Middle East tensions continued to drive risk aversion in the markets as another week started. Stocks in Asia are generally in red, except in being mixed in China. Gold and oil price surge sharply on safe haven flows. Movements in the currency markets are relatively limited though. Canadian Dollar is the stronger one on oil prices, followed by Swiss Franc and Yen. New Zealand and Australian Dollars are the weakest, followed by Dollar.

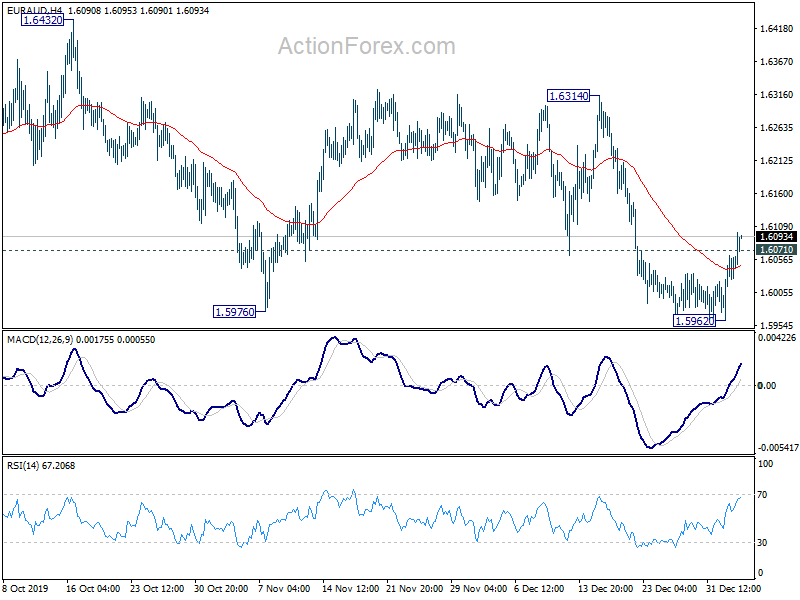

Technically, recovery in USD/CAD is so far rather and held well below 1.3102 resistance. We’d expect further decline through 1.2951 temporary low to 1.2779 projection target. AUD/USD is pressing 0.6938 support and sustained break will confirm near term reversal for 0.6754 support next. EUR/AUD’s break of 1.6071 resistance should confirm short term bottoming. Further rise is expected for 1.6314 resistance next.

In Asia, Nikkei closed down -1.91%. Hong Kong HSI is down -0.66%. China Shanghai SSE is up 0.34%. Singapore Strait Times is down -0.49%. Japan 10-year JGB yield is down -0.017 at -0.033.

