The markets are rather quiet in Asian session with Japan on holiday. Some selloff is seen in Hong Kong stocks but others simply ignored. The forex markets are generally stuck inside Friday’s range, with Dollar and Swiss Franc trading with a soft tone. On the other hand, Aussie and Sterling are so far the firmer ones. But again, range is tight and trading could remain subdued with a thin calendar today.

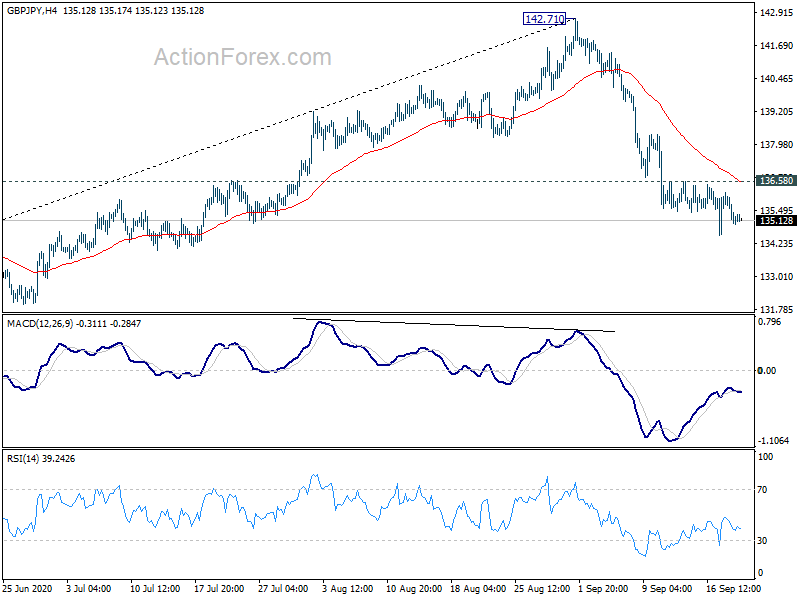

Technically, a focus is on whether Sterling has completed last week’s corrective recovery. Levels to watch include 1.2762 in temporary low in GBP/USD, 0.9291 temporary top in EUR/GBP and 134.57 temporary low in GBP/JPY. Or, Sterling is indeed staging a strong rebound through 1.3035 minor resistance in GBP/USD, 0.9067 support in EUR/GBP and 136.58 resistance in GBP/JPY. We’re preferring the former case but let’s see.

In Asia, currently, Hong Kong HSI is down -0.97%. China Shanghai SSE is down -0.42%. Singapore Strait Times is up 0.26%. Japan is on holiday.

UK manufacturers see no evidence of V sharp recovery

According to the Make UK/BDO Manufacturing Outlook Q3 survey, balance on investment intentions fell to -32% from -26% in the last quarter. Output and orders improved but were still way below historic averages. There were significant cuts to investment while employment prospects weakened. Forward looking indicators suggest conditions will improve albeit slowly. Overall, there was “no evidence of V shape recover”.

Also, Make UK is now forecasting manufacturing output to fall by -10.9% this year. 2021 recovery was downgraded by 6.2% to 5.1%. GDP is forecast to fall by -8.5% this year and recover by 10.1% in 2021.

PBoC kept LPR unchanged for the fifth straight month

China’s PBoC kept its benchmark lending rates unchanged for the fifth consecutive month today. The one-year Loan Prime Rate was held at 3.85%. Five-year LPR was kept at 4.65%. That was basically in line with market expectations.

Recent economic data from China suggested that the economy is on track for recovery. PBoC is expected to continue to stand pat, keeping the policy rate unchanged in the coming months. The main question now is when PBoC would start tightening up policy again. Some speculates that the LPR increase might come early next year.

