Sentiments remain generally cautious in Asian session today. Major indices are mixed following slight weakness in US stocks overnight. The Pound failed to break through near term resistance against Dollar for the second time and retreated. Euro’s rebound against Dollar also lost momentum. Canadian Dollar recovered after BoC Governor Stephen Poloz said monetary policy was “about right”. But there is no clear directions in the forex markets overall. Focus will turn to PMI data from Eurozone, UK and US, as well as Canada retail sales for guidance.

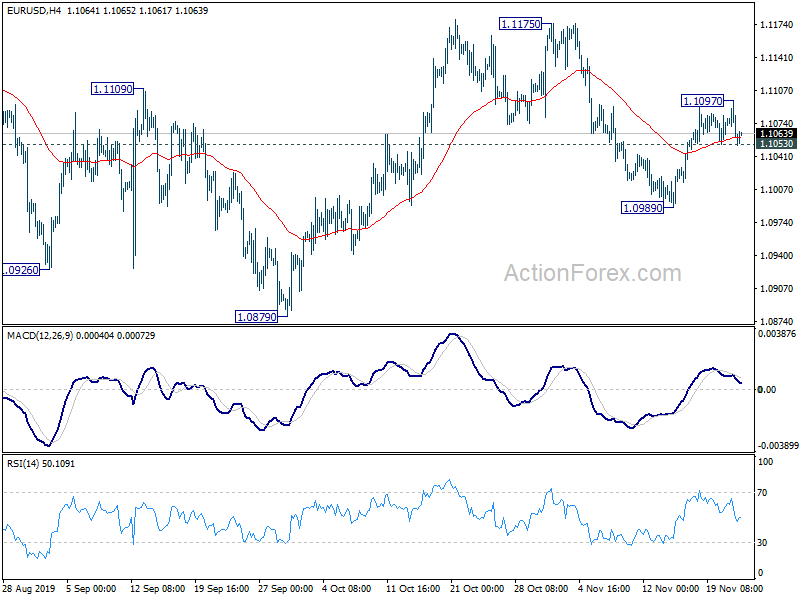

Technically, EUR/USD is now pressing 1.1053 minor support as rebound from 1.0989 lost momentum. Break of 1.1053 will suggest completion of the rebound and bring retest of 1.0989. AUD/USD is crawling back to 0.6769. Break there will downside acceleration will resume the fall from 0.6929 to 0.6670 low. USD/CAD is retreating mildly but further rise is expected with 1.3190 support intact, for 1.3347/82 resistance zone.

In Asia, Nikkei is up 0.35%. Hong Kong HSI is up 0.26%. China Shanghai SSE is down -0.59%. Singapore Strait Times is up 0.52%. Japan 10-year JGB yield rose 0.0293 to -0.081. Overnight, DOW dropped -0.20%. S&P 500 dropped -0.16%. NASDAQ dropped -0.24%. 10-year yield rose 0.034 to 1.772.

Australia PMI composite dropped to 49.5, renewed fall in private sector output

Australia CBA PMI Manufacturing dropped to 49.9 in November, down from 50.0. PMI Services dropped to 49.5, down from 50.1. PMI Composite dropped to 49.5, down form 50.0. The data signalled a renewed fall in private sector output. Declines were seen across both manufacturing and service sectors.

Commenting on the Commonwealth Bank Flash PMI data, CBA Chief Economist, Michael Blythe said: “Activity in the key manufacturing and services sectors continues to bounce around the 50 line that separates expansion from contraction. This is a particularly disappointing result when benchmarked against interest rate cuts, tax cuts, rising house prices and a still solid labour market”.

“Readings on new orders and employment offer a glimmer of positive news. But the challenges faced by Australian businesses are evident in the accelerating growth in input prices and the slowing trend in output prices. Competitive pressures and weak demand are taking a toll”.

Japan PMI composite rose to 48.6, strong possibility of Q4 GDP contraction

Japan PMI Manufacturing rose to 48.6 in November, up from 48.4, but missed expectation of 48.7. PMI Services rose to 50.4, up from 49.7. PMI Composite also improved to 48.6, up from 48.4.

Joe Hayes, Economists at IHS Markit, noted: October PMI data was difficult to interpret as a result of the temporary negative shocks by the sales tax and typhoon. However, we can deduce from the November PMI data that there is a strong possibility of Japan’s economy contracting in the fourth quarter. We have seen little rebound following these temporary factors, especially in the service sector where the impact of the tax rise and poor weather was most prominent:.

Japan CPI core edged up to 0.4%, well below BoJ’s target

Japan CPI core (all item ex-fresh food) rose to 0.4% yoy in October, up from 0.3%, matched expectations. All item CPI was unchanged at 0.2% yoy, missed expectation of 0.3% yoy. CPI core-core (all item ex-fresh food, energy), rose to 0.7%, up from 0.5%, beat expectation of 0.6% yoy.

