Dollar weakens mildly again as risk appetite is lifted by the three-stage plan to exit lockdown in the US. While Q1 GDP contraction in China was deeper than expected, March data also provided some optimism of return to normal. As Asian markets rebound, Yen and Swiss Franc are following Dollar as the next weakest for today. Commodity currencies are generally higher.

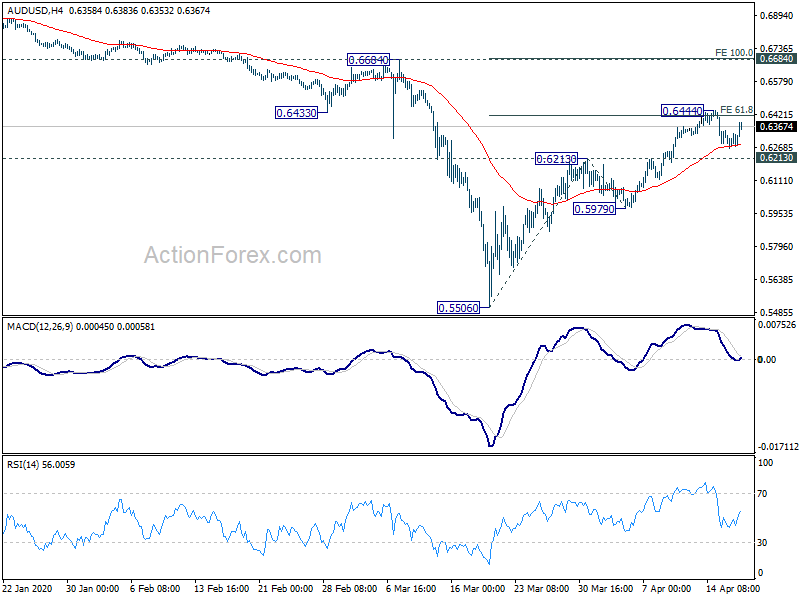

Technically, the recovery in the greenback is somewhat disappointing. USD/JPY is back into focus as rejection by 4 hour 55 EMA might drag the pair down to 106.91 support again. Break will resume whole fall from 111.71 and could prompt selling in Dollar elsewhere. Meanwhile, AUD/USD already drew some support from 4 hour 55 EMA to recovery. Focus is back on 0.6444 temporary top. Break will resume whole rebound from 0.5506.

In Asia, currently, Nikkei is up 2.62%. Hong Kong HSI is up 2.31%. China Shanghai SSE is up 0.89%. Singapore Strait Times is up 1.31%. Japan 10-year JGB yield is up 0.0013 at 0.008. Overnight, DOW rose 0.14%. S&P 500 rose 0.58%. NASDAQ rose 1.66%. 10-year yield dropped -0.029 to 0.609.

China GDP contracted -6.8% in Q1, but March data show improvements

China’s GDP contracted -6.8% quarter over year in Q1. That’s the worst performance since at least 1992 as the country was brought to paralysis coronavirus outbreak. The contraction was also slightly larger than expectation of -6.0%.

In March, retail sales dropped -15.8% yoy, after tumbling for -20.5% yoy in the first two months, versus expectation of -8.8% yoy. Industrial production dropped -1.1% yoy, much less severe than expectation of -5.6% yoy. Fixed asset investments contracted -16.1% ytd yoy in January-March period, below expectation of 15.1% yoy, improved from January-February’s -24.5% ytd yoy.

