Sterling dips notably after the dovish rate hike by BoE. Yen is following as second worst for the day, then Dollar. On the other hand, Aussie is leading other commodity currencies higher, support by strong job data. Euro is mixed with Swiss Franc, closely watching developments in Ukraine. In other markets, Gold is attempting a recovery but still kept well below 2000 handle. WTI crude oil is also recovering and it’s back above 100 handle.

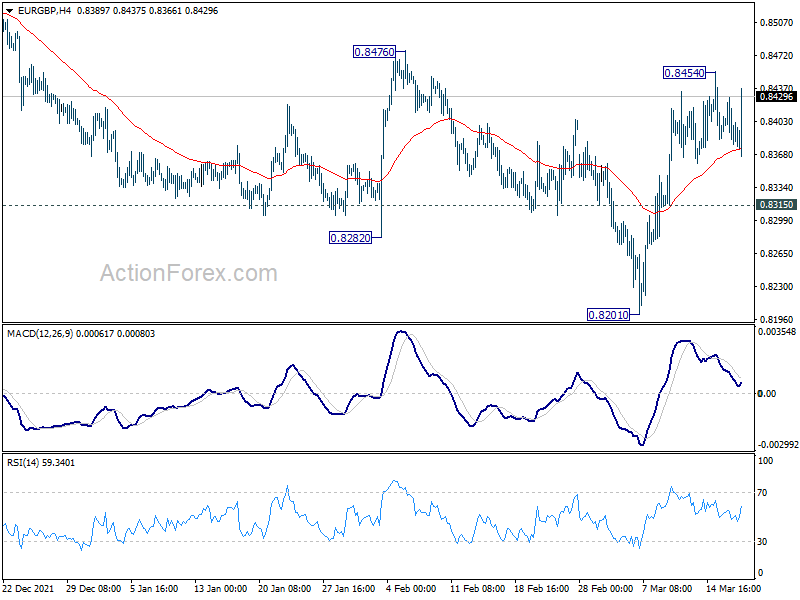

Technically, with the weakness in Euro, focus will be on EUR/GBP. Above 0.8454 temporary top will resume the rebound from 0.8201. Further break of 0.8476 resistance will be the first sign of bullish trend reversal and bring even stronger rise to 0.8598.

In Europe, at the time of writing, FTSE is up 0.44%. DAX is down -1.04%. CAC is down -0.32%. Germany 10-year yield is up 0.009 at 0.401. Earlier in Asia, Nikkei rose 3.46%. Hong Kong HSI rose 7.04%. China Shanghai SSE rose 1.40%. Singapore Strait Times rose 0.97%. Japan 10-year JGB yield dropped -0.0002 to 0.204.

US initial jobless claims dropped to 214k, continuing claims dropped to 1.419m

US initial jobless claims dropped -15k to 214k in the week ending March 12, better than expectation of 221k. Four-week moving average of initial claims dropped -9k to 223k. Continuing claims dropped -71k to 1419k in the week ending march 5, lowest since February 21, 1970. Four-week moving average of continuing claims dropped -42.5k to 1463k, lowest since March 21, 1970.

Housing starts rose to 1.77m annualized rate in February. Building permits dropped to 1.86m. Philly Fed manufacturing survey jumped from 16 to 27.4 in March.

BoE raises bank rate to 0.75%, but Cunliffe voted for no change

BoE raises Bank Rate by 25bps to 0.75% as widely expected. But surprisingly, it was done by a 8-1 vote, with Jon Cunliffe voting for no change at 0.50%. In the statement, BoE said, “some further modest tightening in monetary policy may be appropriate in the coming months, but there are risks on both sides of that judgement depending on how medium-term prospects for inflation evolve.”

“The invasion of Ukraine by Russia has led to further large increases in energy and other commodity prices,” BoE said. “Global inflationary pressures will strengthen considerably further over coming months, while growth in economies that are net energy importers, including the United Kingdom, is likely to slow.”

ECB Lagarde: Inflation to exceed 7% this year in severe scenario

ECB President Christine Lagarde said in a speech the central has given itself some “extra space” in monetary policy by stating that rate hike will come only “some time” after ending net asset purchases.

“This maintains our traditional sequencing logic, but also gives us extra space if needed after we stop purchasing bonds and before we take the next step towards normalization,” she said. “This will allow us to test whether the convergence of inflation to our target that we project today is robust to current and potential new shocks,”

Lagarde also said the outbreak of war has ” introduced new uncertainty into the outlook”, with ” the short-term factors pushing up inflation are likely to be amplified.” Inflation out hit 5.1% on average hits year, and even exceed 7% in the “severe scenario”.

ECB Knot: Normalization the appropriate response with dominant worry in inflation

ECB Governing Council member Klaas Knot said, “At this point, the dominant worry is inflation. That is why normalization of policy, the withdrawal of stimulus is the appropriate policy response.”

He expected the asset purchases to end by the end of the year. “That means September should be available (for a rate hike),” Knot said. “Not that I expect rates will have to go up in September.”

“A rate hike in the fourth quarter to me still is a realistic expectation… but by no means a certainty, he added.

Eurozone CPI finalized at 5.9% yoy in Feb, EU at 6.2% yoy

Eurozone CPI was finalized at 5.9% yoy in February, up from January’s 5.1% yoy. The highest contribution to the annual euro area inflation rate came from energy (+3.12%), followed by services (+1.04%), food, alcohol & tobacco (+0.90%) and non-energy industrial goods (+0.81%).

EU CPI was finalized at 6.2% yoy, up from January’s 5.6% yoy. The lowest annual rates were registered in Malta, France (both 4.2%), Portugal, Finland and Sweden (all 4.4%). The highest annual rates were recorded in Lithuania (14.0%), Estonia (11.6%) and Czechia (10.0%). Compared with January, annual inflation fell in two Member States and rose in twenty-five.

