Dollar continues to pare gains in early US session as the week is coming to a close. PCE inflation data is largely ignored by the markets, while Euro also shrugs CPI. Canadian Dollar also ignores smaller than expected GDP contraction. Sterling is leading the way in the rebound, followed by Aussie. As for the week, the greenback is still in favor to close as the best performer, while New Zealand Dollar is the worst.

In Europe, at the time of the writing, FTSE is down -0.59%. DAX is down -0.31%. CAC is down -0.05%. Germany 10-year yield is down -0.039 at -0.236. Earlier in Asia, Nikkei dropped -2.31%. Japan 10-year JGB yield dropped -0.0145 to 0.055. Singapore Strait Times dropped -1.15%. China and Hong Kong were on holiday.

US PCE price index rose to 4.3% in Aug, core PCE unchanged at 3.6%

US personal income rose 0.2% mom, or USD 35.5B, in August, matched expectations. Personal spending rose 0.8% mom, or USD 130.5B, above expectation of 0.7% mom.

Headline PCE price index rose to 4.3% yoy, up from 4.2% yoy, above expectation of 3.9% yoy. Core PCE price index was unchanged at 3.6% yoy, matched expectations.

Canada GDP contracted -0.1% mom in Jul, to rise 0.7% mom in Aug

Canada GDP dropped -0.1% mom in July, better than expectation of -0.2% mom. Total activity remains -2% below pre-pandemic level in February 2020. Overall, 13 of 20 industrial sectors were up. Preliminary information indicates approximate 0.7% rise in real GDP for August.

Eurozone CPI jumped to 3.4% yoy in Sep, core CPI rose to 1.9% yoy

Eurozone CPI accelerated to 3.4% yoy in September, up from 3.0% yoy, above expectation of 3.3% yoy. Core CPI rose to 1.9% yoy, up from 1.6% yoy, above expectation of 1.8% yoy.

Looking at the main components of euro area inflation, energy is expected to have the highest annual rate in September (17.4%, compared with 15.4% in August), followed by non-energy industrial goods (2.1%, compared with 2.6% in August), food, alcohol & tobacco (2.1%, compared with 2.0% in August) and services (1.7%, compared with 1.1% in August).

Eurozone PMI manufacturing finalized at 58.6, growing toll from supply chain headwinds

Eurozone PMI Manufacturing was finalized at 58.6 in September, down from August’s 61.4. That was the largest drop in the headline index since April 2020 as supply-side constraints impacted goods producers. Acute inflationary pressures persisted as supplier deliver time continued to lengthen considerably.

Chris Williamson, Chief Business Economist at IHS Markit said: “While Eurozone manufacturing expanded at a robust pace in September, growth has weakened markedly as producers report a growing toll from supply chain headwinds… The supply situation should start to improve now that COVID-19 cases are falling and vaccination rates are improving in many countries, notably in several key Asian economies from which many components are sourced, but it will inevitably be a slow process which could see the theme of supply issues and rising prices run well into 2022.”

Germany PMI Manufacturing was finalized at 58.4 in September, down from August’s 62.6. Markit said output and new orders rose at slowest rate in 15 months. Input shortages continued to push up costs, leading to higher output prices. Pace of job creation slowed as growth expectations dipped to 13-month low.

France PMI Manufacturing was finalized at 55.0 in September, down from August’s 57.5, lowest since January. Markit said that input lead times deteriorated at unprecedented rate prior to COVID-19. Output growth lost further momentum amid supply-side challenges. New order growth softened further.

UK PMI manufacturing finalized at 57.1, descending towards a bout of stagflation

UK PMI Manufacturing was finalized at 57.1 in September, down from August’s 60.3. Markit said output and new orders rose at slowest rates since February. New export business fell for the first time in eight months.

Rob Dobson, Director at IHS Markit, said: “The September PMI highlights the risk of the UK descending towards a bout of ‘stagflation’, as growth of manufacturing output and new orders eased sharply while input costs and selling prices continued to surge higher…. With little sign of resolution to these issues, manufacturers, especially smaller firms with lower market power or capacity flexibility, will continue to be buffeted by these headwinds for the foreseeable future, hinting at a tough autumn and winter ahead for many firms.”