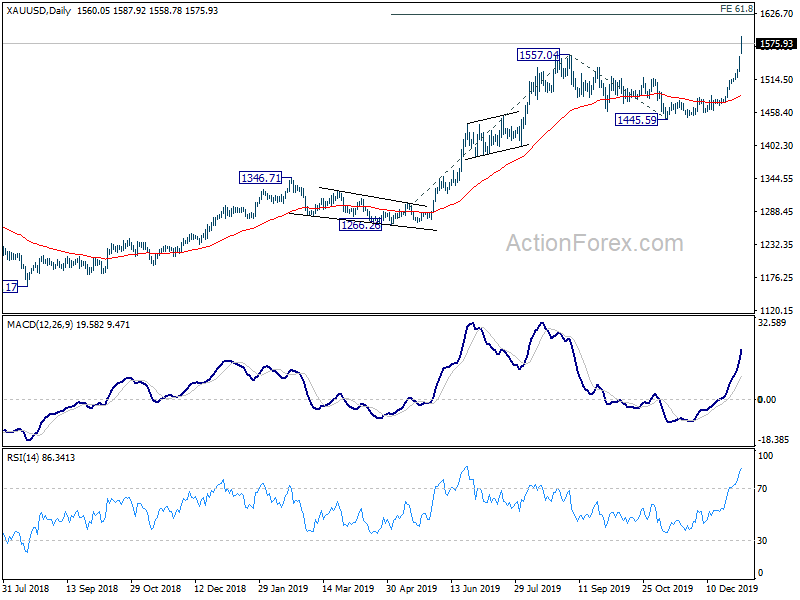

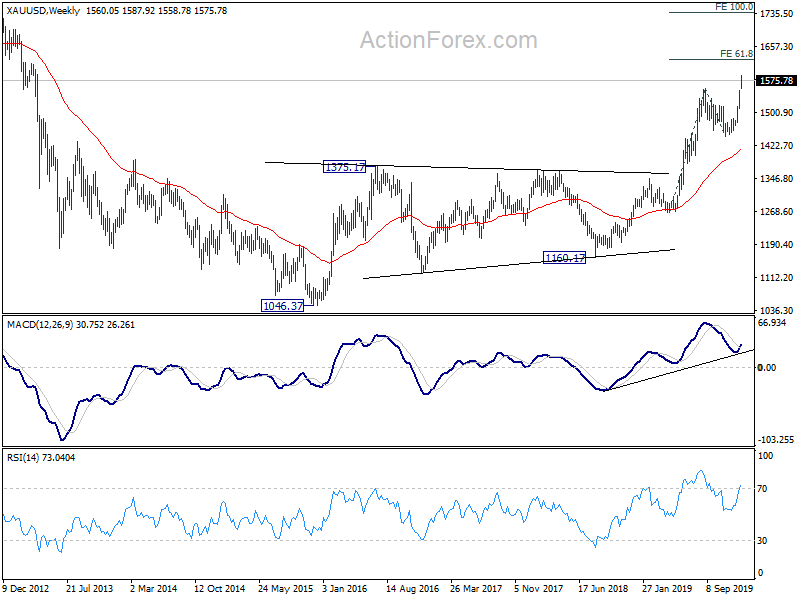

Gold gaps up as Middle East tension escalates, heading to 1625

Gold and oil prices surge as the week starts as Middle East tensions escalated further during the weekend. Iran quitted the nuclear deal and announced it’s no longer bounded by the agreement made in 2015. Iraq denounced US killing of the Iranian general in Baghdad as a violation of the nation’s sovereignty. Iraq’s parliament voted to expel US troops from the country. US President Donald Trump warned of strike to Iran “in a disproportionate manner” if the latter hits any US targets. He also threatened to sanction Iraq if US troops were forced to withdraw from the country.

Gold gaps higher today and hits as high as 1587.92. Break of 1557.04 resistance confirms resumption of up trend from 1160.17. Further rise should be seen to 61.8% projection of 1266.26 to 1557.04 from 1445.59 at 1625.29. As noted before, rise form 1445.59 could be the fifth leg of the five-wave sequence from 1160.17. We’d look for topping signal around 1625.29. However, sustained break of 1625.29 will bring upside acceleration to 100% projection at 1736.37.