The inflation subdued inflation reading suggests that the sales tax hike in the month had little impact on prices, and is unlikely o derail consumer spending. Yet the core inflation reading remains well below BoJ’s 2% target. The central will need to maintain ultra-loose monetary policy for a prolonged period. But even so, there is little evidence to show that inflation could sustainably hit the target with current stimulus.

Looking ahead

PMI data will be the main focuses for today as Eurozone and UK PMIs will be featured in European session. US will also release PMIs. Canada’s retail sales will also be featured.

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1042; (P) 1.1069; (R1) 1.1086; More…

EUR/USD lost upside momentum again after hitting 1.1097. Intraday bias is turned neutral first. On the downside, break of 1.1053 minor support will suggests that rebound from 1.0989 has completed. Intraday bias will be turned back to the downside for 1.0989 support. Break will resume the decline from 1.1175 for retesting 1.0879 low. On the upside, above 1.1097 will extend the rebound to retest 1.1175 resistance.

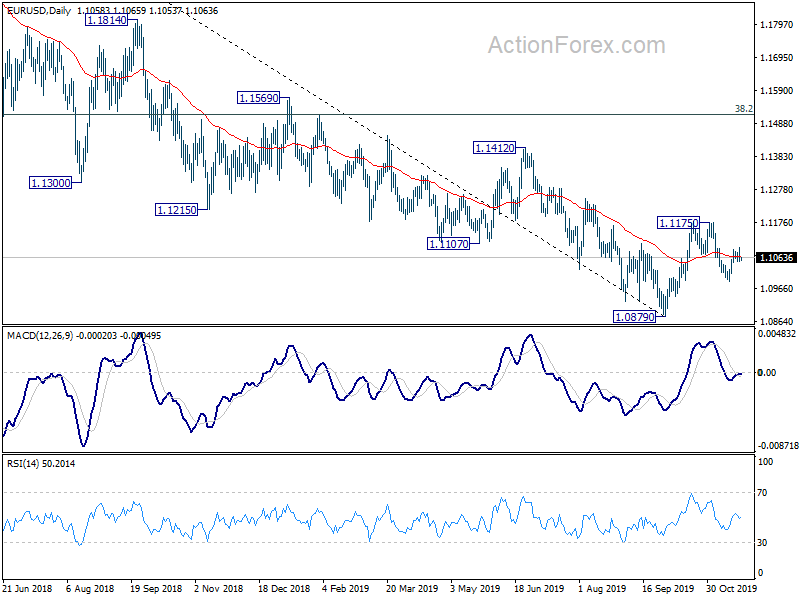

In the bigger picture, at this point, rebound from 1.0879 is seen as a corrective move first. in case of another rise, upside should be limited by 38.2% retracement of 1.2555 to 1.0879 at 1.1519. And, down trend from 1.2555 (2018 high) would resume at a later stage. However, sustained break of 1.1519 will dampen this bearish view and bring stronger rise to 61.8% retracement at 1.1915 next.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:00 | AUD | CBA Manufacturing PMI Nov P | 49.9 | 50 | ||

| 22:00 | AUD | CBA Services PMI Nov P | 49.5 | 50.1 | ||

| 23:30 | JPY | National CPI Core Y/Y Oct | 0.40% | 0.40% | 0.30% | |

| 00:30 | JPY | Jibun Bank Manufacturing PMI Nov P | 48.6 | 48.7 | 48.4 | |

| 07:00 | EUR | Germany GDP Q/Q Q3 | 0.10% | 0.10% | ||

| 08:15 | EUR | France Manufacturing PMI Nov P | 50.8 | 50.7 | ||

| 08:15 | EUR | France Services PMI Nov P | 53 | 52.9 | ||

| 08:30 | EUR | Germany Manufacturing PMI Nov P | 43 | 42.1 | ||

| 08:30 | EUR | Germany Services PMI Nov P | 52 | 51.6 | ||

| 09:00 | EUR | Eurozone Manufacturing PMI Nov P | 46.4 | 45.9 | ||

| 09:00 | EUR | Eurozone Services PMI Nov P | 52.5 | 52.2 | ||

| 09:30 | GBP | PMI Manufacturing Nov P | 48.8 | 49.6 | ||

| 09:30 | GBP | PMI Services Nov P | 50.1 | 50 | ||

| 13:30 | CAD | Retail Sales M/M Sep | 0.00% | -0.10% | ||

| 13:30 | CAD | Retail Sales ex Autos M/M Sep | 0.70% | -0.20% | ||

| 14:45 | USD | Manufacturing PMI Nov P | 51.5 | 51.3 | ||

| 14:45 | USD | Services PMI Nov P | 51.2 | 50.6 | ||

| 14:45 | USD | PMI Composite Nov P | 51.9 | 50.9 | ||

| 15:00 | USD | Michigan Consumer Sentiment Index Nov | 95.9 | 95.7 |

{kind=link}