Sterling’s decline gathers some momentum on resurfacing no-deal Brexit risk. The Pound is currently followed by New Zealand Dollar as the second weakest. Canadian Dollar is the third worst performing so far, follow oil price lower. On the other hand, Yen and Dollar and trading firmer today, despite rebound in European stocks. Overall, though, trading is relatively subdued with US and Canada on holiday.

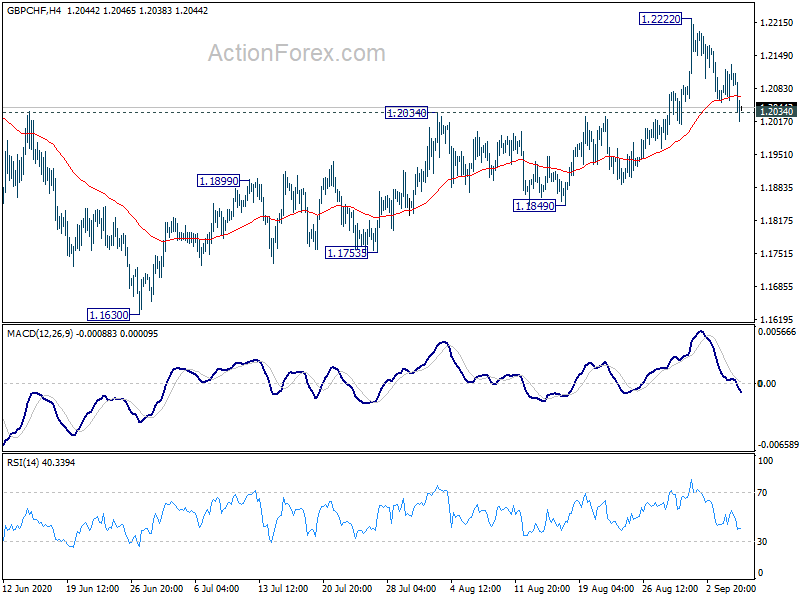

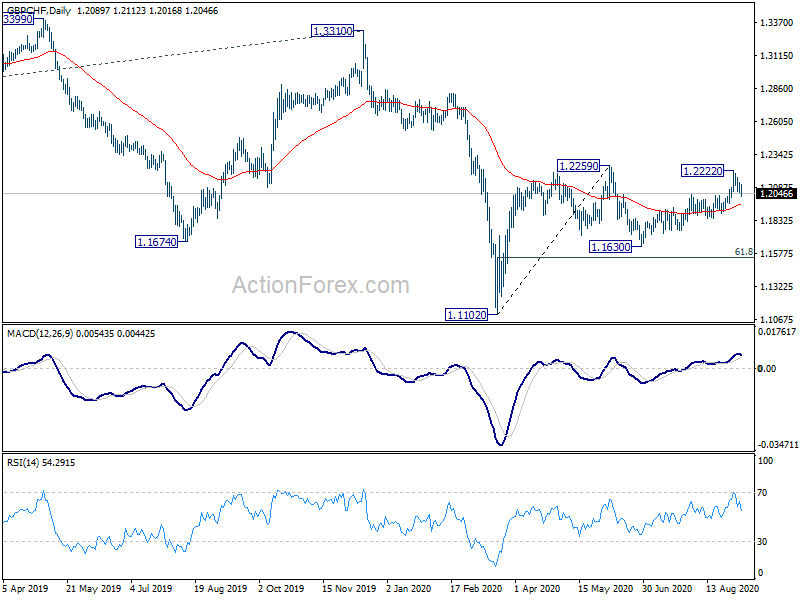

Technically, GBP/CHF’s break of 1.2034 resistance turned support suggests that choppy rebound from 1.1630 has completed at 1.2222, after rejection by 1.2259 resistance. Deeper decline is now in favor to 1.1849 support. Break will confirm that the range pattern from 1.2259 has started a falling leg to 1.1630 support. EUR/GBP’s break of 0.8974 suggests completion of the corrective fall fro m0.9175, ahead of 0.8864 support. Further rise would be seen back to 0.9148/9175 resistance zone. 138.24 support in GBP/USD and 1.3053 support in GBP/USD would be watched to confirm more underlying Sterling weakness.

In Europe, currently, FTSE is up 2.02%. DAX is up 1.67%. CAC is up 1.72%. Germany 10-year yield is down -0.0028 at -0.470. Earlier in Asia, Nikkei dropped -0.50%. Hong Kong HSI dropped -0.43%. China Shanghai SE dropped -1.87%. Singapore Strait Times rose 0.06%. Japan 10-year JGB yield rose 0.0031 to 0.042.

