBP | BoE Interest Rate Decision | 0.75% | 0.75% | 0.75% | |

| 12:00 | GBP | BoE Asset Purchase Facility | 435B | 435B | 435B | |

| 12:00 | GBP | MPC Official Bank Rate Votes | 0–2–7 | 0–0–9 | 0–0–9 | |

| 12:00 | GBP | MPC Asset Purchase Facility Votes | 0–0–9 | 0–0–9 | 0–0–9 | |

| 12:00 | GBP | BoE Quarterly Inflation Report | ||||

| 13:30 | USD | Initial Jobless Claims (Nov 1) | 211K | 215K | 219K | |

| 15:30 | USD | Natural Gas Storage | 46B | 89B |