The financial markets are generally treading water in Asian session today, with very limited movements. Yen, Swiss Franc and Dollar are the strongest ones for the weak so far. But there is not much committed buying seen yet. On the other hand, Sterling is the worst performing one for the week at this point, with clearer follow through selling. Commodity currencies are also soft, awaiting range breakout in stocks.

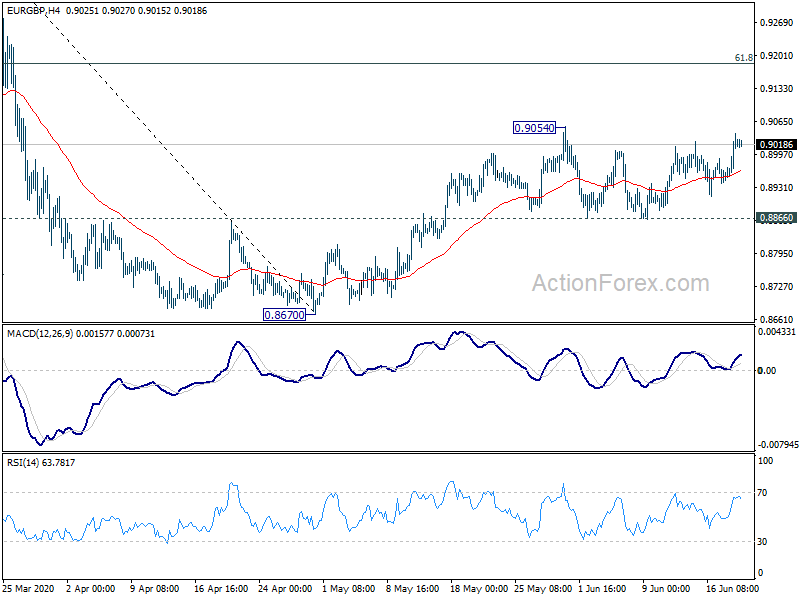

Technically, GBP/USD, GBP/JPY and GBP/CHF has also resumed recent decline. But EUR/GBP is still bounded in range of 0.8866/99054. Break of 0.9054 resistance EUR/GBP is preferred to confirm underlying weakness in the Pound. Yet, Euro’s own softness might cap EUR/GBP’s upside. Both EUR/USD and EUR/JPY have resumed recent decline. A break of 1.0650 temporary low in EUR/CHF could drag Euro down elsewhere, and could kick EUR/GBP back to the lower side of the range.

In Asia, Nikkei is currently up 0.14%. Hong Kong HSI is down -0.11%. China Shanghai SSE is up 0.39%. Singapore is down -0.81%. Japan 10-year JGB yield is up 0.0012 at 0.017. Overnight, DOW dropped -0.15%. S&P 500 rose 0.06%. NASDAQ rose 0.33%. 10-year yield dropped -0.039 to 0.694.

Japan: Economy still in extremely severe situation but had almost stopped worsening

In the last monthly report of Japan’s Cabinet Office, it’s noted that the economy remained in an “extremely severe situation” but it had “almost stopped worsening”. Private consumption is picking up. However, business investment is in a “weak tone”. Exports are “decreasing rapidly”. Industrial production is “decreasing”. Corporate profits are “decreasing rapidly”. Employment situation is “showing weakness”. Consumer prices are “flat”.

“Concerning short-term prospects, the economy is expected to move toward picking up from an extremely severe situation, supported by the effects of the policies while the socio-economic activities will be resumed gradually with taking measures to prevent the spread of infectious diseases. However, attention should be given to the trend of domestic and overseas infections, and the effects of fluctuations in the financial and capital markets.”

Japan CPI core dropped -0.2% yoy, staying in deflation for second month

Japan national CPI core (all items less fresh food) was unchanged at -0.2% yoy in May, worse than expectation of an improvement to -0.1% yoy. That’s also the second straight month of negative reading. Nevertheless, CPI core-core (all times less fresh food, energy) rose back to 0.4%, up from 0.2% yoy, which might be a sign of relief. Headline CPI (all items) was unchanged at 0.1% yoy.

In the minutes of April 27 BoJ meeting, one membered warned that “the economy might fall into deflation”, “fiscal and monetary authorities could further cooperate with each other”. Another member said BoJ should “consider what was necessary to avoid deflation”. A member said it was appropriate to “revise the forward guidance” with a view to “not allowing deflation to take hold”.

Australia retail sales rose record 16.3% in May, insufficient to recover April’s record decline

Preliminary data showed that Australia retail sales rose 16.3% mom in May. that’s the largest rise on 38 years of record. But that wasn’t enough to recover the record contraction of -17.7% mom in April.

ABS said, “there were large rises for clothing, footwear and personal accessory retailing and cafes, restaurants and takeaway food services, as restrictions on trade were lifted during May. Despite the rises, both these industries remain well down on the levels of May 2019.”

