Dollar retreat broadly today as 10-year yield pares gain after failing to sustain above 1.6 handle again. NASDAQ is also set for a rebound while DOW might try to extend the record run. At the time of writing, Yen, Euro and Sterling are following as the next weakest. Australian Dollar is currently the strongest one, followed by Swiss Franc and then New Zealand Dollar.

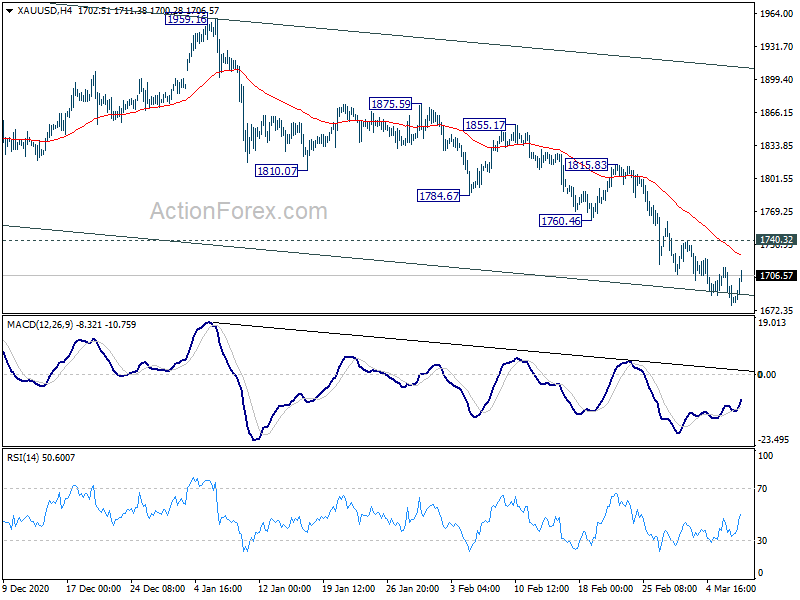

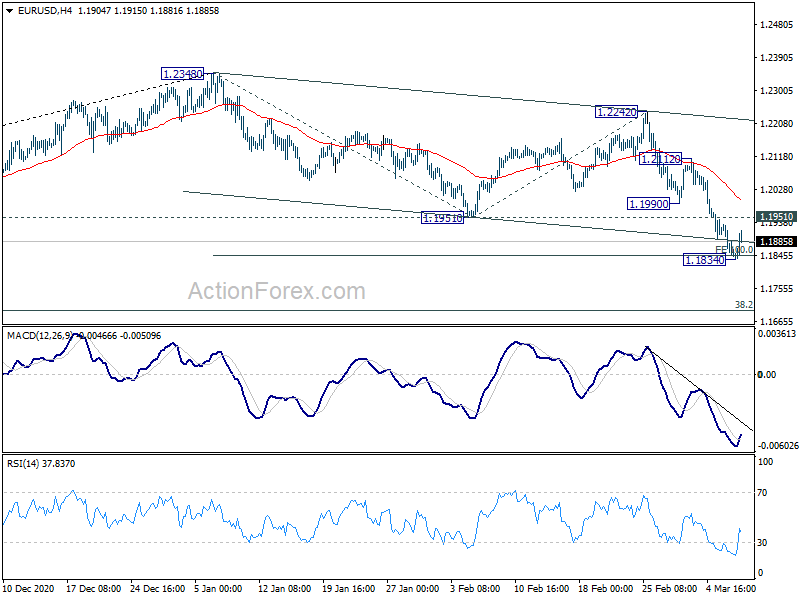

Technically, while Dollar retreats, there is no clear sign of topping yet. Some levels to watch will include 1.1951 minor resistance in EUR/USD, 1.4016 minor resistance in GBP/USD, 0.9256 minor support in USD/CHF and 108.08 minor support in USD/JPY. Also, break of 1740.32 minor resistance in Gold will also indicate short term bottoming, and be a sign of more Dollar pull back.

In Europe, currently, FTSE is up 0.27%. DAX is up 0.31%. CAC is up 0.20%. Germany 10-year yield is down -0.0508 at -0.324. Earlier in Asia, Nikkei rose 0.99%. Hong Kong HSI rose 0.81%. China Shanghai SSE dropped -1.82%. Singapore Strait Times rose 1.22%. Japan 10-year JGB yield rose 0.0079 to 0.130.