Eurozone Sentix investor confidence rose to -8, inflation risks on the rise

Eurozone Sentix Investor Confidence rose to -8 in September, up from -13.4, better than expectation of -10.8. That’s the fifth increase in a row, and the highest level since February. Current Situation Index rose to -33.0, up from -41.3, highest since March and fourth increase in a row. Expectations Index recovery to 20.8, up from 19.3.

Sentix said that overall, “the current recovery phase is similar to that of 2009, when we also saw a continuous improvement, which, as today, had little impact on stock market expectations.” Though, there are “clear signs of change on the bond markets”. “For our theme barometers show that the risks of inflation are on the rise again from the investors’ perspective. The corresponding sub-index for institutional investors fell to -15.5 points in September. This is the worst value since November 2018.

Also released, Germany industrial production rose 1.2% mom in July, below expectation of 4.8% mom. Swiss foreign currency reserves rose to CHF 848B in August.

EU warns WTO term is the way in event of no-deal Brexit

As Brexit negotiation is a main theme today, a European Commission spokesman said at a regular new briefing, “we are fully concentrated on making the most out of this week’s negotiating round… we share prime minister Johnson’s desire to reach a deal quickly. We will do everything in our power to reach an agreement.”

He warned, a no-deal Brexit would “inevitably create barriers to trade and cross border exchanges that do not exist today”. “I finally point out that while we are determined to reach an agreement with the UK, the EU will be ready – in the event of a no deal scenario – to trade with UK on WTO terms as of the first of January, 2021,” the spokesman said.

Separately, Commission President Ursula von der Leyen tweeted: “I trust the British government to implement the Withdrawal Agreement, an obligation under international law & prerequisite for any future partnership. Protocol on Ireland/Northern Ireland is essential to protect peace and stability on the island & integrity of the single market.”

Australia AiG services dropped to 42.5, all sectors in contraction, employment decreased significantly

Australia AiG Performance of Services Index dropped to 42.5 in August, down from 44.0. Looking at some details, employment plunged -7.9 pts to 39.4. But sales were steady, down -0.1 to 43.3. New orders also dropped -1.7 to 45.2. Average wages dropped -2.4 to 43.4.

All sectors remained in contraction in trend terms. AiG added, “the introduction of stage 4 restrictions in the greater Melbourne area following some optimism in July weighed heavily on business activity in Victoria and the impact was felt across other states. All indicators were firmly negative for August and employment decreased significantly from the previous month.”

China exports rose 9.5% in Aug, but imports contracted -2.1%

In USD terms, in August, China’s total international trade rose 4.2% yoy to USD 411.6B. Exports rose 9.5% yoy to USD 235.3B, above expectation of 7.1% yoy. Imports, however, dropped -2.1% yoy to USD 176.3B, well below expectation of 0.1% yoy. Trade surplus narrowed to USD 58.9B, but still above expectation of USD 49.8B.

Year-to-August, total trade dropped -3.6% yoy to USD 2854B. Exports dropped -2.3% yoy to USD 1572B. Imports dropped -5.2% to USD 1283B. Trade balance recorded USD 289B surplus.

With EU, year-to-August, total trade dropped -1.5% yoy to USD 401B. Exports rose 2.1% yoy to USD 245B. Imports dropped -6.8% yoy to USD 156B.

With US, year-to-August, total trade dropped -3.5% yoy to USD 344B. Exports dropped -3.6% to USD 266B. Imports dropped -2.9% yoy to USD 78B.