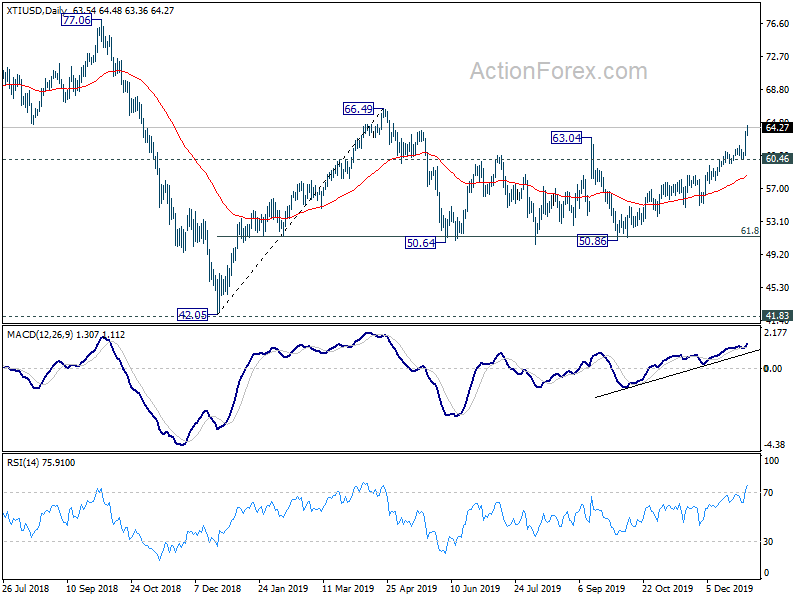

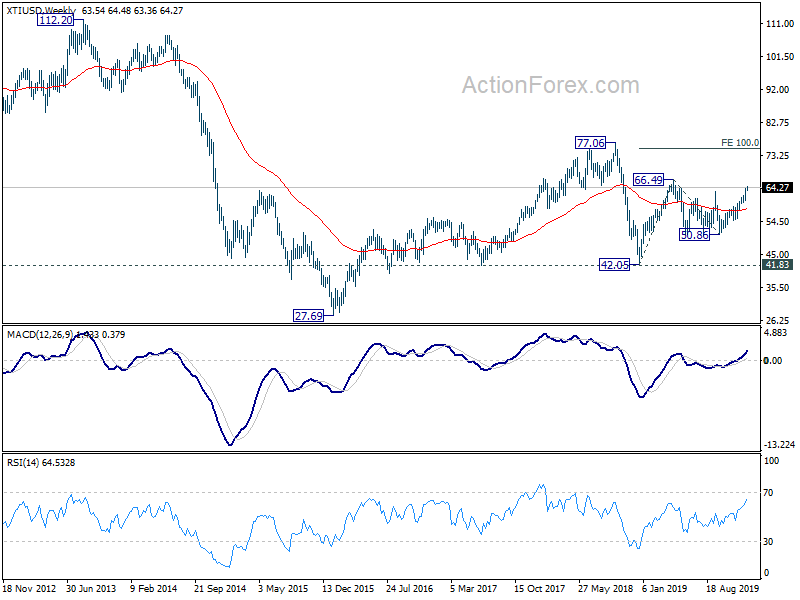

WTI oil breaks 64, but strong resistance still expected from 66.49

WTI crude oil reaches as high as 64.48 so far as recent rally resumes. At this point, we’d still be expecting strong resistance inside 63.04/66.49 to limit upside to bring reversal. We’re not expecting break out from established range between 50.64/66.49 yet. However, firm break of 66.49 will bring upside acceleration to 100% projection of 42.05 to 66.49 from 50.86 at 75.29.

Williams: Fed has to stick to 2% inflation target

New York Fed President John Williams told WSJ that it’s important for Fed to stick to its 2% inflation target. Fed has to make sure inflation expectations don’t slip too far, which will affect actual inflation in the future.

“There’s been a process of going through the stages of grief about a low neutral rate,” he said. “These factors are basically the hand we’ve been dealt for the next five to 10 years.”

He warned “if inflation continues to underrun our target levels like it has, this downward trend in inflation expectations will likely continue with inflation expectations falling well below target levels.”

Japan PMI manufacturing finalized at 48.4, negatively contribute to GDP to Q4

Japan PMI Manufacturing was finalized at 48.4 in December, down from November’s reading of 48.9. Key findings include: 1) Production Cut at strongest rate since March; 2) Weak domestic and external conditions weigh on demand; 3) Output charges reduced as firms try to stimulate sales.

Joe Hayes, Economist at IHS Markit, said: “Japan’s manufacturing sector has ended 2019 where it started, stuck in contraction with little hope of an imminent turnaround. Taking all fourth quarter survey data as one, the manufacturing economy has endured its worst performance in over three years, with momentum clearly to the downside heading into 2020… Overall, the manufacturing sector appears set to negatively contribute to GDP in the fourth quarter and, if considered in tandem with the December flash services PMI figures, the chance of an economic contraction in the fourth quarter looks strong.”

China PMI services dropped to 52.5, overall economy continued to stabilize

China Caixin PMI Services dropped to 52.5 in December, down from 53.5, missed expectation of 53.2. PMI Composite fell fro a 21-month high of 53.2 to 52.6. Markit said December saw softer, but still strong, rise in business activity. Total new work continued to rise solidly. Output charges rose in manufacturing sector, but fell at services companies.

Zhengsheng Zhong, Director of Macroeconomic Analysis at CEBM Group said: “Rates of expansion in both the services and manufacturing sectors moderated. However, China’s overall economy continued to stabilize… Looking forward, the phase one trade deal between China and the U.S. should be able to help corporate sentiment recover. China’s economy is likely to get off to a quick start in 2020, but it will still be constrained by limited demand for the rest of the year.”

Economic calendar back in full gear

The economic calendar back in full gear this week. US ISM services and non-farm payrolls will catch most attentions. But there are some important economic data elsewhere too. From Europe, Eurozone CPI, retail sales, unemployment rate and Germany industrial production will catch most attention. Canada job data will be as important as development in oil prices. Australian dollar will look into trade balance and retail sales too.

Here are some highlights for the week:

- Monday: Australia AiG manufacturing index; China Caixin PMI services; Eurozone PMI services final, PPI, Sentix investor confidence; UK PMI services; Canada RMPI and IPPI; US PMI services final.

- Tuesday: Japan monetary base; Swiss CPI; Eurozone CPI flash, retail sales; Canada trade balance, Ivey PMI; US trade balance, factory orders, ISM services.

- Wednesday: Australia AiG construction index, bulding approvals; Japan cash earnings, consumer confidence; Germany factory orders; US ADP employment.