OECD upgrades 2021 global growth forecasts by 1.4% to 5.6%

OECD upgraded 2021 global growth forecasts as “prospects for a stronger economic recovery from the COVID-19 pandemic have improved with the gradual global vaccines rollout and stronger support from fiscal policy although gaps in economic performance are increasing across and within countries.”

Comparing with December projections:

- World GDP growth was revised up by 1.4% to 5.6% in 2021, revised up by 0.2% to 4.0% in 2022.

- G20 GDP growth was revised up by 1.5% to 6.2% in 2021, revised up by 0.4% to 4.1% in 2022.

- US GDP growth was revised up by 3.3% to 6.5% in 2021, revised up by 0.5% to 4.0% in 2022.

- Eurozone GDP growth, however, was revised up by only 0.3% to 3.9% in 2021, revised up by 0.5% to 3.8% in 2022.

- China GDP growth was revised down by -0.2% to 7.8% in 2021, unchanged at 4.9% in 2022.

- India GDP growth was revised up by 4.7% to 12.6% in 2021, revised up by 0.6% to 5.4% in 2022.

“Speed is of the essence,” said OECD Secretary-General Angel Gurría. “There is no room for complacency. Vaccines must be deployed faster and globally. This will require better international co-operation and co-ordination than we have seen up to now. It is only by doing so that we can focus our attention on building forward better and laying the foundations for a prosperous and lasting recovery for all.”

Eurozone Q4 GDP revised down to -0.7% qoq, EU contracted -0.5% qoq

Eurozone GDP dropped -0.7% qoq in Q3, revised down from prior estimate of -0.5% qoq. For the year 2020 as a whole, GDP dropped -6.6%. EU GDP contracted -0.5% qoq in Q4. For 2020 as a whole, GDP shrank -6.2%.

GDP growth by Member State: Romania (+4.8%) and Malta (+3.8%) recorded the sharpest increases of GDP compared to the previous quarter, followed by Croatia and Greece (both +2.7%). The strongest declines were observed in Ireland (-5.1%) and Austria (-2.7%) , followed by Italy (-1.9%) and France (-1.4%).

Also released in European session, Germany trade surplus widened to EUR 22.2B in January, versus expectation of EUR 17.9B. Italy industrial output rose 1.0% mom in January, versus expectation of 0.7% mom.

Japan household spending dropped -6.1% yoy in Jan

Japan household spending dropped -6.1% yoy in January, much worse than expectation of -2.1% yoy. That’s also the second straight month of decrease, as spending was dragged down by a second state of emergency. “With people refraining from going out under the state of emergency, outlays for items such as suits and dresses fell,” a Ministry of Internal Affairs and Communications official told reporters. Also released, nominal total cash earnings dropped -0.8% yoy in January, down for a 10th straight month.

In Q4, GDP growth was finalized at 2.8% qoq, 11.7% yoy. The figures were revised down form 3.0% qoq, 22.9% annualized. Capital expenditure grew 4.3% qoq. External demand rose 1.1% qoq. Private consumption rose 2.2% qoq. Price index rose 0.3% yoy.

The economy is expected to shrink in Q1 as it returned to pandemic restrictions. Prime Minister Yoshihide Suga last week extended the emergency through March 21 for the Tokyo region.

Australian NAB business confidence rose to 16, highest since early 2010

Australia NAB business confidence rose from 12 to 16 in February. That’s the highest level since early 2010, as all states and industries reported gains, except for retail. Business conditions rose from 9 to 15, also a multi-year high. Looking at some details, trading conditions rose from 13 to 21. Profitability conditions rose from 13 to 17. Employment conditions rose from 3 to 8.

“Businesses are the most optimistic they’ve been since 2010. This says the economy recovery has very strong momentum and even though government support is tapering, businesses are increasingly confident the economy will continue to improve,” said Alan Oster, NAB Group Chief Economist.

“Business conditions have rebounded to the very strong levels we saw in December and, importantly, employment conditions remain strong. Businesses are again expanding their workforce, which is key for supporting the labour market recovery.”

New Zealand ANZ business confidence dropped to 0, gains will be harder won

In the preliminary reading, New Zealand ANZ business confidence dropped from 7 to 0 in March. Own activity outlook also dropped from 21.3 to 17.4. Looking at some more details, export intensions rose form 5.1 to 6.0. Investment intentions dropped slightly from 15.6 to 14.4. Employment intentions jumped from 10.6 to 16.0. Pricing intentions rose from 46.2 to 48.9. Inflation expectations rose from 1.76 to 1.95.

