Swiss Franc jumps broadly on political news from Russia today and takes the Euro higher. Yen follow as third strongest on risk aversion as European stocks also dive on the news. Sterling is among the weakest, following weaker than expected CPI, as well as dovish comments from a BoE dove. Dollar is mixed for now, as markets await, finally, the signing of US-China trade deal phase one.

Technically, USD/CHF’s break of 0.9646 support suggests resumption of whole down trend from 1.0237. Next short to medium term target is 0.9445 projection level. EUR/GBP might has a take on 0.8595 temporary top again today. Break will extend recent rebound from 0.8276 to 0.8676 fibonacci level.

In Europe, currently, FTSE is up 0.02%. DAX is down -0.40%. CAC is down -0.42%. German 10-year yield is down -0.0458 to -0.214. Earlier in Asia, Nikkei dropped -0.45%. Hong Kong HSI dropped -0.39%. China Shanghai SSE dropped -0.54%. Singapore Strait Times dropped -0.41%. Japan 10-year yield dropped -0.0094 to 0.006, staying positive.

Russian PM resigns to give way to Putin’s constitutional changes

As reported by Russia’s Tass, Prime Minister Dmitry Medvedev submitted his resignation to President Vladimir Putin today. That’s seen as a move to make way for Putin’s changes in the constitution, to increase the powers of both the prime minster and the cabinet.

The news came after Putin’s annual state of the nation address earlier, where he proposed constitutional amendments. He said, the changes would “increase the role and significance of the country’s parliament … of parliamentary parties, and the independence and responsibility of the prime minister.”

The moves reignites speculations on Putin’s plan after his current presidential term ends in 2024. One possibility is that he would shift power to the parliament and assume an enhanced role as prime minister afterwards.

US Mnuchin: China made very strong commitments to stop forced technology transfer

US Treasury Secretary Steven Mnuchin told CNBC that the “first step” regarding trade deal with China is “really focusing on enforcement”. There will be additional tariff rollbacks in Phase 2. “This gives China a big incentive to get back to the table and agree to the additional issues that are still unresolved”.

On the details, he added, “China has agreed to put together very significant laws to change rules and regulations and have made very strong commitments to our companies that there will not be forced technology going forward.”

President Donald Trump and Chinese Vice Premier Liu He scheduled to sign the trade deal at a ceremony at the White House today, at 11:300am EST.

US Empire State manufacturing rose to 4.8

US Empire State Manufacturing general business conditions rose to 4.8 in January, up from 3.5, beat expectation of 4.1. Twenty-eight percent of respondents reported that conditions had improved over the month, while 23 percent reported that conditions had worsened. Business activity “edged somewhat higher”.

PPI rose 0.1% mom, 1.3% yoy in December, versus expectation of 0.2% mom, 1.2% yoy. PPI core rose 0.1% mom, 1.1% yoy, versus expectation of 0.2% mom, 1.4% yoy.

BoE Saunders: Possibly appropriate to cut rates further

In a speech, BoE dove Michael Saunders said the UK economy has “remained sluggish”. The “most likely outlook ” is a “further period of subdued growth” and hence, a “disinflationary backdrop of a persistent – albeit modest – output gap”. Additionally, neutral rate may have fallen further over the last year or two, both in UK and externally.

Therefore, “against this backdrop, it probably will be appropriate to maintain an expansionary monetary policy stance and possibly to cut rates further, in order to reduce risks of a sustained undershoot of the 2% inflation target.”

Also, “with limited monetary policy space, risk management considerations favour a relatively prompt and aggressive response to downside risks at present.”

UK CPI slowed to 1.3%, lowest since Dec 2016

UK CPI slowed to 1.3% yoy in December, down from 1.5% yoy, below expectation of 1.5% yoy. That’s also the lowest level since December 2016. Core CPI also slowed to 1.4% yoy, down from 1.7% yoy, missed expectation of 1.7% yoy. RPI was unchanged at 2.2% yoy, below expectation of 2.3% yoy.

Also released, PPI input rose to -0.1% yoy, up from -1.9%, versus expectation of -0.7% yoy. PPI output rose to 0.9% yoy, up from 0.5% yoy , matched expectation. PPI output core dropped to 0.9% yoy, down from 1.1% yoy, missed expectation of 1.0% yoy.