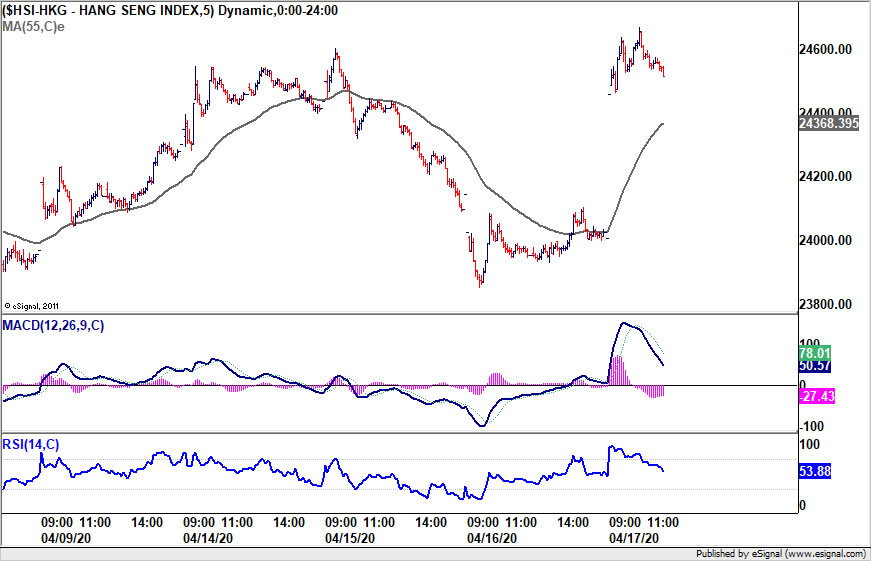

There was no negative reactions from the markets, despite the poor GDP data. Some traders are indeed seeing the improvement in March data, in particular production, as sign of silver linings. Hong Kong HSI gapped up earlier today and remains firm, up more than 2% at the time of writing.

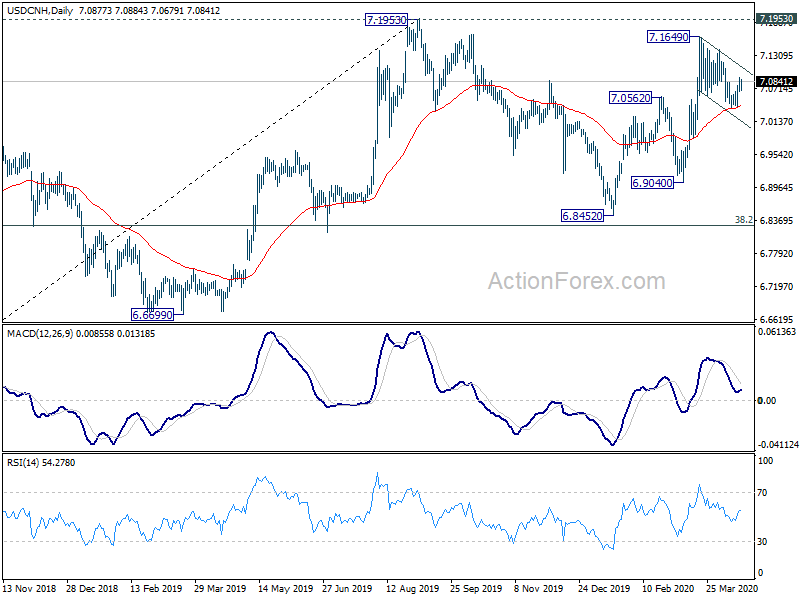

USD/CNH is also staying in tight range today. The pair recovered after drawing support from 55 day EMA. Rise from 6.8452 is still mildly in favor to extend to retest 7.1953 high.

Fed Williams: Full scale of coronavirus economic consequences still unknown

New York Fed President John Williams said yesterday, “the coronavirus pandemic has created circumstances we have never experienced before in our lifetimes. The reality is that the full scale of the economic consequences is still unknown.”

The economy is “going to be underperforming for some time”. “There’s a lot of uncertainty about how long it will take,” Williams added, and Fed will “use all of our tools as appropriate” to support the economy.

Fed Harker: The worst thing is to rush reopening

Philadelphia Fed President Patrick Harker said monetary policy is going to “stay low until we really see the economy starting to recover back to our dual mandate”. Exactly how long that is a “function of how quickly medical science and industry can put in place the tools, the testing regimes, the vaccines etc. to keep the American public safe.”

But he warned, “the worst thing we can do in my mind is rush this” and have a “significant rebound… which would just set us back”.

Fed Kashkari: Staged approach for reopening makes sense

Minneapolis Fed President Neel Kashkari said the plan to reopen the economy in a staged approach “makes sense”. “When I looked at the president’s plan it seems consistent with the advice and the feedback that we’ve heard from health experts, that there is a way to slowly reopen the economy,” he said.

