Dollar’s rally extends in Asian session, with EUR/USD breaching 1.13 key support zone. Meanwhile, USD/JPY also breaks 114.86 near term top. Sterling is so far very resilient as markets await inflation data from the UK. Canadian Dollar is just mixed ahead of Canada CPI. Much volatility is likely in the day ahead. In other markets, Gold is back at around 1850 after failing rally attempt. WTI crude oil continues to defend 80 handle.

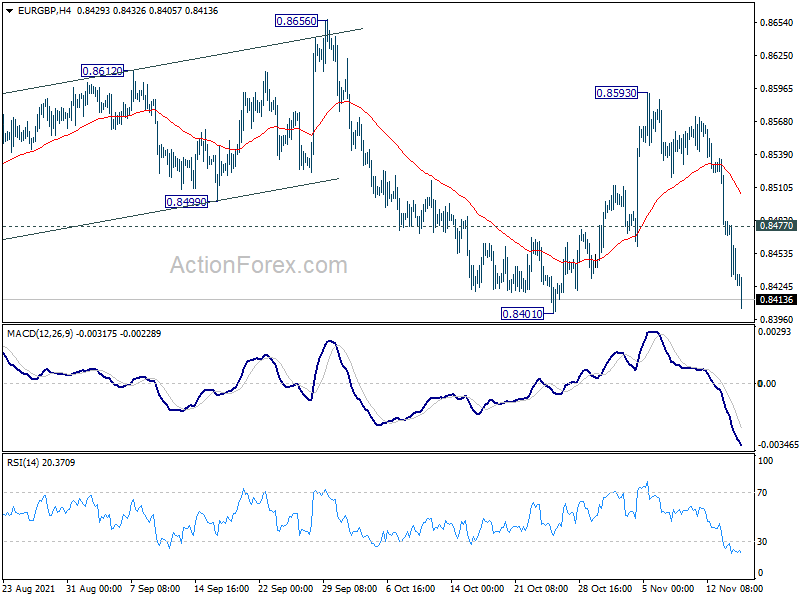

Technically, EUR/GBP is also a pair to watch ahead. Firm break of 0.8401 will resume medium term down trend towards key long term support level at 0.8276. Euro’s broad based selloff could further intensify with such development. However, rebound from current level, followed by break of 0.8477 minor resistance will indicate temporary easing of selling pressure, which might be accompanied by recovery in EUR/USD and EUR/CHF.

In Asia, at the time of writing, Nikkei is down -0.30%. Hong Kong HSI is down -0.26%. China Shanghai SSE is up 0.29%. Singapore Strait Times is down -0.30%. Japan 10-year JGB yield is down -0.0010 at 0.075. Overnight, DOW rose 0.15%. S&P 500 rose 0.39%. NASDAQ rose 0.76%. 10-year yield rose 0.011 to 1.634.

BoC Schembri: Rate to stay at ELB until excess capacity is absorbed

BoC Deputy Governor Lawrence Schembri said yesterday, “Our assessment of labour market conditions and underlying capacity and inflationary pressures is now more difficult. Consequently, more uncertainty exists around the timing of when the output gap will close and inflation will return sustainably to our 2-per-cent target.”

“We’ll keep the policy rate at the effective lower bound [0.25%] until excess capacity is absorbed … that excess capacity includes all the groups of employees that aren’t fully employed at this juncture,” Schembri said in response to a question after the speech.

“Now of course, one has to take into account that there’s going to be some natural friction in the labour market, people are going to move between jobs, so we’re not saying that there has to be zero unemployment,” he added.

Fed Daly: Ready to act as we get clearer signal

San Francisco Fed Bank President Mary Daly urged patience in assess the economic development before acting on interest rates. “Reacting in response to things that aren’t likely to last will move us farther from — not closer to — our goals,” she said.

“Over the next several quarters, as tapering occurs, we will watch how the economy does and see whether inflation eases and workers come back.”

“As we get a clearer signal, we will be ready to act accordingly, continuing to provide or remove support as needed to ensure the economy settles at a sustainable place.”

Japan exports growth slowed to 9.4% yoy on fall in car shipments

Japan exports rose 9.4% yoy to JPY 7.18B in October. That was the slowest expansion since a decline in February. By region, exports to China rose 9.5% yoy, slowed from 10.3% yoy in the prior month, on -46.8% yoy fall in car shipments. Exports to US grew just 0.4% yoy, also weighed down by -46.4% yoy fall in car exports. Imports rose 26.7% yoy to JPY 7.25B. Trade balance came at as JPY -0.07B deficit

In seasonally adjusted terms exports rose 2.7% mom to JPY 6.93B while imports rose 0.3% mom to JPY 7.38B. Trade deficit came in at JPY -0.44B.

Also from Japan, machine orders rose 0.0% mom in September, versus expectation of 1.8% mom.

Australia wage price index rose 0.6% qoq in Q3

Australia wage price index rose 0.6% qoq 2.2% yoy in Q3. Private sector rose 0.6% qoq, 2.4% yoy. Public sector rose 0.5% qoq, 1.7% yoy. The three largest states were the main contributors to growth, New South Wales, Victoria, and Queensland. The most significant industries to contribute to growth this quarter were the Professional, scientific and technical services, Health care and social assistance and Construction industries.

Westpac leading index rose 0.20% mom in October.