Eurozone industrial rose 0.2% mom in November

Eurozone industrial production rose 0.2% mom in November, below expectation of 0.3% mom. Production of capital goods rose by 1.2% and energy by 0.8%, while production of intermediate goods fell by 0.5%, non-durable consumer goods by 0.7% and durable consumer goods by 0.8%.

EU 28 industrial production dropped -0.1%. Among Member States for which data are available, the highest increases in industrial production were registered in Lithuania (+3.0%), Malta (+2.6%), Poland and Sweden (both +1.6%). The largest decreases were observed in Denmark (-4.7%), Ireland (-4.1%) and Greece (-3.7%).

Trade surplus narrowed to EUR 19.2B in November, missed expectation of EUR 22.3B.

BoJ downgrades economic assessments of three regions

In the latest Regional Economic Report, BoJ downgraded the assessments of three regions, Hokuriku, Tokai and Chugoku. Nevertheless, all nine regions reported that “their economy had been either expanding or recovering.”

“The background to this was that domestic demand, in terms of such items as business fixed investment and private consumption, had continued on an uptrend, with a virtuous cycle from income to spending operating in both the corporate and household sectors, although exports, production, and business sentiment had shown some weakness, mainly affected by the slowdown in overseas economies and natural disasters.”

Earlier today, BoJ Governor Haruhiko Kuroda reiterated that “we will adjust policy as necessary to maintain momentum toward our price stability target while examining risks… We will not hesitate to take additional easing steps if risks heighten to an extent that the momentum toward the price target is undermined.”

