Dollar shrugs off slightly better than expected consumer inflation data and weakens mildly in early US session. But loss is limited as focus turns to FOMC rate decision, statement and new economic projections. At this point, European majors are generally weak as markets also look forward to tomorrow’s UK elections. Latest YouGov polls suggested that a hung parliament cannot be ruled out, even though Conservative majority remains the base case. Meanwhile, Australian and New Zealand Dollar strengthen broadly, reversing some of this week’s losses. Trades might be jumping the gun in trading tariff delay. But nothing is confirmed until some named official from the US could confirm it.

Technically, AUD/USD’s strong rebound today should have invalidated the near term bearish case. And rise from 0.6754 should still be in progress. Break of 0.6862 resistance will pave the way back to 0.6929 resistance. EUR/AUD was also rejected below 1.6323 resistance and focus is back on 1.6148 support. GBP/USD, EUR/GBP and GBP/JPY are staying consolidations, while would likely extend further first.

In Europe, currently, FTSE is down -0.05%. DAX is up 0.52%. CAC is up 0.06%. German 10-year yield is down -0.019 at -0.311. Earlier in Asia, Nikkei dropped -0.08%. Hong Kong HSI rose 0.79%. China Shanghai SSE rose 0.24%. Singapore Strait Times rose 0.32%. Japan 10-year JGB yield rose 0.0181 to -0.004.

US CPI accelerated to 2.1%, core CPI unchanged at 2.3%

In November, US CPI rose 0.3% mom versus expectation of 0.2% mom. Core CPI rose 0.2% mom matched expectations. Annually, headline CPI accelerated to 2.1% yoy, up from 1.8% yoy, beat expectation of 2.0% yoy. Core CPI was unchanged at 2.3% yoy, matched expectations.

Fed to stand pat, focuses on economic projections, some previews

FOMC rate decision is the major focus today and Fed is widely expected to keep the fed funds rates unchanged at 1.50-1.75%. Fed officials have repeatedly noted that policy is in the right place for now. There won’t be any further adjustments unless there are material changes in the economic outlook. We’d expect Fed’s statement to reflect such message again.

Attentions would, therefore, be mainly on the new economic projections, in particular, federal funds rate projections. As in September’s meeting, median rate projections were at 1.9% in 2019 and 1.9% in 2020, before rising to 2.1% in 2021 and 2.4% in 2022. Current rates are already below these levels and thus, downside revisions should naturally be seen. Fed is unlikely to revise down 2020 projections to an extent that reflects another rate cut. Thus, the main market moving part would on the how fast Fed officials expect rates to climb back in 2021 and 2022.

Here are some suggested previews:

- Fed to Leave Policy Rate Unchanged in December, and Likely for 2020

- FOMC Preview: Fed On Hold For At Least A Couple Of Meetings

- Fed Meeting: No Fireworks, Focus on the ‘Dots’

- FOMC Preview: Rates On Hold

BoJ Kuroda: Global economy relatively bright next year

BoJ Governor Haruhiko Kuroda said together that the “overall global economy is expected to be relatively bright next year”. He noted that economies in US and China are firm. Global economy will also pick up. Additionally, BoJ would need to pay close attention to climate change.

Meanwhile, Kuroda also said BoJ stands ready to step up stimulus if needed. But it’s also mindful of rising costs of prolonged easing. He urged financial institutions to diversify operations, cut costs and consider consolidating businesses.

BoJ said “the domestic and external environment surrounding financial institutions is changing rapidly. The industry is entering an age of reform aimed at rebuilding its business model into a more sustainable one”.

