Yen stays general firm after earlier rally today, and Dollar is following. Euro shrugs off better than expected German economic sentiment data. Sterling and Swiss Franc are mixed. Australian and New Zealand Dollar are currently the weakest. Gold is firm but there is no follow through buying through 1833.79 key resistance. WTI oil treads water at around 82 handle. A focus is whether benchmark yields in US and Europe would extend recent decline.

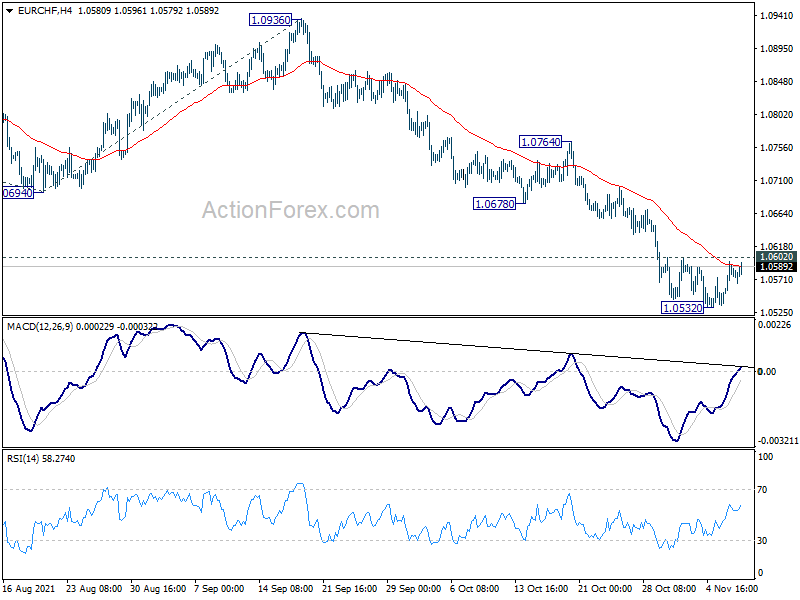

Technically, EUR/CHF would be a pair to watch today as it’s struggling to extend rebound from 1.0532. Yet, break of 1.0602 resistance will indicate short term bottoming, and should bring stronger rise back to 1.0678 support turned resistance. If happens, that might help lift EUR/USD through 1.1615 minor resistance to 1.1691 near term resistance level.

In Europe, at the time of writing, FTSE is down -0.06%. DAX is up 0.19%. CAC is up 0.23%. Germany 10-year yield is down -0.039 at -0.282. Earlier in Asia, Nikkei dropped -0.75%. Hong Kong HSI rose 0.20%. China Shanghai SSE rose 0.24%. Singapore Strait Times dropped -0.63%. Japan 10-year JGB yield rose 0.0048 to 0.066.

US PPI up 0.6% mom, 8.6% yoy in Oct

US PPI for final demand rose 0.6% mom in October, above expectation of 0.5% yoy. For the 12 months period, PPI was unchanged at 8.6% yoy, slightly below expectation of 8.7% yoy.

PPI core came in at 0.4% mom, 6.8% yoy, versus expectation of 0.5% mom, 6.8% yoy.

ECB Klass: Transitory pressures are not necessarily short-lived

ECB Governing Council member Klaas Knot reiterated that inflation remains “largely transitory” but “upside risks to this baseline dominate”. Though “we need to prepare for upside scenarios as well,” he added.

“These transitory pressures are not necessarily short-lived,” Knot said. “In fact, we have come to realize that the inflationary pressures from these sources last longer than initially thought.”

He also said that ECB shouldn’t tie itself up, as “we cannot make long-lasting unconditional commitments that might end up being incompatible with how the inflation outlook develops”. But still, conditions for a rate hike are “very unlikely” to be met next year.

