Surging global yields remain the major focus today, with Germany 10-year bund yield hitting as high as -0.234, while UK 10-year gilt yield reaching as high as 0.818. Earlier in Asia, Japan 10-year JGB yield closed strongly at 0.152. US 10-year yield is also trading above 1.45. In the currency markets, Euro is trying to have a come back today and is currently trading as the strongest, followed by Canadian and then Aussie. Yen and Swiss Franc remain the weakest while Sterling softens as recent rally seems exhausted.

Technically, EUR/USD’s break of 1.2188 resistance should set the stage for further rise to retest 1.2348 high. EUR/GBP is worth a watch to gauge the strength of Euro’s rebound. Extending yesterday’s recovery, focus is now on 0.8653 minor resistance in EUR/GBP. Break there will indicate short term bottoming and bring strong rise back to 0.8737 support turned resistance.

In Europe, currently, FTSE is up 0.44%. DAX is down -0.01%. CAC is up 0.13%. German 10-year yield is up 0.0295 at 0.152. Earlier in Asia, Nikkei rose 1.67%. Hong Kong HSI rose 1.20%. China Shanghai SSE rose 0.59%. Singapore Strait Times rose 1.67%. Japan 10-year JGB yield rose 0.0295 to 0.152.

US durable goods orders rose 3.4% in Jan, initial jobless claims dropped to 730k

US durable goods orders rose 3.4% mom to USD 256.6B in January, above expectation of 1.1% mom. That’s the ninth straight month of growth. Ex-transport orders rose to 1.4% mom, above expectation of 0.7% mom. Ex-defense orders rose 2.3% mom. Transportation rose 7.8% to USD 85.1B.

Initial jobless claims dropped -111k to 730k in the week ending February 20, below expectation of 820k. Four-week moving average of initial claims dropped -20.5k to 807.8k. Continuing claims dropped -101k to 4419k in the week ending February 13. Four-week moving average of continuing claims dropped -91.5k to 4547k.

Q4 GDP growth was revised up to 4.1% annualized, according to the second estimate. That compared to Q3’s 33.4% annualized growth. The increase in real GDP reflected increases in exports, non-residential fixed investment, PCE, residential fixed investment, and private inventory investment that were partly offset by decreases in state and local government spending and federal government spending. Imports, which are a subtraction in the calculation of GDP, increased.

ECB Lane: Ensuring favourable financing conditions is central to restoring inflation momentum

ECB chief economist Philip Lane said in a speech, “ensuring favourable financing conditions is central to restoring inflation momentum and guiding the formation of inflation expectations”. And, “preservation of favourable financing conditions should involve the inspection of indicators along the whole transmission chain of our monetary policy”.

Within the broad-based set of indicators, “the downstream conditions facing the households and firms that rely on bank-based credit play a prominent role,” he said”. “Upstream indicators of risk-free OIS rates and sovereign yields are particularly important”.

Accordingly, “the ECB is closely monitoring the evolution of longer-term nominal bond yields,” Lane added.

Eurozone economic sentiment rose to 93.4 in Feb, EU rose to 93.4

Eurozone Economic Sentiment Indicator rose from 91.5 to 93.1 in February. Industrial confidence rose from -6.1 to -3.3. Services confidence dropped from -17.7 to -17.1. Consumer confidence rose from -15.5 to -14.8. Retail trade confidence dropped from -18.5 to -19.1. Employment Expectation Index rose from 89.1 to 90.0.

EU Economic Sentiment Indicator rose 1.9 pts to 93.4. Amongst the largest EU economies, the ESI rose markedly in Poland (+4.7), Italy (+4.4), Germany (+3.0)and, to a lesser extent, in France (+0.9). By contrast, sentiment worsened strongly in Spain (-3.2) and, more mildly so, in the Netherlands (-1.3).

Eurozone M3 money supply rose 12.5% yoy in January, matched expectations.

Germany Gfk consumer sentiment rose to -12.9, recovering from tough lockdown shock

Germany Gfk Consumer Sentiment for March improved to -12.9 in March, up 2.6 pts. For February, economic expectation rose notably from 1.3 to 8.0. Income expectations rose from -2.9 to 6.5. Propensity to buy rose from 0.0 to 7.4.

“Consumers are recovering to some extent from the shock they suffered after the tough lockdown in mid-December. The recent dip in infection rates and the launch of the vaccination program are fueling hopes of a speedy easing of measures,” says Rolf Bürkl, consumer expert at GfK.

New Zealand ANZ business confidence dropped to 7, overshoot in demand dissipating

New Zealand ANZ Business Confidence dropped to 7.0 in February, down from December’s 9.4, and preliminary reading of 11.8. Confidence was highest in retails at at 15.6, followed by construction at 12.9, services at 10.8 and manufacturing at 3.6. Agriculture confidence was at -38.1.

Own Activity Outlook rose to 21.3, up from 21.7, vs prelim. 22.3. Activity was highest in construction at 41.9, followed by services at 24.7, retail at 13.3, manufacturing at 10.7 and agriculture at 0.

ANZ said, “overshoot in demand resulting from the disruptions of 2020 is beginning to dissipate, and we expect the economy to go broadly sideways for a while as it digests the national income hit from the decimated tourism industry and as the housing market cools to something more sustainable.”

From Australia, private capital expenditure rose 3.0% in Q4 versus expectation of 0.6%.

