Dollar is trading as the worst performing for the day, and receive no support from solid ADP private job data. The greenback is somewhat weighed down by extended retreat in benchmark US yields. On the other hand, Euro is supported by rising Germany benchmark yields, after consumer inflation hit the highest level in more than 40 years. Yet, Euro bulls are still not too committed to push it higher, as the hope of Russia ceasefire remains in doubt. Yen is the strongest one for today, trying to extend recovery.

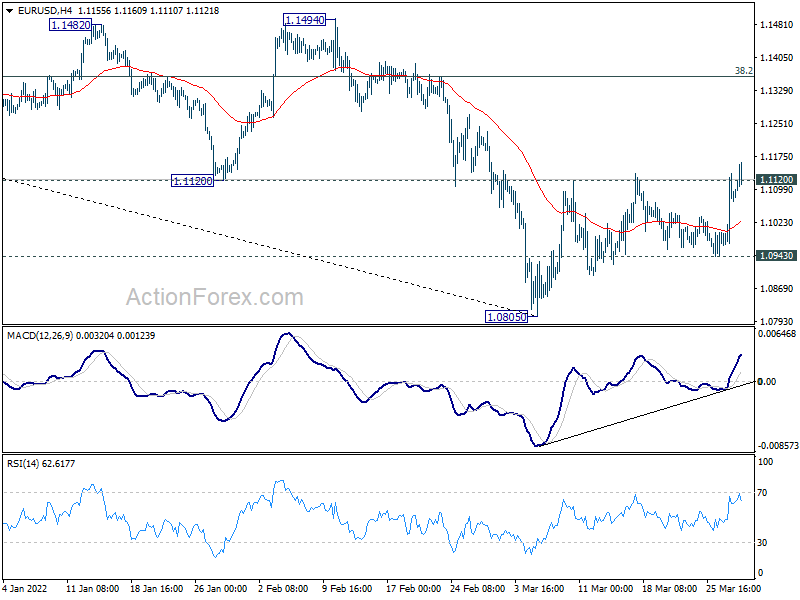

Technically, we’d reiterate that some near term resistance levels need to be take out with conviction before Euro could prove it’s underlying strength. the levels include 1.1120 support turned resistance in EUR/USD, 0.8476 structural resistance in EUR/GBP, and 1.0400 resistance in EUR/CHF. As for Dollar, it will probably need to wait until non-farm payroll report to have a chance for a come back.

In Europe, at the time of writing, FTSE is up 0.02%. DAX is down -1.64%. CAC is down -1.10%. Germany 10-year yield is up 0.051 at 0.683. Earlier in Asia, Nikkei dropped -0.80%. Hong Kong HSI rose 1.39%. China Shanghai SSE rose 1.96%. Singapore Strait Times rose 0.25%. Japan 10-year JGB yield dropped -0.0328 to 0.220.

US ADP jobs grew 455k, broad-based growth

US ADP private employment grew 455k in March, slightly above expectation of 450k. By company size, small businesses added 90k jobs, medium businesses added 188k, large businesses added 177k. By sector, goods-producing jobs grew 79k while service-providing jobs grew 377k.

“Job growth was broad-based across sectors in March, contributing to the nearly 1.5 million jobs added for the first quarter in 2022,” said Nela Richardson, chief economist, ADP. “Businesses are hiring, specifically among the service providers which had the most ground to make up due to early pandemic losses. However, a tight labor supply remains an obstacle for continued growth in consumer-facing industries.”

ECB Lagarde emphasizes principles of optionality, gradualism and flexibility

ECB President Christine Lagarde said in a speech the economic impact of Ukraine war is a “supply shock” that ” simultaneously pushes up inflation and reduces growth.” Three main favors are likely to take inflation higher, including energy, food, and manufacturing bottlenecks.

The war also posses “significant risks” to growth, implying a loss of EUR 150B in the economy in one year. The conflict also “drain confidence” through at least two channels. Firstly, households become more pessimistic and cut back on spending. Secondly, business investment is likely to be affected.