BoJ opinions: No significant change in the situation in Japan

In the Summary of Opinions of BoJ’s September 21-22 meeting, it’s noted, “since there is no significant change in the situation in Japan where economic activity, such as of firms, has been supported by accommodative financial conditions, it is appropriate for the Bank to maintain the current monetary policy measures”.

One opinion also noted, “although financial markets have been stable on the whole, it is necessary to be vigilant in closely monitoring economic and financial developments, including the impact of developments in the Chinese real estate sector on global financial markets, and be ready to respond promptly if necessary.”

Japan Tankan large manufacturing index rose to 18, highest since 2018

Japan’s Tankan large manufacturing index rose from 14 to 18 in Q3, above expectation of 13. That’s the highest level since 2018. Large manufacturing outlook rose from 13 to 14, below expectation of 15. Non-manufacturing index rose from 1 to 2, above expectation of 0. Non-manufacturing outlook was unchanged at 3, below expectation of 5.

Large companies expected to expand capital investment by 10.1% in the fiscal year started April, risen from prior indication of 9.6%. Inflation is expected to be 0.7% a year from now, slightly higher than 0.6% as expected in prior survey.

Japan PMI manufacturing finalized at 51.5

Japan PMI Manufacturing was finalized at 51.5 in September, down from August’s 52.7. Markit noted renewed reductions in production and incoming business. Cost burdens has the sharpest rise in 13 years amid supply chain disruption. Businesses confidence, however, strengthened for the first time in three months.

Also released, unemployment rate was unchanged at 2.8% in August.

Australia AiG manufacturing dropped to 51.2, recovery all-but-stalled

Australia AiG Performance of Manufacturing Index dropped from 51.6 to 51.2 in September. Looking at some details, production rose 2.9 to 53.1. Employment dropped from -4.3 to 47.1. New orders dropped -5.1 to 52.0. Exports rose 6.8 to 51.9.

Ai Group Chief Executive Innes Willox said: “The recovery in the manufacturing sector over the past year all-but-stalled in September as the impacts of lockdowns and border closures constrained activity in the two largest states…. Manufacturers are hoping that the prospect of restrictions being wound back will see a strong lift in performance over coming months.”

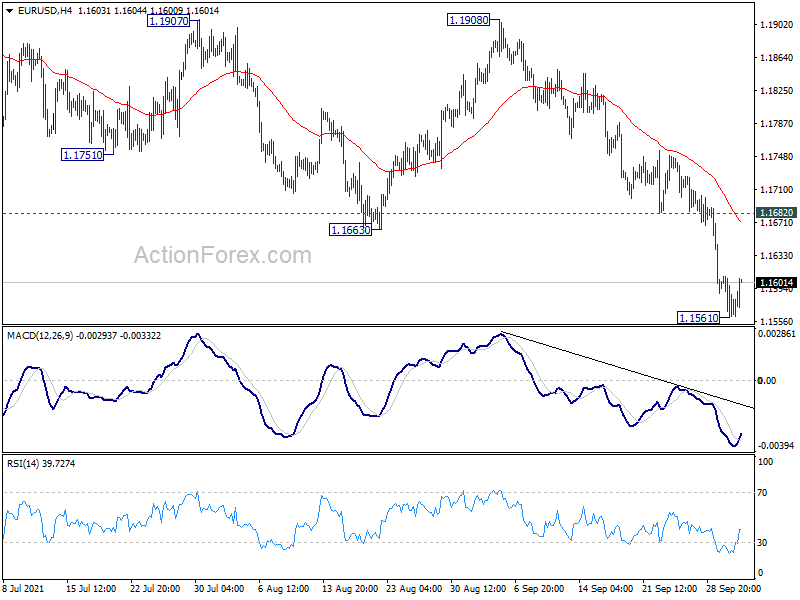

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1556; (P) 1.1583; (R1) 1.1603; More…

Intraday bias in EUR/USD is turned neutral with 4 hour MACD crossed above signal line. Upside of recovery should be limited by 1.1682 resistance to bring another fall. On the downside, break of 1.1561 will extend the whole fall from 1.2348, as a correction to whole rise from 1.0634. Next target is 1.1289 medium term fibonacci level. Nevertheless, sustained break of 1.1682 will bring stronger rebound back towards 1.1908 resistance.