UK consumer confidence improved, could be that infamous dead cat bounce

UK Gfk consumer confidence rose 6 pts to -30 in June, hitting the highest level since March. That’s also the biggest improvement in nearly four years. Expectations on general economic situation over the next 12 months improved by 9 pts to -48, but stayed deeply negative.

“We have seen queues as some shoppers return to battered high streets,” said Joe Staton, GfK client strategy director. But “with the labor market set for more job losses, we have to question whether we are seeing early signs of economic recovery or that infamous ‘dead cat bounce.'”

Fed Bullard: Definitely don’t think we’re out of the woods

St. Louis Fed President James Bullard said yesterday that the he “definitely don’t think we’re out of the woods”, from the coronavirus crisis. The US is still at a high, high risk level here,” he warned, “Any crisis, I think you have to keep in mind that many things can happen – many twists and turns can occur.” “If you get massive business failures, you’ll face depression risk or financial crisis risk or both,” Bullard said. “And we want to stay out of those situations,”

Minneapolis Fed President Neel Kashkari said yesterday that “economic recovery is likely to be bumpy and it’s going to be more muted.” “My base-case scenario is that we are going to continue to see peaks, second waves, etcetera, unfortunately, for the rest of the year, until we get to some form of effective therapy or some form of vaccine or very, very widespread testing, and we are not there yet,” he added.

Looking ahead

UK retail sales and public sector net borrowing will be featured in European session. Germany will release PPI and current account. Later in the day, Canada will release retail sales while US will release current account balance.

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8966; (P) 0.9004; (R1) 0.9058; More…

Intraday bias in EUR/GBP remains neutral at this point. With 0.8866 minor support intact, further rise is in favor. On the upside, break of 0.9054 will resume the rebound from 0.8670 and target 61.8% retracement of 0.9499 to 0.8670 at 0.9182. However, firm break of 0.8866 will indicate completion of the rise from 0.8670. Intraday bias will be turned back to the downside for retesting 0.8670 support.

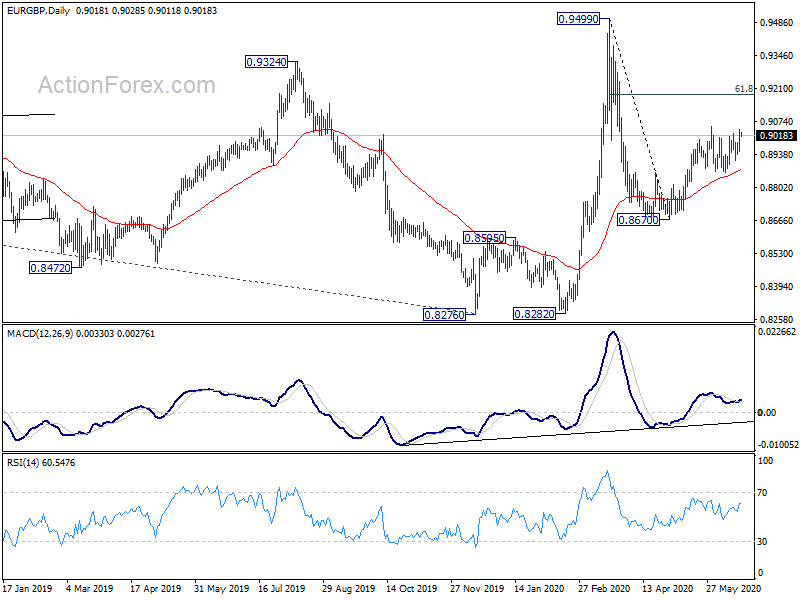

In the bigger picture, while the pull back from 0.9499 is deep, there is no sign of trend reversal yet. The up trend from 0.6935 (2015 low) should resume at a later stage to 61.8% projection of 0.6935 to 0.9263 from 0.8276 at 0.9715. This will remain the favored case as long as 0.8276 support holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | National CPI Core Y/Y May | -0.20% | -0.10% | -0.20% | |

| 23:50 | JPY | BoJ Minutes | ||||

| 06:00 | GBP | Retail Sales M/M May | -16.00% | -18.10% | ||

| 06:00 | GBP | Retail Sales Y/Y May | -22.60% | |||

| 06:00 | GBP | Retail Sales ex-Fuel Y/Y May | -18.20% | -18.40% | ||

| 06:00 | GBP | Retail Sales ex-Fuel M/M May | -15.00% | -15.20% | ||

| 06:00 | GBP | Public Sector Net Borrowing (GBP) May | 49.3B | 61.4B | ||

| 06:00 | EUR | Germany PPI M/M May | -0.30% | -0.70% | ||

| 06:00 | EUR | Germany PPI Y/Y May | -2.10% | -1.90% | ||

| 08:00 | EUR | Eurozone Current Account (EUR) Apr | 27.4B | |||

| 12:30 | CAD | Retail Sales M/M Apr | -14.00% | -10.00% | ||

| 12:30 | CAD | Retail Sales ex Autos M/M Apr | -7.30% | -0.40% | ||

| 12:30 | USD | Current Account (USD) Q1 | -101B | -110B |

{kind=link}