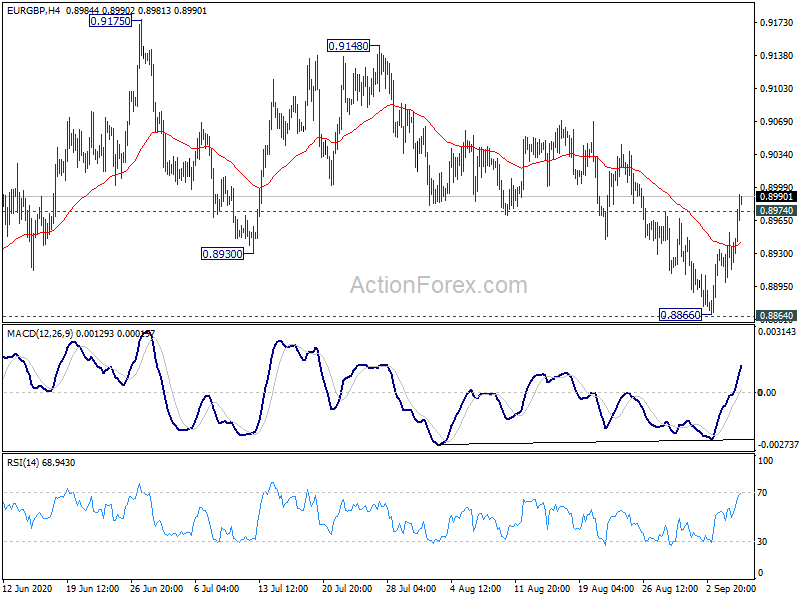

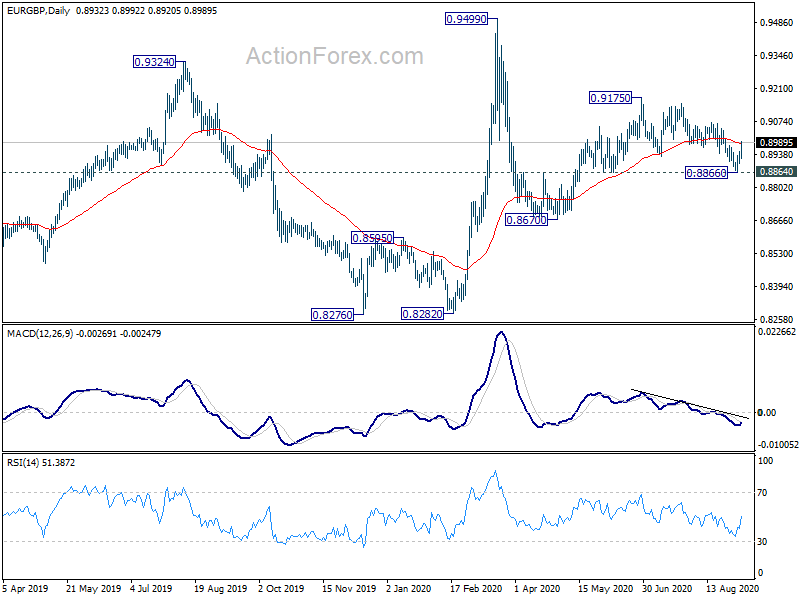

EUR/GBP Mid-Day Outlook

Daily Pivots: (S1) 0.8894; (P) 0.8923; (R1) 0.8946; More…

EUR/GBP’s rebound from 0.8866 extends higher today. Break of 0.8974 firstly indicates short term bottoming at 0.8866, ahead of 0.8864. More importantly, corrective decline from 0.9175 has possibly completed with three waves down to 0.8866. Rise from 0.8670 might be still in progress. Intraday bias is turned back to the upside for 0.9148/9175 resistance zone. Nevertheless, break of 0.8866 will resume the fall from 0.9175.

In the bigger picture, at this point, we’s still seeing the fall from 0.9499 as developing into a corrective pattern. That is, up trend form 0.6935 (2015 low) would resume at a later stage. This will remain the favored case as long as 0.8276 support holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:30 | AUD | AiG Performance of Services Index Aug | 42.5 | 44 | ||

| 3:15 | CNY | Trade Balance (USD) Aug | 58.9B | 49.8B | 62.3B | |

| 3:15 | CNY | Exports (USD) Y/Y Aug | 9.50% | 7.10% | 7.20% | |

| 3:15 | CNY | Imports (USD) Y/Y Aug | -2.10% | 0.10% | -1.40% | |

| 3:15 | CNY | Trade Balance (CNY) Aug | 417B | 385B | 442B | |

| 3:15 | CNY | Imports (CNY) Y/Y Aug | -0.50% | -0.70% | 1.60% | |

| 3:15 | CNY | Exports (CNY) Y/Y Aug | 11.60% | 2.10% | 10.40% | |

| 5:00 | JPY | Leading Economic Index Jul P | 86.9 | 84.6 | 85 | |

| 6:00 | EUR | Germany Industrial Production M/M Jul | 1.20% | 4.80% | 8.90% | 9.30% |

| 7:00 | CHF | Foreign Currency Reserves (CHF) Aug | 848B | 846B | 847B | |

| 8:30 | EUR | Eurozone Sentix Investor Confidence Sep | -8.0 | -10.8 | -13.4 |

{kind=link}