Commodity currencies remained generally pressured in Asian session today. While DOW and S&P 500 managed to reverse initial losses to close at new record highs, there is no follow through risk-on sentiment in Asia. Canadian Dollar is additionally weighed down with WTI crude oil dipping below 68 handle. Aussie is getting not particular support from the balanced RBA minutes. Yen and Swiss Franc are still the stronger ones, but Dollar is trying to catch up, against others.

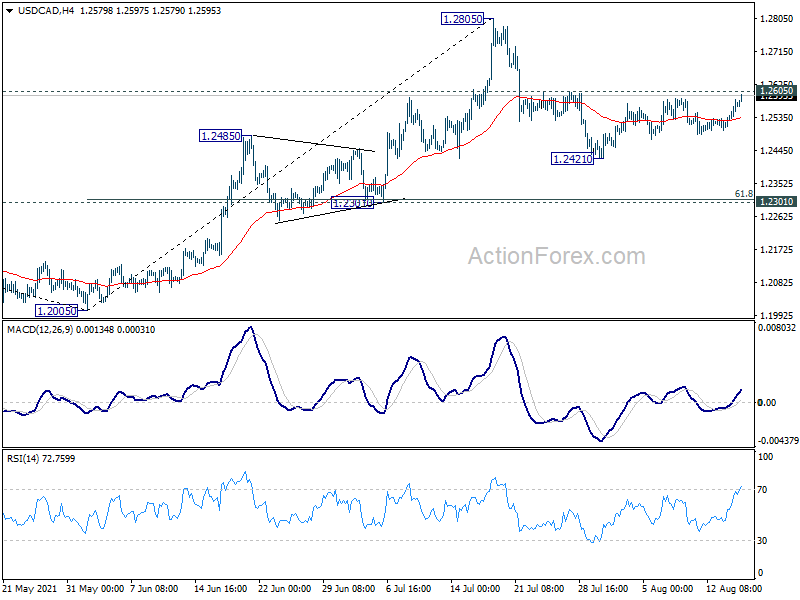

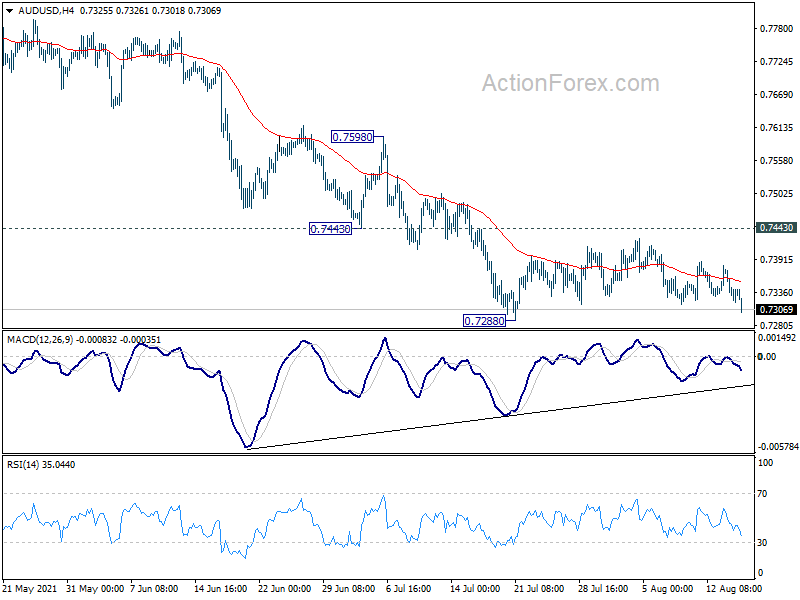

Technically, USD/CAD is now eyeing 1.2605 minor resistance as rebound from 1.2421 resumes. Firm break there will suggest that pull back from 1.2805 has already completed and bring retest of this high. At the same time, AUD/USD is dipping towards 0.7288 low. Break there will resume the larger decline from 0.8006. Both developments could signal further selling in commodity currencies elsewhere.

In Asia, at the time of writing, Nikkei is up 0.17%. Hong Kong HSI is down -0.40%. China Shanghai SSE is down -0.43%. Singapore Strait Times is down -0.48%. Japan 10-year JGB yield is up 0.0031 at 0.020. Overnight, DOW rose 0.31%. S&P 500 rose 0.26%. NASDAQ dropped -0.20%. 10-year yield dropped -0.040 to 1.257.

RBA minutes: Central scenario still for the economy to growth strongly again next year

In the minutes of August 3 meeting, RBA said recent outbreaks of the Delta variant of had “interrupted the recovery”. But the economy entered lockdowns with “more momentum than previously expected”, with fiscal and monetary support already cushion the economic effects. It added, “experience to date had been that, once virus outbreaks were contained, the economy bounced back quickly.” The “central scenario” was still for the economy to “growth strongly again next year”.

Committee members considered the case to delay tapering of asset purchases to AUD 4B a week scheduled for September. But they noted that additional bond purchases would only have a “marginal effect” at present”, but “maximum effect” during the resumption of strong growth in 2022. Also fiscal policy is recognized as a “more appropriate instrument” in response to a “temporary, localized reduction in incomes”. Thus, the Board reaffirmed the previously announced schedule for tapering.