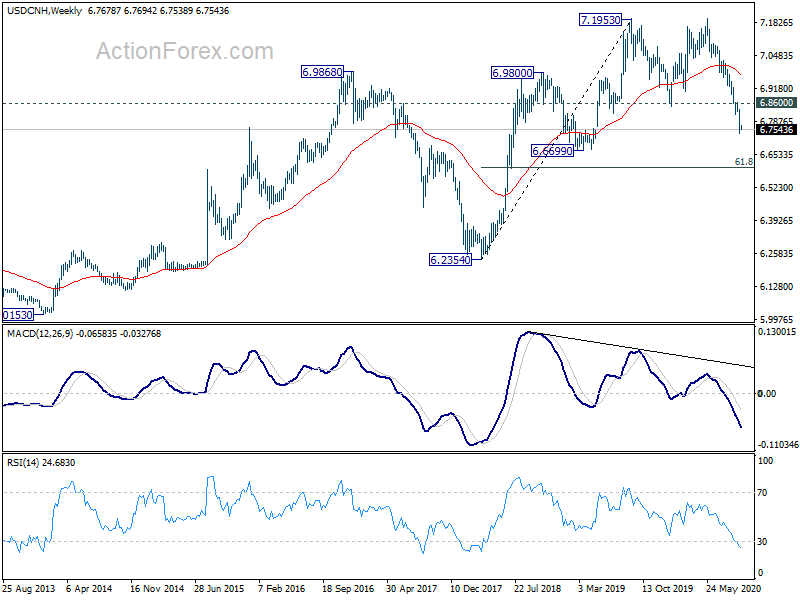

USD/CNH is now reversing the whole up trend from 2018 low at 6.2354 to 7.193. As long as 6.8600 near term resistance holds, USD/CNH would continue its decline to 6.6699 support, and possibly further to 61.8% retracement at 6.6021.

RBNZ and SNB to meet in a relatively light week

Two central bank will meet this week. RBNZ is expected to keep OCR at 0.25%. The intention to move to negative rates is clear, but RBNZ will hold fire for now. The question is whether Governor Adrian Orr would finally hint on a time line. SNB is expected to keep interest rate unchanged at -0.75%. The question is on whether Chairman Thomas Jordan would step up the tone on intervention to talk down the Franc. Fed chair Jerome Powell will deliver his testimony but he’s unlikely to provide anything new.

Here are some highlights for the week:

- Monday: UK Rightmove house price; Canada new housing price index.

- Tuesday: UK public sector net borrowing, CBI industrial order expectations; Eurozone consumer confidence; US existing home sales.

- Wednesday: Australia CBA PMIs; RBNZ rate decision; Japan PMI manufacturing, all industry index; Germany Gfk consumer climate; Eurozone PMIs; UK PMIs; US house price index, PMIs.

- Thursday: New Zealand trade balance; BoJ minutes; SNB rate decision; ECB monthly bulletin; Germany Ifo business climate; US jobless claims, new home sales.

- Friday: Japan corporate service price; Eurozone M3 money supply; US durable goods orders.

GBP/JPY Daily Outlook

Daily Pivots: (S1) 134.68; (P) 135.42; (R1) 135.89; More…

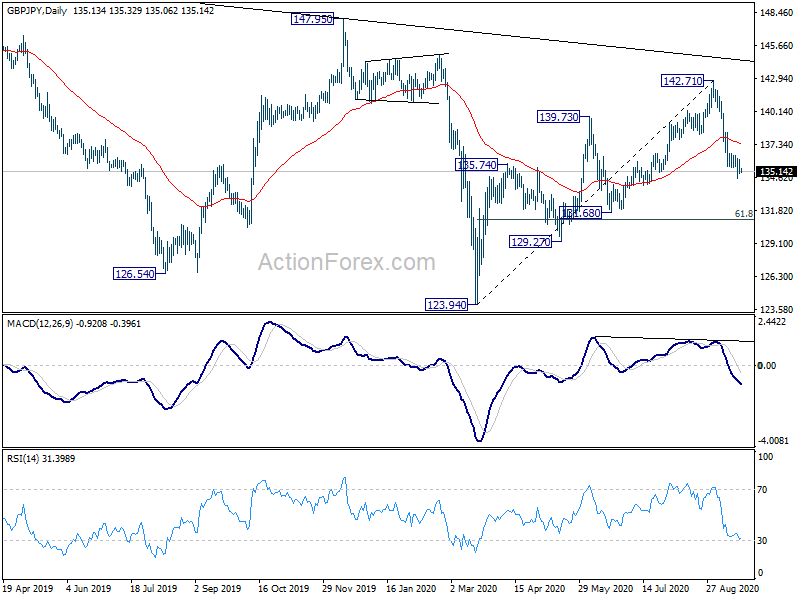

Intraday bias in GBP/JPY stays on the downside at this point. As noted before, whole corrective rebound from 123.94 should have completed at 142.71. Deeper fall would be seen to 61.8% retracement of 123.94 to 142.71 at 131.11 next. On the upside, above 136.58 minor resistance will turn bias neutral and bring consolidations, before staging another fall.

In the bigger picture, rise from 123.94 is seen only as a rising leg of the sideway consolidation pattern from 122.75 (2016 low). As long as 147.95 resistance holds, an eventual downside breakout remains in favor. However, firm break of 147.95 will raise the chance of long term bullish reversal. Focus will then be turned to 156.59 resistance for confirmation.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| EUR | German Buba Monthly Report | |||||

| 23:01 | GBP | Rightmove House Price Index M/M Sep | 0.20% | -0.20% | ||

| 12:30 | CAD | New Housing Price Index M/M Aug | 0.10% | 0.40% |

{kind=link}