Australian Dollar strengthen mildly today following recovery in the stock markets. It remains steady after RBA left monetary policy unchanged as widely expected. Rally in oil price, with WTI crude oil up 6.5% at 21.7, is helping sentiments in general, as well as the Canadian Dollar. On the other hand, Dollar turns soft, followed by Swiss France, Euro and Yen.

Technically, there is no confirmation of return of risk-off yet. DOW is holding comfortably above 22941.88 support despite yesterday’s initial dip. Hong Kong HSI is also holding above corresponding support at 23483.31. In the currency markets, the selloff in commodity currencies could have passed an initial peak, with AUD/USD recovery and USD/CAD retreating. Consolidative trading might continue in general. Though, a focus is back on 106.35 temporary low in USD/JPY and break will resume whole fall from 111.71.

In Asia, currently, Hong Kong HSI is up 0.54%. Singapore Strait Times is up 0.78%. Japan and China remain on holiday. Overnight, DOW rose 0.11%. S&P 500 rose 0.42%. NASDAQ rose 1.23%. 10-year yield dropped -0.005 to 0.637.

RBA stands pat, scaled back bond purchases as markets improved

RBA left monetary policy unchanged today as widely expected. The cash rate is held at 0.25%. The bank “will not increase the cash rate target until progress is being made towards” the dual mandate of full employment and inflation target.

Target for 3-year government bond yield is also kept at 0.25%. Global financial markets are working “more effectively” and Australian government bond markets has “improved”. Hence, RBA scaled back the size and frequency of purchases, which “to date have totalled around $50 billion”. Though, the 3-year yield target will “remain in place” and the bank is “prepared to scale up” the purchases if necessary.

In the baseline scenario for the economy, RBA said output would fall by around -10% over H1 2020 and around -6% over the year. There would be a bounce-back of 6% in 2021. Unemployment rate would peak at around 10% over the coming months and stay above 7% by the end of 2020. Inflation will remain below 2% target over the next few years in the various scenarios considered. In the baseline scenario, inflation will be at 1-1.5% in 2021 and gradually picks up further from there.

Australia AiG construction dropped to 21.6, record low

Australia AiG Performance on Construction Index dropped to 21.6 in April, down from 37.9. That was the lowest result on record and the -16.3 decline was the largest record single-month fall too.

AiG said, “activity, new orders, employment and average wages all fell to their lowest levels on record… Capacity utilised across the construction industry fell to a 12-year low. Supplier deliveries fell to their lowest since 2012.”

Also, “activity and new orders indexes for all four construction sectors included in the Australian PCI fell to record lows in April. Apartment building was the weakest sector, with its activity index falling to just 22.1 points (trend).

Also released, New Zealand building permits dropped -21.3% mom in March. ANZ commodity price dropped -1.1% in April.

US Treasury to raise USD 3T debts in Q2 to fund coronavirus measures

US Treasury announced to raise near USD 3 trillion in Q2 with privately held net marketable debt to fund the measures to counter the coronavirus economic impact. The Q2 sum alone is more than five times the amount raised during the 2008 financial crisis, and more than double the borrowed in 2019.

The Treasury said in a statement: “The increase in privately-held net marketable borrowing is primarily driven by the impact of the COVID-19 outbreak, including expenditures from new legislation to assist individuals and businesses, changes to tax receipts including the deferral of individual and business taxes from April – June until July, and an increase in the assumed end-of-June Treasury cash balance.”

Additionally, the Treasury expects to borrow USD 677 billion in privately-held net marketable debt, assuming an end-of-September cash balance of USD 800 billion.

Looking ahead

Swiss will release CPI in European session. UK will release PMI services final. Eurozone will release PPI. Later in the day, US ISM non-manufacturing will be the main focus and trade balance will be featured. Canada will also release trade balance.