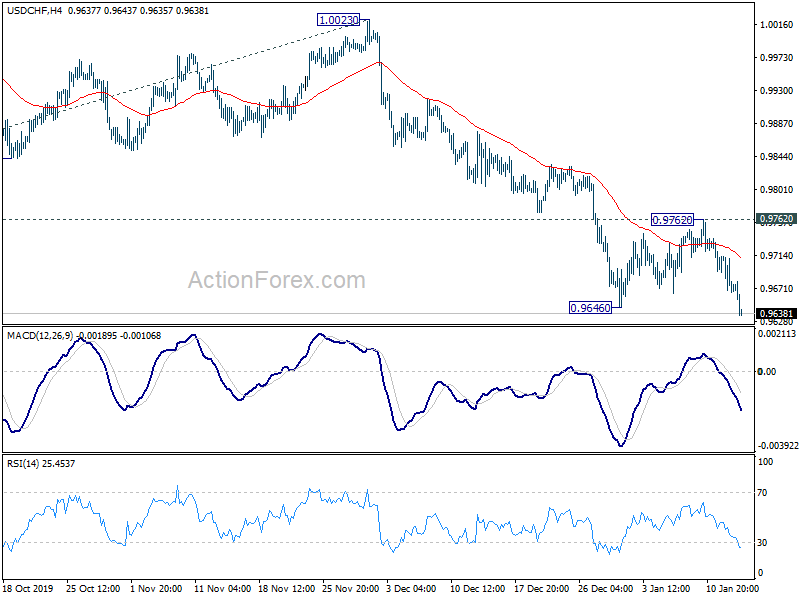

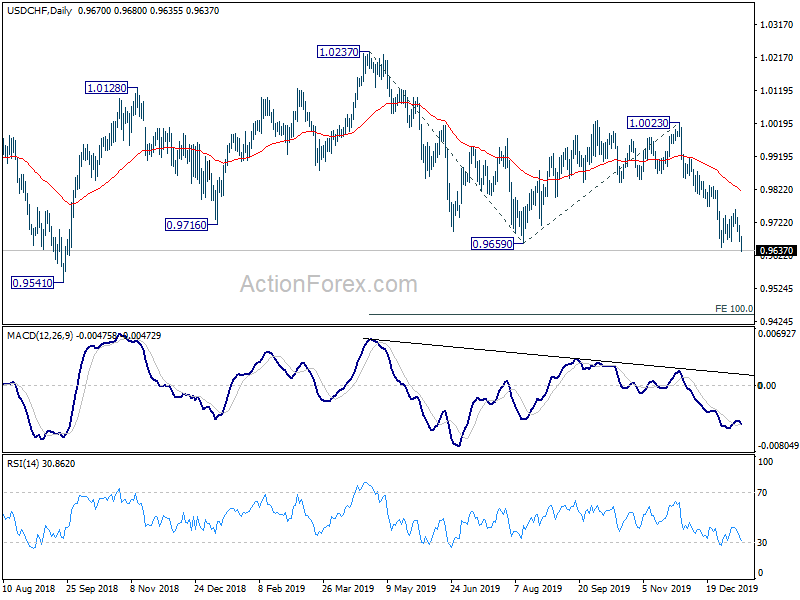

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9656; (P) 0.9685; (R1) 0.9703; More…

USD/CHF drops to as low as 0.9635 so far today. Break of 0.9646 support indicates resumption of larger down trend from 1.0237. Intraday bias is back on the downside for 100% projection of 1.0237 to 0.9659 from 1.0023 at 0.9445. On the upside, break of 0.9762 resistance is needed to indicate short term bottoming. Otherwise, outlook will remain bearish in case of recovery.

In the bigger picture, medium term outlook remains neutral as USD/CHF is staying sideway trading started from 1.0342 (2016 high). Fall from 1.0237 is a leg inside the pattern and could target 0.9186 (2018 low). In case of another rise, break of 1.0237 is needed to indicate up trend resumption. Otherwise, more sideway trading would be seen with risk of another fall.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Money Supply M2+CD Y/Y Dec | 2.70% | 2.70% | 2.80% | 2.70% |

| 06:00 | JPY | Machine Tool Orders Y/Y Dec P | -33.60% | -37.90% | ||

| 09:30 | GBP | DCLG House Price Index Y/Y Nov | 2.20% | 1.20% | 0.70% | 1.30% |

| 09:30 | GBP | CPI M/M Dec | 0.00% | 0.20% | 0.20% | |

| 09:30 | GBP | CPI Y/Y Dec | 1.30% | 1.50% | 1.50% | |

| 09:30 | GBP | Core CPI Y/Y Dec | 1.40% | 1.70% | 1.70% | |

| 09:30 | GBP | RPI M/M Dec | 0.30% | 0.30% | 0.20% | |

| 09:30 | GBP | RPI Y/Y Dec | 2.20% | 2.30% | 2.20% | |

| 09:30 | GBP | PPI – Input M/M Dec | 0.10% | 0.30% | -0.30% | 0.50% |

| 09:30 | GBP | PPI – Input Y/Y Dec | -0.10% | -0.70% | -2.70% | -1.90% |

| 09:30 | GBP | PPI – Output M/M Dec | 0.00% | 0.00% | -0.20% | |

| 09:30 | GBP | PPI – Output Y/Y Dec | 0.90% | 0.90% | 0.50% | |

| 09:30 | GBP | PPI – Output Core M/M Dec | -0.10% | 0.00% | -0.10% | |

| 09:30 | GBP | PPI – Output Core Y/Y Dec | 0.90% | 1.00% | 1.10% | |

| 10:00 | EUR | Eurozone Trade Balance (EUR) Nov | 19.2B | 22.3B | 24.5B | 24.0B |

| 10:00 | EUR | Industrial Production M/M Nov | 0.20% | 0.30% | -0.50% | -0.90% |

| 13:30 | USD | Empire State Manufacturing Index Jan | 4.8 | 4.1 | 3.5 | |

| 13:30 | USD | PPI M/M Dec | 0.10% | 0.20% | 0.00% | |

| 13:30 | USD | PPI Y/Y Dec | 1.30% | 1.20% | 1.10% | |

| 13:30 | USD | PPI Core M/M Dec | 0.10% | 0.20% | -0.20% | |

| 13:30 | USD | PPI Core Y/Y Dec | 1.10% | 1.40% | 1.30% | |

| 15:30 | USD | Crude Oil Inventories | 0.4M | 1.2M | ||

| 19:00 | USD | Fed’s Beige Book |

{kind=link}