The financial markets are trading in risk-on mode as another week starts, boosted by last week’s record run in US equities. In addition to being supported by the set of solid job data, comments from White House economic adviser Gary Cohn also provided some optimism to investors. Nonetheless, in the currency markets, Dollar has turned into consolidative mode instead and is waiting for fresh inspirations. Euro, on the other hand, is regaining some growth. New Zealand Dollar and Yen are trading as the weakest ones so far. In other markets, gold failed to stand firm above 1280 handle last week and retreated on Dollar’s rebound. it’s hovering in tight range of 1260/5 for the moment. WTI crude oil is also struggling to regain momentum for another attempt of 50 handle yet.

US Cohn: Tax bill to be completed "early in the fall"

Comments from White House economic adviser Gary Cohn raised hopes of better US growth outlook. Cohn noted that the current US corporate tax rate, at 35%, is too high when compared with the average of 23% in OECD economies. Cohn reiterated that the government’s timetable of getting a comprehensive tax bill completed "early in the fall", adding that top priority "for now until the end of the year is taxes". Recall that pro-growth tax plan outlined by the Trump administration in April proposed a 15% rate. Trump also proposed to reduce the number of individual income tax bracket from seven to three, with the highest marginal tax bracket dropping from 39.6% to 33%.

Kiwi lower ahead of RBNZ

New Zealand Dollar trades notably lower today as RBNZ’s survey showed inflation expectation eased. The survey showed that respondents expect 1.77% annual inflation in 1 year and 2.09% in 2 years. That’s much lower than the survey result three months ago, at 1.92% in 1 year and 2.17% in 2 years. For growth, firms expected GDP to grow 2.7% in 1 year and 2.64% in 2 years, comparing to prior 2.81% and 2.58% respectively.

The data comes just head of RBNZ meeting this week on August 9, which is a major focus of the week. RBNZ is widely expected to stand pat and keep OCR unchanged at 1.75%. The central bank will likely maintain a dovish tone and keep its own forecast that rates would be on hold until September 2019.

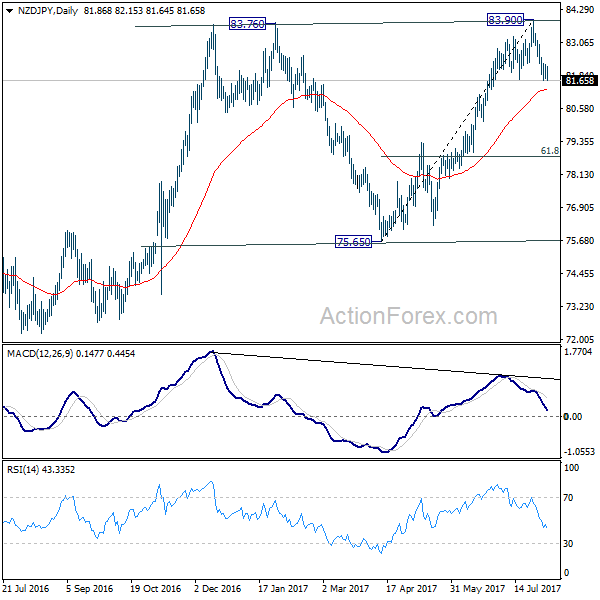

NZD/JPY’s breach of 81.66 support last week indicates short term topping at 83.90, after failing to sustain above 83.76 resistance. Bias is back on the downside for 55 day EMA (now at 81.29). Sustained break there should confirm completion of whole rise from 75.65. And deeper fall would then be seen back to 61.8% retracement of 75.65 to 83.90 at 78.80 and below before getting support for rebound.

Elsewhere, Japan leading index rose to 106.3 in June. German industrial production dropped -1.1% mom in June. Swiss foreign currency reserves rose to CHF 714b in July. Swiss CPI rose slightly to 0.3% yoy in July. Eurozone Sentix investor confidence is the only feature for today.

US CPI as main focus of the week

Looking ahead, US CPI is the most important data to watch. The July report, due Friday, probably shows that inflation improved to 1.8% yoy, from 1.6% in June. Core CPI probably stayed unchanged at 1.76. Both readings are expected to stay below the Fed’s target of 2%. Recall that the Fed delivered a dovish tone at the July meeting statement, noting that "on a 12-month basis, overall inflation and the measure excluding food and energy prices have declined and are running below 2%". In June the Fed only noted that inflation has "declined recently". It is advised to pay attention to the upcoming FOMC minutes and see if the Fed would continue to describe weak inflation as "transitory".