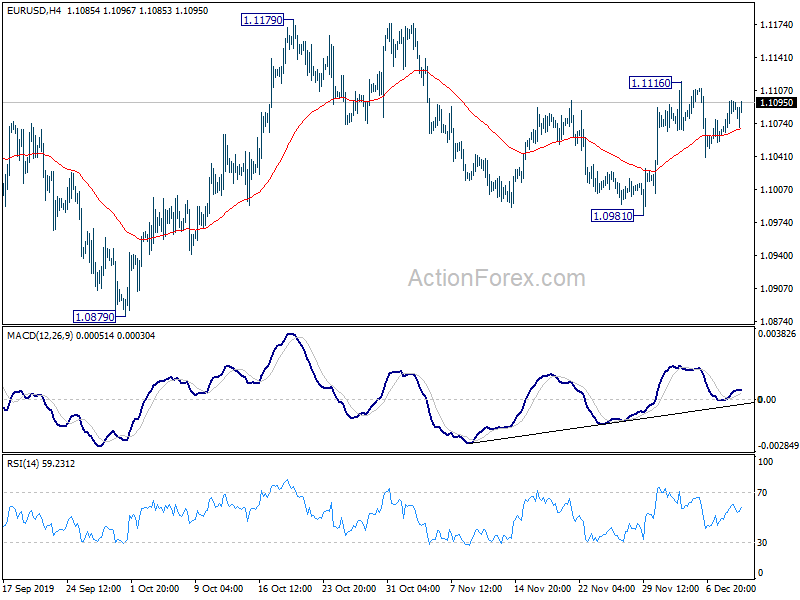

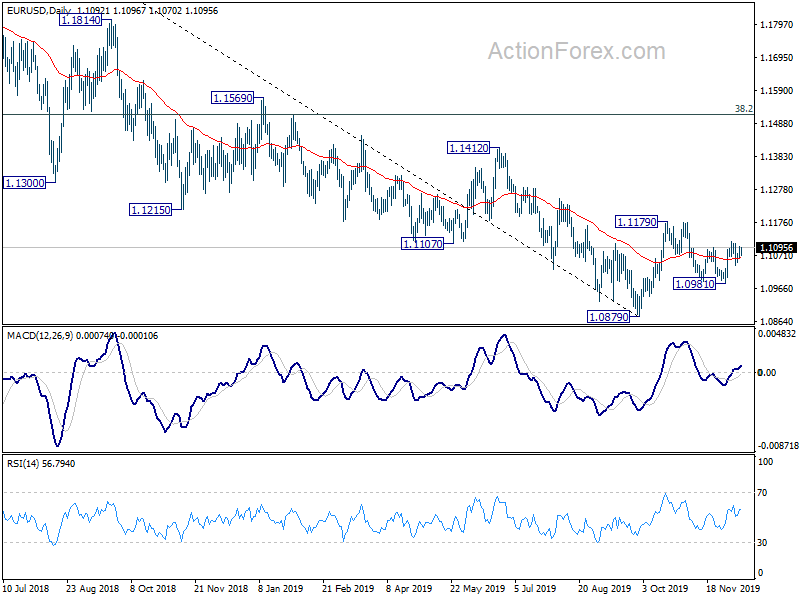

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1073; (P) 1.1086; (R1) 1.1108; More…

Intraday bias in EUR/USD stays neutral and range trading continues inside 1.0981/1116. On the upside, above 1.1116 will resume the rise from 1.0981 to 1.1179 resistance. That will also revive the case that correction from 1.1179 has completed and rise from 1.0879 is ready to resume. On the downside, break of 1.0981 will resume the decline from 1.1179 for retesting 1.0879 low instead.

In the bigger picture, rebound from 1.0879 is seen as a corrective move first. In case of another rise, upside should be limited by 38.2% retracement of 1.2555 to 1.0879 at 1.1519. And, down trend from 1.2555 (2018 high) would resume at a later stage. However, sustained break of 1.1519 will dampen this bearish view and bring stronger rise to 61.8% retracement at 1.1915 next.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | AUD | Westpac Consumer Confidence Dec | -1.90% | 4.50% | ||

| 23:50 | JPY | PPI Y/Y Nov | 0.10% | 0.00% | -0.40% | |

| 23:50 | JPY | BSI Large Manufacturing Index Q/Q Q4 | -7.8 | 0.2 | -0.2 | |

| 13:30 | USD | CPI M/M Nov | 0.30% | 0.20% | 0.40% | |

| 13:30 | USD | CPI Y/Y Nov | 2.10% | 2.00% | 1.80% | |

| 13:30 | USD | CPI Core M/M Nov | 0.20% | 0.20% | 0.20% | |

| 13:30 | USD | CPI Core Y/Y Nov | 2.30% | 2.30% | 2.30% | |

| 13:30 | CAD | Capacity Utilization Q3 | 81.70% | 82.10% | 83.30% | |

| 15:30 | USD | Crude Oil Inventories | -2.9M | -4.9M | ||

| 19:00 | USD | FOMC Rate Decision | 1.75% | 1.75% | ||

| 19:00 | USD | FOMC Economic Projections | ||||

| 19:30 | USD | FOMC Press Conference |

{kind=link}