German ZEW economic sentiment rose to 31.7, but current situation dropped to 12.5

Germany ZEW Economic Sentiment rose to 31.7 in November, up from 22.3, well above expectation of 20.3. That’s also the first rise since May. Current Situation, however, worsened again and dropped sharply from 21.6 to 12.5, well below expectation of 19.4.

Eurozone ZEW Economic Sentiment rose from 21.0 to 25.9, above expectation of 20.6. Current situation dropped -4.3 pts to 11.6. Inflation expectations for Eurozone dropped very sharply by -31.4 pts to -14.3. This shows that the experts expect the inflation rate in the eurozone to decline over the next six months.

“Financial market experts are more optimistic about the coming six months. However, the renewed decline in the assessment of the economic situation shows that the experts assume that the supply bottlenecks for raw materials and intermediate products as well as the high inflation rate will have a negative impact on the economic development in the current quarter. For the first quarter of 2022, they expect growth to pick up again and inflation to fall both in Germany and the eurozone,” comments ZEW President Professor Achim Wambach on current expectations.

Also released, Germany trade surplus narrowed to EUR 13.2B in September, versus expectation of EUR 14.2B. France trade deficit widened slightly to EUR -6.8B, versus expectation of EUR -7.0B.

Australia NAB business confidence rose to 21 in Oct, conditions rose to 11

Australia NAB business confidence rose sharply from 10 to 21 in October. Business conditions rose from 5 to 11, back above long-run average. Trading conditions rose from 10 to 17. Profitability conditions rose from 2 to 8. Employment conditions rose from 1 to 6.

“The large improvement in forward orders provides further evidence of the strong rebound in economic activity that is underway,” said NAB Chief Economist Alan Oster. “Businesses can see that conditions are improving and that momentum should continue over coming months.”

“We are starting to see some price pressures, but these remain largely in the form of pressure on input costs,” said Oster. “These pressures should pull back as global supply chain disruptions ease and labour markets normalise, although this process may take some time yet.”

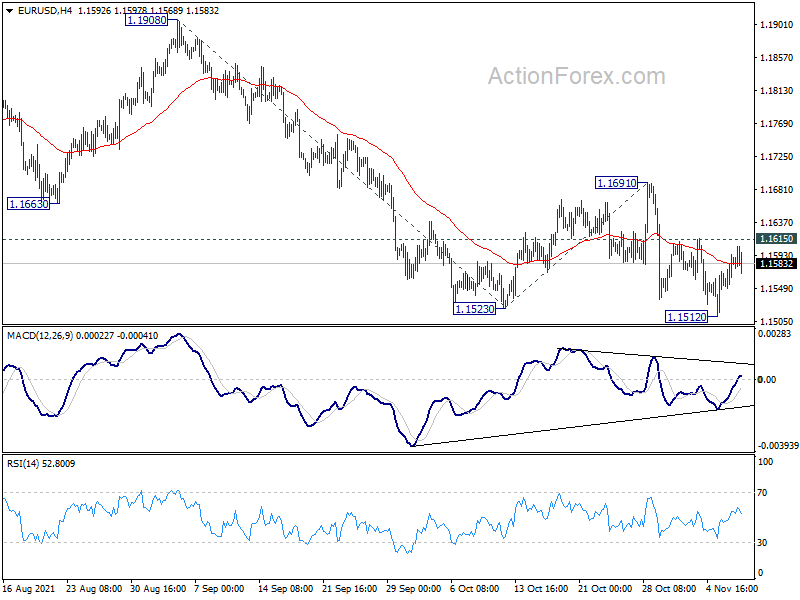

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1561; (P) 1.1578; (R1) 1.1605; More…

EUR/USD is still staying in range of 1.1512/1615 and intraday bias remains neutral. Further decline is in favor as long as 1.1615 minor resistance holds. Break of 1.1512 will extend the pattern from 1.2348 to 61.8% projection of 1.1908 to 1.1523 from 1.1691 at 1.1453. Break will pave the way to 100% projection at 1.1306. On the upside, though, above 1.1615 minor resistance will dampen the bearish case and turn bias back to the upside for 1.1691 resistance.