Here are some highlights for the week ahead:

- Tuesday: China trade balance; Australia business confidence; Swiss unemployment rate; German trade balance; Canada housing starts

- Wednesday: China PPI and CPI; Australia home loans; Canada building permits; US non-farm productivity

- Thursday: RBNZ rate decision; UK RICS house price balance; Japan domestic CGPI, tertiary industrial index; UK productions, trade balance; US jobless claims, PPI

- Friday: German CPI final, US CPI

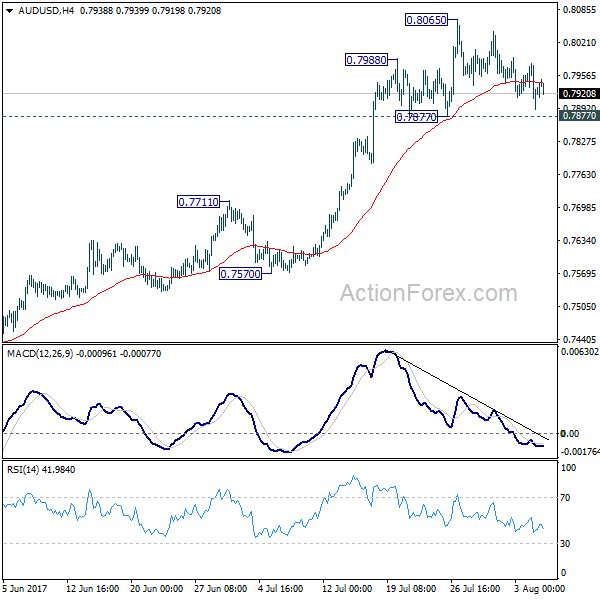

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7887; (P) 0.7933; (R1) 0.7975; More…

Intraday bias in AUD/USD remains neutral as consolidation from 0.8065 is still in progress. As long as 0.7877 support holds, another rise remains mildly in favor. Break of 0.8065 will target 100% projection of 0.6826 to 0.7833 from 0.7328 at 0.8335. Nonetheless, break of 0.7877 will indicate short term topping, with bearish divergence condition in 4 hour MACD. In such case, intraday bias will be turned back to the downside for 0.7711 resistance turned support.

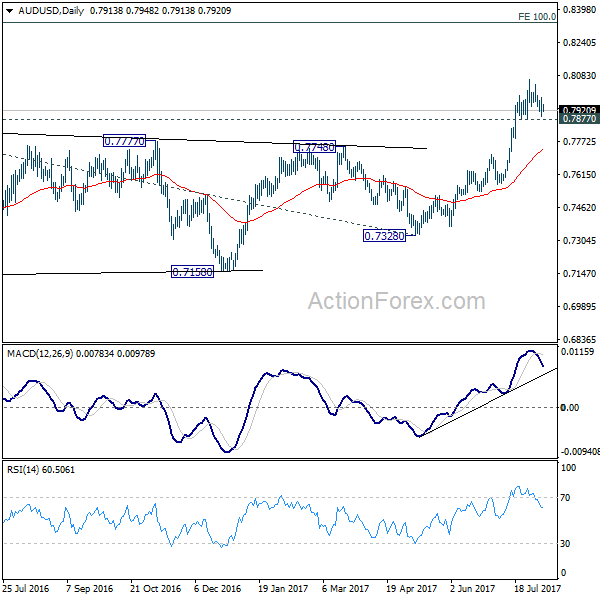

In the bigger picture, current development suggests that rebound from 0.6826 is developing into a medium term rise. There is no confirmation of trend reversal yet and we’ll continue to treat such rebound as a corrective pattern. But in any case, break of 55 month EMA (now at 0.8100) will target 38.2% retracement of 1.1079 to 0.6826 at 0.8451. Break of 0.7328 support is needed to confirm completion of the rebound. Otherwise, further rise is now expected.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 3:00 | NZD | RBNZ 2-Year Inflation Expectation Q3 | 2.10% | 1.90% | 2.20% | |

| 5:00 | JPY | Leading Index Jun P | 106.3 | 106.2 | 104.6 | |

| 6:00 | EUR | German Industrial Production M/M Jun | -1.10% | 0.20% | 1.20% | |

| 7:00 | CHF | Foreign Currency Reserves Jul | 714B | 693B | 694B | |

| 7:15 | CHF | CPI M/M Jul | -0.30% | -0.30% | -0.10% | |

| 7:15 | CHF | CPI Y/Y Jul | 0.30% | 0.30% | 0.20% | |

| 7:30 | GBP | Halifax Plc House Prices M/M Jul | 0.40% | 0.30% | -1.00% | -0.90% |

| 8:30 | EUR | Eurozone Sentix Investor Confidence Aug | 27.6 | 28.3 |