- Thuresday: Australia trade balance; China CPI, PPI; Germany industrial production, trade balance; Swiss retail sales, foreign currency reserves; Eurozone unemployment rate; Canada housing starts, building permits; US jobless claims.

- Friday: Australia AiG services, retail sales; Japan household spending, leading indciators; Swiss unemployment rate; Canada employment; US non-farm payroll.

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6005; (P) 1.6034; (R1) 1.6092; More…

EUR/AUD’s break of 1.6071 minor resistance should confirm short term bottoming at 1.5962, ahead of 1.5894/5906 key support zone. Intraday bias is turned back to the upside. Further rise is expected to 1.6314 resistance. Decisive break there will re-affirm medium term bullishness. On the downside, break of 1.5692 will turn focus back to 1.5894/5906. Decisive break there will carry larger bearish implications.

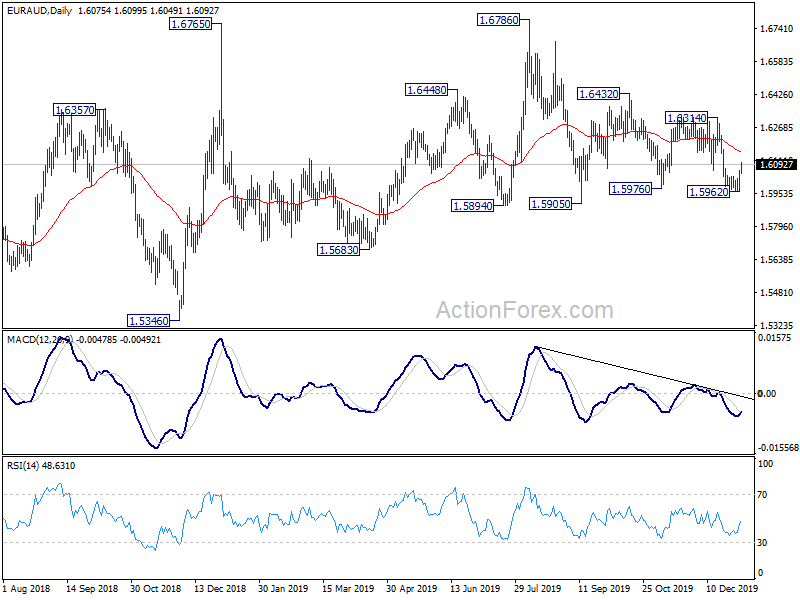

In the bigger picture, as long as 1.5894 support holds, outlook remains bullish. Firm break of 1.6786 will resume up trend from 1.1602 (2012 low). Next upside target is 61.8% retracement of 2.1127 (2008 high) to 1.1602 at 1.7488. However, sustained break of 1.5894 will have 55 week EMA (now at 1.6079) firmly taken out too. That should indicate medium term topping and target 1.5346 key support next.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:30 | AUD | AiG Performance of Mfg Index Dec | 48.3 | 48.1 | ||

| 0:30 | JPY | Jibun Bank Manufacturing PMI Dec F | 48.4 | 48.8 | ||

| 1:45 | CNY | Caixin Services PMI Dec | 52.5 | 53.2 | 53.5 | |

| 7:00 | EUR | Germany Retail Sales M/M Nov | 1.00% | -1.90% | ||

| 8:15 | EUR | Spain Services PMI Dec | 53.9 | 53.2 | ||

| 8:45 | EUR | Italy Services PMI Dec | 51.1 | 50.4 | ||

| 8:50 | EUR | France Services PMI Dec | 52.4 | 52.4 | ||

| 8:55 | EUR | Germany Services PMI Dec | 52 | 52 | ||

| 9:00 | EUR | Eurozone Services PMI Dec | 52.4 | 52.4 | ||

| 9:30 | EUR | Eurozone Sentix Investor Confidence Jan | -4.9 | 0.7 | ||

| 9:30 | GBP | Services PMI Dec | 49.2 | 49 | ||

| 10:00 | EUR | Eurozone PPI M/M Nov | 0.00% | 0.10% | ||

| 10:00 | EUR | Eurozone PPI Y/Y Nov | -1.60% | -1.90% | ||

| 13:30 | CAD | Raw Material Price Index M/M Nov | 1.50% | -1.90% | ||

| 13:30 | CAD | Industrial Product Price M/M Nov | 0.40% | 0.10% | ||

| 14:45 | USD | Services PMI Dec F | 52.2 | 52.2 |

{kind=link}