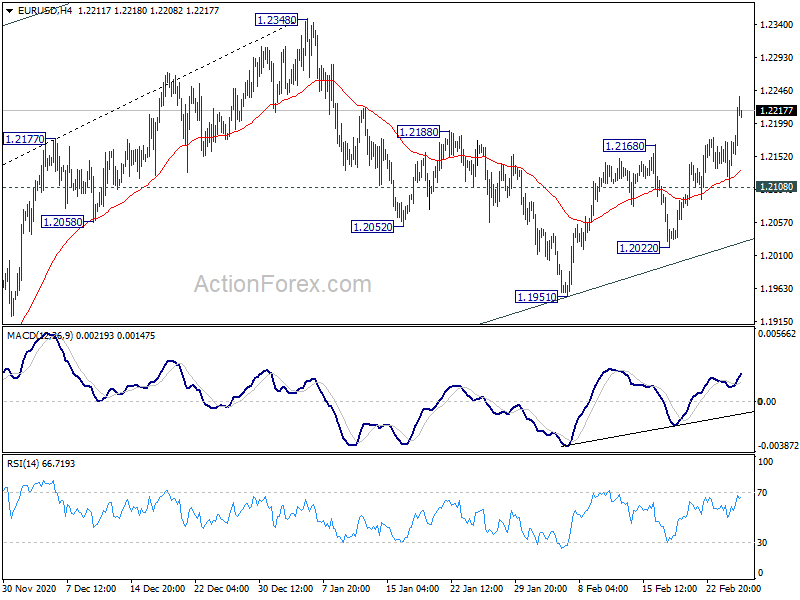

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2128; (P) 1.2151; (R1) 1.2194; More…

EUR/USD’s break of 1.2188 resistance should confirm completion of correction from 1.2348 at 1.1951. Intraday bias is back on the upside for retesting 1.2348 high first. Decisive break there will resume larger up trend from 1.0635, to 1.2555 key cluster resistance. On the downside, through, break of 1.2108 support will dampen this view and turn bias to the downside for 1.2022 support instead.

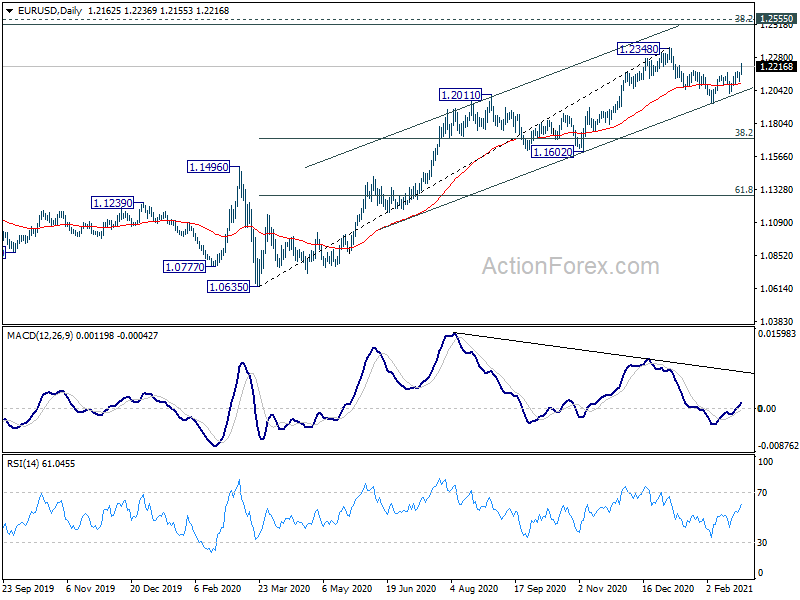

In the bigger picture, rise from 1.0635 is seen as the third leg of the pattern from 1.0339 (2017 low). Further rally could be seen to cluster resistance at 1.2555 next, (38.2% retracement of 1.6039 to 1.0339 at 1.2516). This will remain the favored case as long as 1.1602 support holds. We’d be alerted to topping sign around 1.2516/55. But sustained break there will carry long term bullish implications.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 00:00 | NZD | ANZ Business Confidence Feb F | 7 | 11.8 | 11.8 | |

| 00:30 | AUD | Private Capital Expenditure Q4 | 3.00% | 0.60% | -3.00% | |

| 07:00 | EUR | Germany Gfk Consumer Confidence Mar | -12.9 | -14 | -15.6 | -15.5 |

| 09:00 | EUR | Eurozone M3 Money Supply Y/Y Jan | 12.50% | 12.50% | 12.30% | |

| 10:00 | EUR | Eurozone Economic Sentiment Indicator Feb | 93.4 | 92.3 | 91.5 | |

| 10:00 | EUR | Eurozone Industrial Confidence Feb | -3.3 | -4.5 | -5.9 | -6.1 |

| 10:00 | EUR | Eurozone Business Climate Feb | -0.34 | -0.27 | ||

| 10:00 | EUR | Eurozone Services Sentiment Feb | -17.1 | -18.3 | -17.8 | -17.7 |

| 10:00 | EUR | Eurozone Consumer Confidence Feb F | -14.8 | -14.8 | -14.8 | -15.5 |

| 13:30 | USD | Initial Jobless Claims (Feb 19) | 730K | 820K | 861K | 841K |

| 13:30 | USD | GDP Annualized Q4 P | 4.10% | 4.10% | 4.00% | |

| 13:30 | USD | GDP Price Index Q4 P | 2.10% | 2.00% | 2.00% | |

| 13:30 | USD | Durable Goods Orders Jan | 3.40% | 1.10% | 0.50% | |

| 13:30 | USD | Durable Goods Orders ex Transportation Jan | 1.40% | 0.70% | 1.10% | |

| 15:00 | USD | Pending Home Sales M/M Jan | 0.20% | -0.30% | ||

| 15:30 | USD | Natural Gas Storage | -323B | -237B |

{kind=link}