“Obviously we want to try to avoid the virus flaring back up again and giving back the gains that we’ve had, and I think a staged approach, looking over the horizon, makes sense.”

Looking ahead

Eurozone March CPI final and Italy trade balance will be featured in European session. Canada will release foreign securities purchases later in the day.

AUD/USD Daily Report

Daily Pivots: (S1) 0.6279; (P) 0.6306; (R1) 0.6348; More…

AUD/USD recovered after hitting 4 hour 55 EMA but stays below 0.6444 temporary top. Intraday bias remains neutral first. on the upside, break of 0.6444 will extend the rebound from 0.5506 to 100% projection of 0.5506 to 0.6213 from 0.5979 at 0.6686, which is close to 0.6684 key resistance. On the downside, break of 0.6213 resistance turned support will argue that such rebound has completed. Intraday bias will be turned back to the downside for 0.5979 support for confirmation.

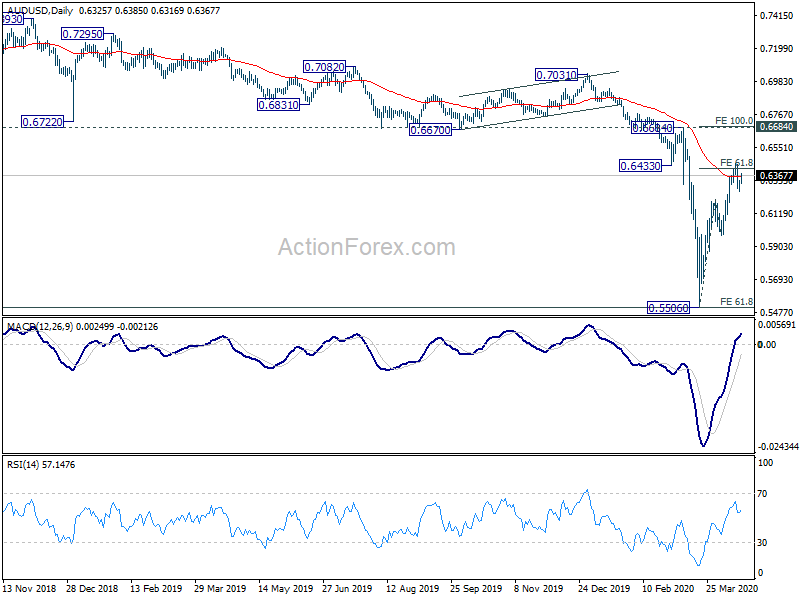

In the bigger picture, there is no clear sign of trend reversal yet. The larger down trend from 1.1079 (2011 high) is still in favor to extend. 61.8% projection of 1.1079 to 0.6826 from 0.8135 at 0.5507 is already met. Sustained break there will pave the way to 0.4773 (2001 low). On the upside, break of 0.6670 support turned resistance is needed to indicate medium term bottoming. Otherwise, outlook will remain bearish even in case of strong rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 2:00 | CNY | GDP Q/Y Q1 | -6.80% | -6.00% | 6.00% | |

| 2:00 | CNY | Retail Sales Y/Y Mar | -15.80% | -8.80% | -20.50% | |

| 2:00 | CNY | Industrial Production Y/Y Mar | -1.10% | -5.60% | -13.50% | |

| 2:00 | CNY | Fixed Asset Investment YTD Y/Y Mar | -16.10% | -15.10% | -24.50% | |

| 4:30 | JPY | Tertiary Industry Index M/M Feb | -0.50% | -0.20% | 0.80% | |

| 4:30 | JPY | Industrial Production M/M Feb F | -0.30% | 0.40% | 0.40% | |

| 8:00 | EUR | Italy Trade Balance (EUR) Feb | 0.54B | |||

| 9:00 | EUR | Eurozone CPI Y/Y Mar F | 0.70% | 0.70% | ||

| 9:00 | EUR | Eurozone CPI – Core Y/Y Mar F | 1.00% | 1.00% | ||

| 12:30 | CAD | Foreign Securities Purchases (CAD) Feb | 17.01B |

{kind=link}