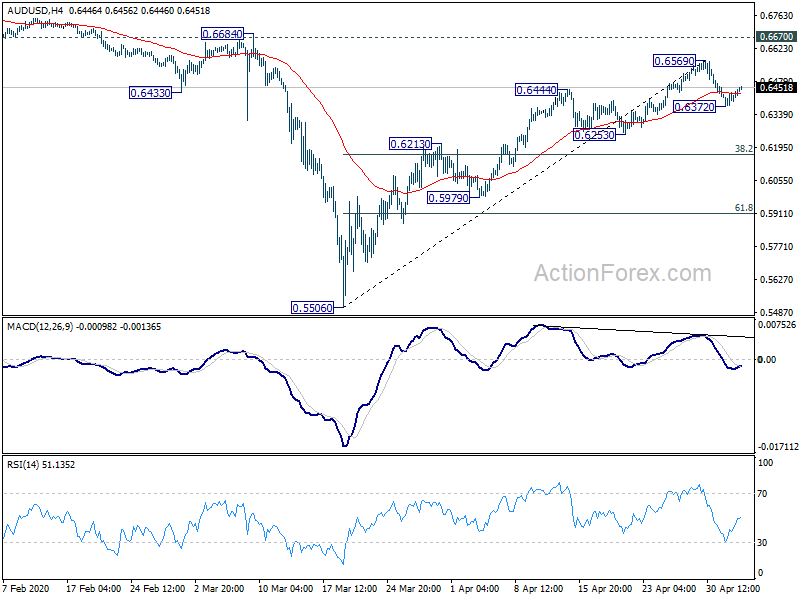

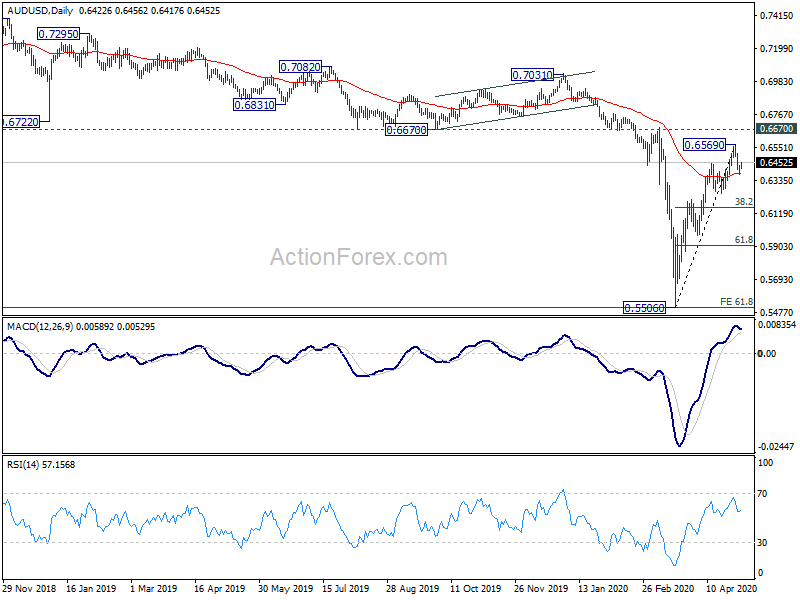

AUD/USD Daily Report

Daily Pivots: (S1) 0.6387; (P) 0.6411; (R1) 0.6449; More…

AUD/USD recovered after hitting 0.6372 and intraday bias is turned neutral first. Fall fro 0.6569 short term top is still in favor to continue and below 0.6372 will target 0.6253 support first. Break there should indicate completion of whole rise from 0.5506 and target 38.2% retracement of 0.5506 to 0.6569 at 0.6163. On the upside, break of 0.6569 will extend the rebound to 0.6670 key resistance instead.

In the bigger picture, there is no clear sign of trend reversal yet. The larger down trend from 1.1079 (2011 high) is still in favor to extend. 61.8% projection of 1.1079 to 0.6826 from 0.8135 at 0.5507 is already met. Sustained break there will pave the way to 0.4773 (2001 low). On the upside, however, sustained break of 0.6607 will suggest medium term bottoming and turn focus to 0.7031 resistance next.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:30 | AUD | AiG Performance of Construction Index Apr | 21.6 | 37.9 | ||

| 22:45 | NZD | Building Permits M/M Mar | -21.30% | 4.70% | 5.70% | |

| 1:00 | NZD | ANZ Commodity Price Apr | -1.10% | -2.10% | -2.00% | |

| 4:30 | AUD | RBA Interest Rate Decision | 0.25% | 0.25% | 0.25% | |

| 5:45 | CHF | SECO Consumer Climate Q2 | -40 | -9 | ||

| 6:30 | CHF | CPI M/M Apr | -0.10% | 0.10% | ||

| 6:30 | CHF | CPI Y/Y Apr | -0.50% | -0.50% | ||

| 8:30 | GBP | Services PMI Apr F | 12.3 | 12.3 | ||

| 9:00 | EUR | Eurozone PPI M/M Mar | -1.20% | -0.60% | ||

| 9:00 | EUR | Eurozone PPI Y/Y Mar | -2.40% | -1.30% | ||

| 12:30 | CAD | Trade Balance (USD) Mar | -2.2B | -1.0B | ||

| 12:30 | USD | Trade Balance (USD) Mar | -41.0B | -39.9B | ||

| 13:45 | USD | Services PMI Apr | 27 | 27 | ||

| 14:00 | USD | ISM Non-Manufacturing PMI May | 37.5 | 52.5 |

{kind=link}