From New Zealand, PPI input rose 1.6% qoq in Q3, versus expectation of 1.7% qoq. PPI output rose 1.8% qoq, versus expectation of 1.4% qoq.

Looking ahead

UK CPI and PPI will be the main focus in European session. Eurozone will release CPI final too. Later in the day, Canada CPI will take center stage. US will release building permits and housing starts.

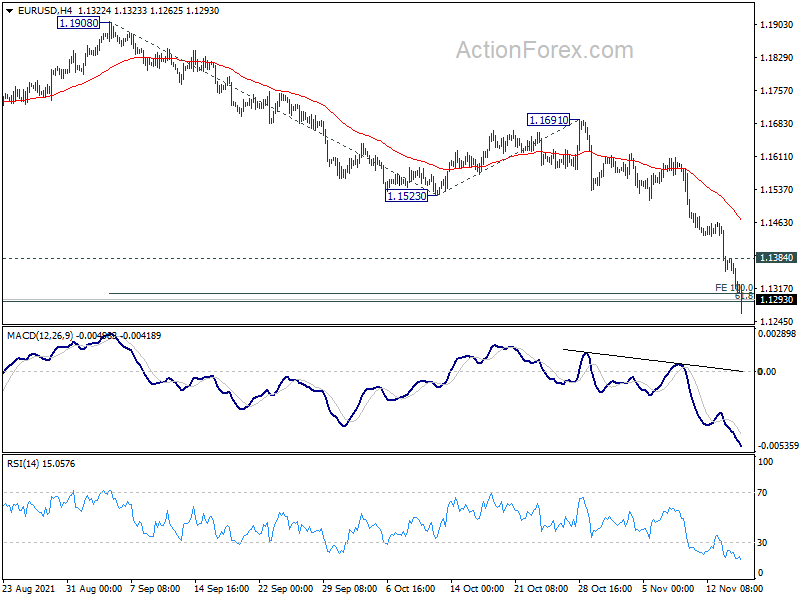

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1290; (P) 1.1338; (R1) 1.1366; More…

EUR/USD’s fall accelerates to as low as 1.1262 so far today and intraday bias stays on the downside. Sustained break of 1.1289 long term fibonacci level will carry larger bearish implication. Next target will be 161.8% projection of 1.1908 to 1.1523 from 1.1691 at 1.1068. On the upside, above 1.1384 minor resistance will turn intraday bias neutral first. But outlook will remain bearish as long as 1.1523 support turned resistance holds.

In the bigger picture, there are various ways of interpreting the fall from 1.2348 (2021 high). It could be a correction to rise from 1.0635 (2020 low), the fourth leg of a sideway pattern from 1.0339 (2017 low), or resuming long term down trend. In any case, outlook will now stay bearish as long as 1.1703 support turned resistance holds. Sustained break of 61.8% retracement of 1.0635 to 1.2348 at 1.1289 would pave the way back to 1.0635.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | PPI Input Q/Q Q3 | 1.60% | 1.70% | 3.00% | |

| 21:45 | NZD | PPI Output Q/Q Q3 | 1.80% | 1.40% | 2.60% | |

| 23:30 | AUD | Westpac Leading Index M/M Oct | 0.20% | 0.00% | ||

| 23:50 | JPY | Machinery Orders M/M Sep | 0.00% | 1.80% | -2.40% | |

| 00:30 | AUD | Wage Price Index Q/Q Q3 | 0.60% | 0.50% | 0.40% | |

| 07:00 | GBP | CPI M/M Oct | 0.80% | 0.30% | ||

| 07:00 | GBP | CPI Y/Y Oct | 3.80% | 3.10% | ||

| 07:00 | GBP | Core CPI Y/Y Oct | 3.00% | 2.90% | ||

| 07:00 | GBP | RPI M/M Oct | 1.00% | 0.40% | ||

| 07:00 | GBP | RPI Y/Y Oct | 5.60% | 4.90% | ||

| 07:00 | GBP | PPI Input M/M Oct | 1.10% | 0.40% | ||

| 07:00 | GBP | PPI Input Y/Y Oct | 11.60% | 11.40% | ||

| 07:00 | GBP | PPI Output M/M Oct | 0.70% | 0.50% | ||

| 07:00 | GBP | PPI Output Y/Y Oct | 6.80% | 6.70% | ||

| 07:00 | GBP | PPI Core Output M/M Oct | 0.70% | 0.50% | ||

| 07:00 | GBP | PPI Core Output Y/Y Oct | 6.50% | 5.90% | ||

| 10:00 | EUR | Eurozone CPI Y/Y Oct F | 4.10% | 4.10% | ||

| 10:00 | EUR | Eurozone CPI Core Y/Y Oct F | 2.10% | 2.10% | ||

| 13:30 | CAD | CPI M/M Oct | 0.70% | 0.20% | ||

| 13:30 | CAD | CPI Y/Y Oct | 4.70% | 4.40% | ||

| 13:30 | CAD | CPI Common Y/Y Oct | 1.90% | 1.80% | ||

| 13:30 | CAD | CPI Median Y/Y Oct | 2.90% | 2.80% | ||

| 13:30 | CAD | CPI Trimmed Y/Y Oct | 3.40% | 3.40% | ||

| 13:30 | USD | Building Permits Oct | 63M | 1.59M | ||

| 13:30 | USD | Housing Starts Oct | 1.58M | 1.56M | ||

| 15:30 | USD | Crude Oil Inventories | 1.0M | 1.0M |

{kind=link}