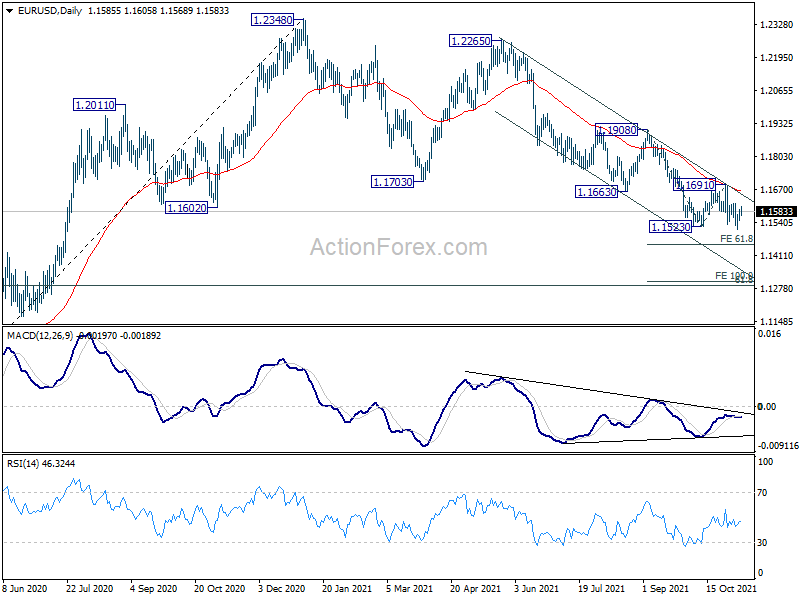

In the bigger picture, price actions from 1.2348 should at least be a correction to rise from 1.0635 (2020 low). As long as 1.1908 resistance holds, deeper fall would be seen to 61.8% retracement of 1.0635 to 1.2348 at 1.1289. Nevertheless break of 1.1908 resistance will revive medium term bullishness and turn focus back to 1.2348 high.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | Labor Cash Earnings Y/Y Sep | 0.20% | 0.60% | 0.70% | 0.60% |

| 23:50 | JPY | Bank Lending Y/Y Oct | 0.90% | 0.70% | 0.60% | |

| 23:50 | JPY | Current Account (JPY) Sep | 0.76T | 0.85T | 1.04T | 0.88T |

| 00:01 | GBP | BRC Like-For-Like Retail Sales Y/Y Oct | -0.20% | -0.60% | ||

| 00:30 | AUD | NAB Business Confidence Oct | 21 | 13 | 10 | |

| 00:30 | AUD | NAB Business Conditions Oct | 11 | 5 | ||

| 07:00 | EUR | Germany Trade Balance (EUR) Sep | 13.2B | 14.2B | 13.0B | |

| 07:45 | EUR | France Trade Balance (EUR) Sep | -6.8B | -7.0B | -6.7B | |

| 10:00 | EUR | Germany ZEW Economic Sentiment Nov | 31.7 | 20.3 | 22.3 | |

| 10:00 | EUR | Germany ZEW Current Situation Nov | 12.5 | 19.4 | 21.6 | |

| 10:00 | EUR | Eurozone ZEW Economic Sentiment Nov | 25.9 | 20.6 | 21 | |

| 11:00 | USD | NFIB Business Optimism Index Oct | 98.2 | 98.6 | 99.1 | |

| 13:30 | USD | PPI M/M Oct | 0.60% | 0.50% | 0.50% | |

| 13:30 | USD | PPI Y/Y Oct | 8.60% | 8.70% | 8.60% | |

| 13:30 | USD | PPI Core M/M Oct | 0.40% | 0.50% | 0.20% | |

| 13:30 | USD | PPI Core Y/Y Oct | 6.80% | 6.80% | 6.80% |

{kind=link}