In the bigger picture, sustained break of 1.1602 will argue that rise from 1.0635 (2020 low) has completed at 1.2348. Deeper fall would be seen to 61.8% retracement of 1.0635 to 1.2348 at 1.1289. Note also that the firm break of 55 week EMA (1.1830) also carries medium term bearish implication. Firm break of 1.1289 will pave the way to retest 1.0635 low. On the upside, though, break of 1.1908 resistance will revive medium term bullishness and turn focus back to 1.2348 high.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Tankan Large Manufacturing Index Q3 | 18 | 13 | 14 | |

| 23:50 | JPY | Tankan Large Manufacturing Outlook Q3 | 14 | 15 | 13 | |

| 23:50 | JPY | Tankan Non-Manufacturing Index Q3 | 2 | 0 | 1 | |

| 23:50 | JPY | Tankan Non-Manufacturing Outlook Q3 | 3 | 5 | 3 | |

| 23:50 | JPY | Tankan Large All Industry Capex Q3 | 10.10% | 9.10% | 9.60% | |

| 23:30 | JPY | Unemployment Rate Aug | 2.80% | 2.90% | 2.80% | |

| 23:50 | JPY | BoJ Summary of Opinions | ||||

| 00:30 | JPY | Manufacturing PMI Sep F | 51.5 | 51.2 | 51.2 | |

| 05:00 | JPY | Consumer Confidence Index Sep | 37.8 | 38.9 | 36.7 | |

| 06:00 | EUR | Germany Retail Sales M/M Aug | 1.10% | 1.60% | -5.10% | |

| 07:30 | CHF | SVME PMI Sep | 68.1 | 65.6 | 67.7 | |

| 07:45 | EUR | Italy Manufacturing PMI Sep | 59.7 | 60.1 | 60.9 | |

| 07:50 | EUR | France Manufacturing PMI Sep F | 55 | 55.2 | 55.2 | |

| 07:55 | EUR | Germany Manufacturing PMI Sep F | 58.4 | 58.5 | 58.5 | |

| 08:00 | EUR | Eurozone Manufacturing PMI Sep F | 58.6 | 58.7 | 58.7 | |

| 08:30 | GBP | Manufacturing PMI Sep F | 57.1 | 56.3 | 56.3 | |

| 09:00 | EUR | Eurozone CPI Y/Y Sep P | 3.40% | 3.30% | 3.00% | |

| 09:00 | EUR | Eurozone CPI Core Y/Y Sep P | 1.90% | 1.80% | 1.60% | |

| 12:30 | CAD | GDP M/M Jul | -0.10% | -0.20% | 0.70% | |

| 12:30 | USD | Personal Income M/M Aug | 0.20% | 0.20% | 1.10% | |

| 12:30 | USD | Personal Spending Aug | 0.80% | 0.70% | 0.30% | -0.10% |

| 12:30 | USD | PCE Price Index M/M Aug | 0.40% | 0.40% | ||

| 12:30 | USD | PCE Price Index Y/Y Aug | 4.30% | 3.90% | 4.20% | |

| 12:30 | USD | Core PCE Price Index M/M Aug | 0.30% | 0.20% | 0.30% | |

| 12:30 | USD | Core PCE Price Index Y/Y Aug | 3.60% | 3.60% | 3.60% | |

| 13:30 | CAD | Manufacturing PMI Sep | 57.2 | |||

| 13:45 | USD | Manufacturing PMI SepF | 60.2 | 60.5 | ||

| 14:00 | USD | Michigan Consumer Sentiment Index Sep | 71 | 71 | ||

| 14:00 | USD | ISM Manufacturing PMI Sep | 59.9 | 59.9 | ||

| 14:00 | USD | ISM Manufacturing Prices Paid Sep | 83.8 | 79.4 | ||

| 14:00 | USD | ISM Manufacturing Employment Index Sep | 49 | |||

| 14:00 | USD | Construction Spending M/M Aug | 0.30% | 0.30% |

{kind=link}