BoJ Kuroda: Too early to debate specifics on stimulus exit

BoJ Governor Haruhiko Kuroda told the parliament today, “it will take more time to achieve our 2% inflation target in a stable manner, so it’s too early to debate specifics on how to exit from easy policy.”

Core consumer inflation in Japan is generally expected to climb up in the months ahead, with prospect of hitting the 2% target. But Kuroda talked down the significance of such development. “I don’t think Japan is in a condition where inflation stably hits 2%, even when the impact of cellphone fee cuts taper off and energy prices rise further,” he said.

Kuroda just reiterated that BoJ will consider stimulus exit when 2% inflation is achieved. And, “in doing so, we will guide monetary policy to ensure markets including those for Japanese government bonds remain stable.”

Australia employment rose 77.4k in Feb, unemployment rate dropped to 4%

Australia employment grew 77.4k in February, nearly double of expectation of 40.0k. Full-time jobs rose 121.9k while part-time jobs dropped -44.5k. Employment was around 202k above pre-Delta high of June 2021.

Unemployment rate dropped from 4.2% to 4.0%, better than expectation of 4.1%. That’s the lowest level since August 2008. Participation rate rose 0.2% to 66.2%. Monthly hours worked rose 8.9%, or 149m, to 1813m hours.

From New Zealand, GDP grew 3.0% qoq in Q4, below expectation of 3.2% qoq.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3068; (P) 1.3112; (R1) 1.3193; More…

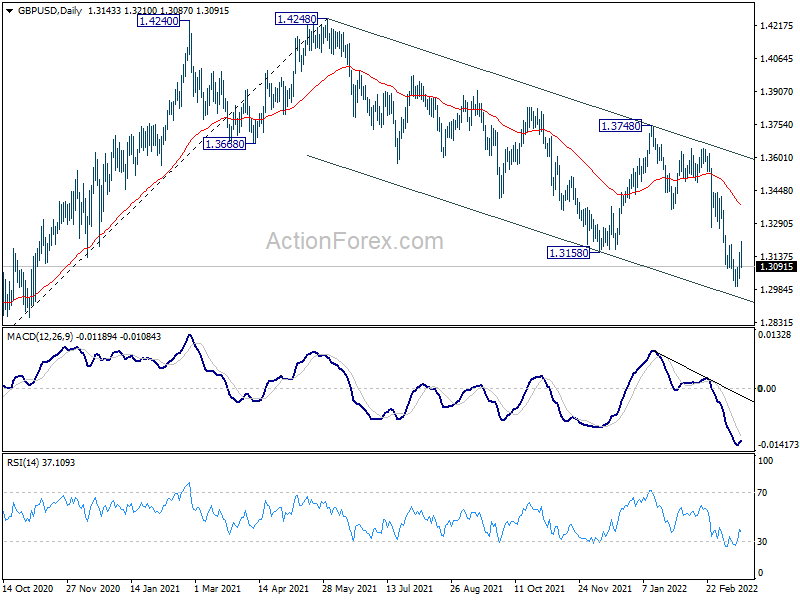

GBP/USD reversed after breaching 1.3193 resistance, but stays above 1.2999 support. Intraday bias remains neutral first and further decline is still in favor. On the downside, break of 1.2999 will resume larger down trend from 1.4248. However, on the upside, firm break of 1.3193 will confirm short term bottoming. Intraday bias will be turned back to the upside for 55 day EMA (now at 1.3374).

In the bigger picture, current development suggests that the up trend from 1.1409 (2020 low) has completed at 1.4248. Decline from 1.4248 could still be a corrective move, or it could be the start of a long term down trend. In either case, deeper decline would be seen back to 61.8% retracement of 2.1161 to 1.1409 at 1.2493. In any case, break of 1.3748 resistance is needed to indicate medium term bottoming, or outlook will stay bearish.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | GDP Q/Q Q4 | 3.00% | 3.20% | -3.70% | -3.60% |

| 23:50 | JPY | Machinery Orders M/M Jan | -2.00% | -2.20% | 3.60% | 3.10% |

| 00:30 | AUD | Employment Change Feb | 77.4K | 40.0K | 12.9K | 28.3K |

| 00:30 | AUD | Unemployment Rate Feb | 4.00% | 4.10% | 4.20% | |

| 07:00 | CHF | Trade Balance (CHF) Feb | 5.95B | 4.20B | 3.18B | 3.07B |

| 10:00 | EUR | Eurozone CPI Y/Y Feb F | 5.90% | 5.80% | 5.80% | |

| 10:00 | EUR | Eurozone CPI Core Y/Y Feb F | 2.70% | 2.70% | 2.70% | |

| 12:00 | GBP | BoE Interest Rate Decision | 0.75% | 0.75% | 0.50% | |

| 12:00 | GBP | MPC Official Bank Rate Votes | 8–0–1 | 9–0–0 | 9–0–0 | |

| 12:30 | USD | Initial Jobless Claims (Mar 11) | 214K | 221K | 227K | 229K |

| 12:30 | USD | Housing Starts Feb | 1.77M | 1.70M | 1.64M | 1.66M |

| 12:30 | USD | Building Permits Feb | 1.86M | 1.87M | 1.90M | |

| 12:30 | USD | Philadelphia Fed Manufacturing Survey Mar | 27.4 | 15 | 16 | |

| 13:15 | USD | Industrial Production M/M Feb | 0.50% | 1.40% | ||

| 14:30 | USD | Natural Gas Storage | -71B | -124B |

{kind=link}