RBA also reiterated that the condition for raising interest rate is not expected to be met before 2024. “Meeting this condition will require the labour market to be tight enough to generate wages growth that is materially higher than it is currently,” it said.

Fed Rosengren wouldn’t want to wait any later than December on tapering

Boston Fed President Eric Rosengren said the US had over 900k jobs growth for two months in a row and unemployment rate dropped by half a percent to 5.4%. He added, “if we get another strong labor market report, I think that I would be supportive of announcing in September that we are ready to start the taper program.”

“I think it’s appropriate to start in the fall. That would be October or November,” Rosengren told CNBC. “I certainly wouldn’t want to wait any later than December. My preference would be probably for sooner rather than later.” He also said that “there’s no reason to drag it out as long as the economy continues to progress as we expect.”

On the other hand, he’d prefer to see more progress before moving on to raising interest rate. “The criteria for starting to raise rates is that we see outcomes that are consistent with sustainable inflation at a little bit above 2%,” he reiterated Fed’s general position.

Looking ahead

UK employment data and Eurozone GDP will be featured in European session. Canada housing starts and foreign securities purchases will be released later in the day. But main focus will be on US retail sales, while industrial production, business inventories and NAHB housing index will be released too.

AUD/USD Daily Report

Daily Pivots: (S1) 0.7312; (P) 0.7343; (R1) 0.7365; More…

AUD/USD dips notably in Asian session but stays above 0.7288 low. Intraday bias remains neutral first. As long as 0.7443 resistance holds, outlook stays bearish for further decline. On the downside, break of 0.7288 will resume the fall from 0.8006 to 161.8% projection of 0.8006 to 0.7530 from 0.7890 at 0.7120 next. On the upside, break of 0.7443 will bring stronger rebound to 0.7530 support turned resistance instead.

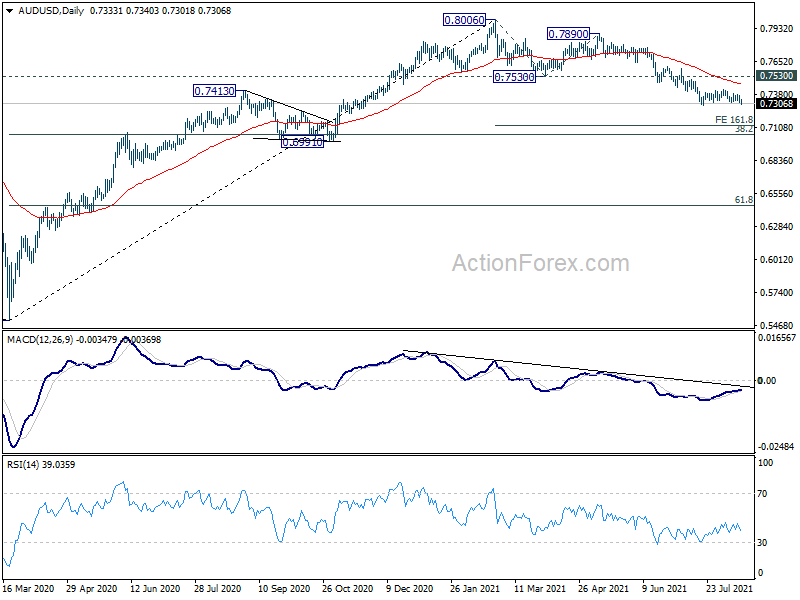

In the bigger picture, rise from 0.5506 medium term bottom could have completed at 0.8006, after failing 0.8135 key resistance. Correction from there could target 0.6991 cluster support (38.2% retracement of 0.5506 to 0.8006 at 0.7051). We’d look for strong support from there to bring rebound. However, sustained break of this level would argue that the whole medium term trend has indeed reversed.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 01:30 | AUD | RBA Meeting Minutes | ||||

| 04:30 | JPY | Tertiary Industry Index M/M Jun | 1.80% | -2.70% | ||

| 06:00 | GBP | Claimant Count Change Jul | -114.8K | |||

| 06:00 | GBP | ILO Unemployment Rate (3M) Jun | 4.80% | 4.80% | ||

| 06:00 | GBP | Average Earnings Excluding Bonus 3M/Y Jun | 7.40% | 6.60% | ||

| 06:00 | GBP | Average Earnings Including Bonus 3M/Y Jun | 8.70% | 7.30% | ||

| 09:00 | EUR | Eurozone GDP Q/Q Q2 P | 2.0% | 2.0% | ||

| 09:00 | EUR | Eurozone Employment Change Q/Q Q2 P | -0.50% | -0.30% | ||

| 12:15 | CAD | Housing Starts Jul | 275K | 282K | ||

| 12:30 | CAD | Foreign Securities Purchases (CAD) Jun | 20.79B | |||

| 12:30 | USD | Retail Sales M/M Jul | -0.20% | 0.60% | ||

| 12:30 | USD | Retail Sales ex Autos M/M Jul | 0.10% | 1.30% | ||

| 13:15 | USD | Industrial Production M/M Jul | 0.40% | 0.40% | ||

| 13:15 | USD | Capacity Utilization Jul | 75.70% | 75.40% | ||

| 14:00 | USD | Business Inventories Jun | 0.80% | 0.50% | ||

| 14:00 | USD | NAHB Housing Market Index Aug | 80 | 80 |

{kind=link}