ANZ said: “The economy is entering a phase in which gains will be harder won. The tourism sector pain is becoming more palpable, and booming sectors such as construction are running up against constraints in terms of the availability of labour and, increasingly, imported materials.”

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1815; (P) 1.1874; (R1) 1.1903; More….

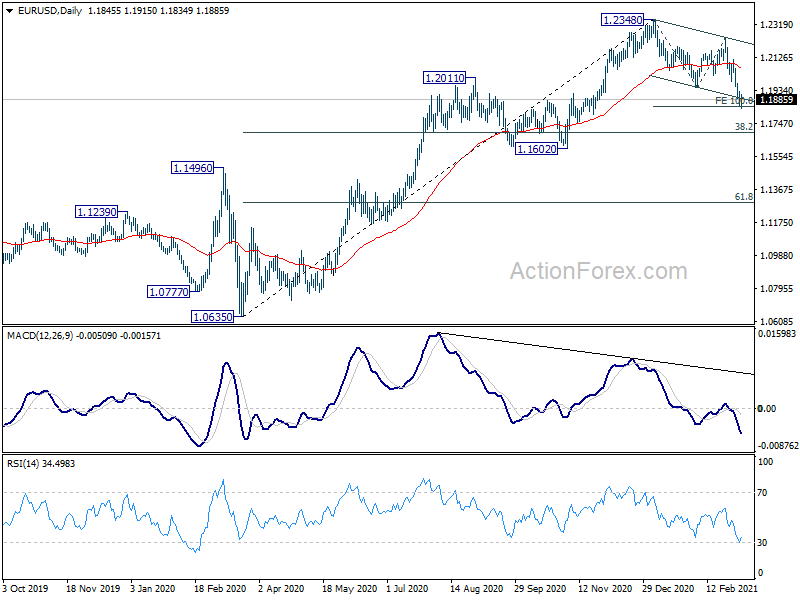

EUR/USD recovers after hitting 100% projection of 1.2348 to 1.1951 from 1.2242 at 1.1845. Intraday bias is turned neutral first. We’d continue to pay attention to bottoming signal at current level. On the upside, break of 1.1951 support turned resistance will indicate short term bottoming and turn bias to the upside. However, decisive break of 1.1845 will extend the correction to 38.2% retracement of 1.0635 to 1.2348 at 1.1694.

In the bigger picture, rise from 1.0635 is seen as the third leg of the pattern from 1.0339 (2017 low). Further rally could be seen to cluster resistance at 1.2555 next, (38.2% retracement of 1.6039 to 1.0339 at 1.2516). This will remain the favored case as long as 1.1602 support holds. We’d be alerted to topping sign around 1.2516/55. But sustained break there will carry long term bullish implications.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | Manufacturing Sales Q4 | -0.60% | 10.00% | 10.40% | |

| 23:30 | JPY | Labor Cash Earnings Y/Y Jan | -0.80% | -1.70% | -3.00% | |

| 23:30 | JPY | Overall Household Spending Y/Y Jan | -6.10% | -2.10% | -0.60% | |

| 23:50 | JPY | GDP Q/Q Q4 F | 2.80% | 3.00% | 3.00% | |

| 23:50 | JPY | GDP Deflator Y/Y Q4 | 0.30% | 0.20% | 0.20% | |

| 23:50 | JPY | Money Supply M2+CD Y/Y Feb | 9.60% | 9.50% | 9.40% | |

| 0:00 | NZD | ANZ Business Confidence Mar P | 0 | 7 | ||

| 0:01 | GBP | BRC Like-For-Like Retail Sales Y/Y Feb | 9.50% | 7.10% | ||

| 0:30 | AUD | NAB Business Confidence Feb | 16 | 10 | 12 | |

| 6:00 | JPY | Machine Tool Orders Y/Y Feb P | 36.70% | 9.70% | ||

| 7:00 | EUR | Germany Trade Balance (EUR) Jan | 22.2B | 17.9B | 16.1B | |

| 9:00 | EUR | Italy Industrial Output M/M Jan | 1.00% | 0.70% | -0.20% | |

| 10:00 | EUR | Eurozone GDP Q/Q Q4 | -0.70% | -0.60% | -0.60% | |

| 10:00 | EUR | Eurozone Employment Change Q/Q Q4 F | 0.30% | 0.30% | 0.30% | |

| 11:00 | USD | NFIB Business Optimism Index Feb | 95.8 | 96.2 | 95 |

{kind=link}