Economic data from the US shows the sharpest labor downturn in history due to coronavirus pandemic. Yet, the financial markets have little reactions to the terrible data. US futures are pointing to higher open while European indices are in black. Investors are somewhat relieved by a formal statement by US Trade Representative regarding the “good progress” made in US-China trade deal implementations.

In the currency markets, Yen is currently the weakest one for today, followed by Dollar and then Euro. Commodity currencies are the strongest. As for the week, Euro, Swiss Franc and Sterling are the worst performing ones. Commodity currencies are the best. There might not be any special technical breakthroughs before weekly close.

In Europe, currently, FTSE is up 1.40%. DAX is up 1.26%. CAC is up 1.15%. German 10-year yield is up 0.0133 at -0.532. Earlier in Asia, Nikkei rose 2.56%. Hong Kong HSI rose 1.04%. China Shanghai SSE rose 0.83%. Singapore Strait Times rose 0.01%. Japan 10-year JGB yield dropped -0.0023 to -0.002.

US non-farm payroll dropped -20.5m, unemployment rate jumped to 14.7%

US non-farm payroll employment dropped by -20.5m in April. The over-the-month decline is that largest on record since 1939. Employment dropped to the lowest level since February 2011. Unemployment rate surged to 14.7%. This is the highest rate and largest over-the month increase in history of the series started back in January 1948. Labor force participation rate also dropped by -2.5% to 60.2%, lowest since January 1973.

Canada employment dropped -1993.7k in April, with -1472k loss in full time jobs and -552k loss in part time jobs. Unemployment rate surged to 13.0%, second only to 13.1% observed back in December 1982.

German DIHK: Still a long way to go before economy recovers

According to a flash survey of the German Chamber of Commerce and Industry DIHK, 60% of companies continue to suffer from lower demand during coronavirus crisis. 43% are experience cancelled orders. Investments are also cut back by more than a third.

80% expect a decline in sales for the whole year. One in four even fear a decline of more than 50% in sales. Over a third of companies expect a return to previous business situation in 2021 at the earliest.

“This shows the enormous challenges we are now facing,” said DIHK President Eric Schweitzer. “There is still a long way to go before our economy recovers.”

Also from Germany, trade surplus narrowed to EUR 12.8B in March, down from EUR 21.4B, missed expectation of EUR 20.1B.

RBA projects -6% GDP contraction in 2020, unemployment rate to peak at 10% in June

In the statement of monetary policy, “the Board will not increase the cash rate target until progress is being made towards full employment and it is confident that inflation will be sustainably within the 2–3 per cent target band”. Additionally, “the Board is committed to do what it can to support jobs, incomes and businesses during this difficult period and to make sure that Australia is well placed for the expected recovery.”

In the latest projections, GDP could contract by as much as -6.00% in the year ended December 2020, then recovered by 6.00% in the year-ended December 2021. Unemployment rate would surge to 10% in June 2020, then gradually drop back to 6.50% in two year’s time, without reaching the pre-crisis level of 5.20%.

Path of headline inflation projected is rather rocky. CPI would tumble to -1.00% in June 2020, then surge to 2.75% by June 2021, then drop back to 1.25-1.50% before June 2022. Trimmed mean inflation would remain steady, though, at between 1.25-1.50% throughout projection horizon, without hitting the 2% target.

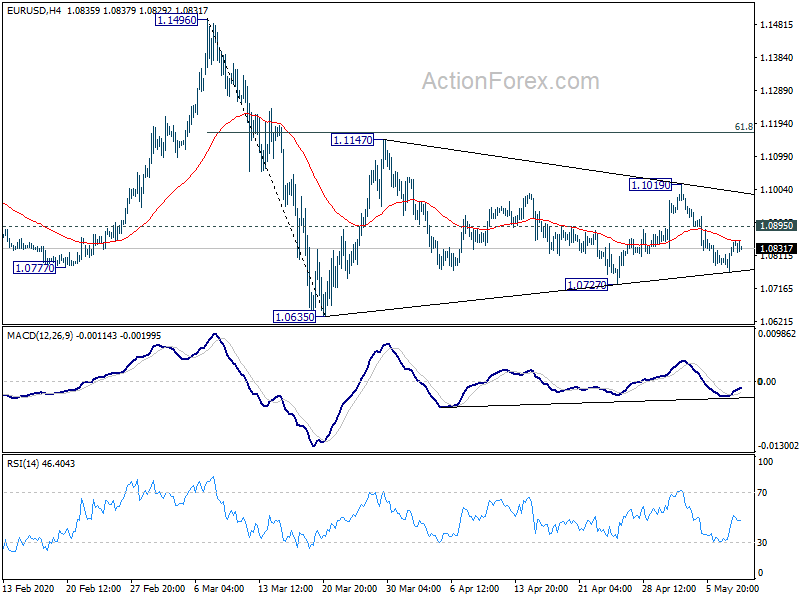

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0789; (P) 1.0812; (R1) 1.0856; More…

Intraday bias in EUR/USD remains neutral at this point. Overall, consolidation from 1.0635 is still extending. Above 1.0899 minor resistance will bring another rise to 1.1019 resistance and above. But upside should be by 61.8% retracement of 1.1496 to 1.0635 at 1.1167. On the downside, break of 1.0727 will bring retest of 1.0635 low next.

In the bigger picture, as long as 1.1496 resistance holds, whole down trend from 1.2555 (2018 high) should still be in progress. Next target is 1.0339 (2017 low). However, sustained break of 1.1496 will argue that such down trend has completed. Rise from 1.0635 could then be seen as the third leg of the pattern from 1.0339. In this case, outlook will be turned bullish for retesting 1.2555.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | Labor Cash Earnings Y/Y Mar | 0.10% | 0.10% | 0.70% | |

| 23:30 | JPY | Overall Household Spending Y/Y Mar | -6.00% | -6.70% | -0.30% | |

| 01:30 | AUD | RBA Monetary Policy Statement | ||||

| 06:00 | EUR | Germany Trade Balance (EUR) Mar | 12.8B | 20.1B | 21.6B | 21.4B |

| 12:30 | CAD | Building Permits M/M Mar | -13.20% | -20.10% | -7.30% | -8.40% |

| 12:30 | CAD | Net Change in Employment Apr | -1993.8K | -5000.0K | -1010.7K | |

| 12:30 | CAD | Unemployment Rate Apr | 13.00% | 7.20% | 7.80% | |

| 12:30 | USD | Nonfarm Payrolls Apr | -20500K | -20000K | -701K | -870K |

| 12:30 | USD | Unemployment Rate Apr | 14.70% | 14.00% | 4.40% | |

| 12:30 | USD | Average Hourly Earnings M/M Apr | 4.70% | 0.20% | 0.40% | 0.50% |

| 14:00 | USD | Wholesale Inventories Mar | -1.00% | -1.00% |

{kind=link}