As for ECB, Lagarde said the best way to navigate this uncertainty is to emphasize the “principles of optionality, gradualism and flexibility.” Optionality means if incoming data support that medium term inflation will not weaken after the end of net asset purchases, the APP will be concluded in Q3. But ECB also stand ready to revise the schedule for net asset purchases in terms of size and/or duration. Gradualism means the adjustments to interest rate will take place “some time” after end of net purchases and will be gradual. Flexibility means ECB will use the its toolkit to ensure policy is transmitted evenly across all parts of Eurozone.

Eurozone economic sentiment dropped to 108.5, EU down to 107.5

Eurozone Economic Sentiment Indicator dropped from 113.9 to 108.5 in March. Industry confidence dropped from 14.1 to 10.4. Services confidence rose from 12.9 to 14.4. Consumer confidence dropped from -8.8 to -18.7. Retail trade confidence dropped from 5.5 to 0.2. Construction confidence ticked down from 9.9 to 9.8. Employment Expectation Indicator dropped from 116.4 to 115.5.

EU Economic Sentiment dropped from 112.8 to 107.5. Amongst the largest EU economies, the ESI fell sharply in France (-7.1), Spain (-6.5), Germany (-4.3) and, to a lesser extent, in Poland (-3.0) and Italy (-2.6), while it brightened slightly in the Netherlands (+0.5).

Swiss KOF dropped to 99.7, recovery overshadowed by war in Ukraine

Swiss KOF Economic Barometer dropped from 105 to 99.7 in March, worse than expectation of 101.0. The index is now slightly below its long-term average.

KOF said: “The recovery from the economic consequences of the pandemic is now overshadowed by the war in Ukraine. Overall, a moderate development of the Swiss economy can be expected for the near future.”

“The decline is primarily due to indicators from the manufacturing sector, followed by those for private consumption. The other indicators included in the barometer show hardly any changes.”

BoJ increases size of JGB purchases to defend yield cap

BoJ announced to increase the size of its JGB purchases to defend it’s 10-year yield cap imposed under the yield curve control.

It increased the size of purchase of JGB with maturities of 3 to 10 years today, by a combined JPY 450B to JPY 1325B. It will additionally buy JPY 150B of JGB with maturities between 10 to 25 years, and JPY 100B with maturity more than 25 years.

“The BOJ will increase the number of auction dates and the amount of outright JGB purchases as needed, taking account of market conditions,” the BOJ said in a statement.

Released from Japan, retail sales dropped -0.8% yoy in February, worse than expectation of -0.3% yoy.

New Zealand ANZ business confidence rose to -41.9, inflation expectations rose again

New Zealand ANZ business confidence rose from -51.8 to -41.9 in March. Own activity outlook rose from -2.2 to 3.3. Looking at some details, export intentions rose from 0.9 to 7.9. Investment intentions rose from 4.5 to 5.2. Employment intentions rose from 2.3 to 12.3. Pricing intentions rose from 74.1 to 80.5. Cost expectations rose from 92.0 to 95.9. Inflation expectations rose back from 5.29 to 5.51.

ANZ said: “With inflation pressures now so extreme, and the RBNZ’s inflation-targeting credibility on the line, it’s full steam ahead for rate hikes – we’re forecasting 50bp hikes in both April and May.

“It could well be a rough ride, but maintaining medium-term price stability is the best contribution monetary policy can make to New Zealand’s big-picture economic prospects from this very difficult starting point.”

Also from New Zealand, building permits rose 10.5% mom in February.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0992; (P) 1.1064 (R1) 1.1159; More…

Intraday bias in EUR/USD is mildly on the with focus on 1.1120 support turned resistance. Sustained break there will argue that it’s at least correcting the decline from 1.2265. Further rally should then be seen to 38.2% retracement of 1.2265 to 1.0805 at 1.1363. On the downside, however, break of 1.0943 support will revive near term bearishness, and bring retest of 1.0805 low.

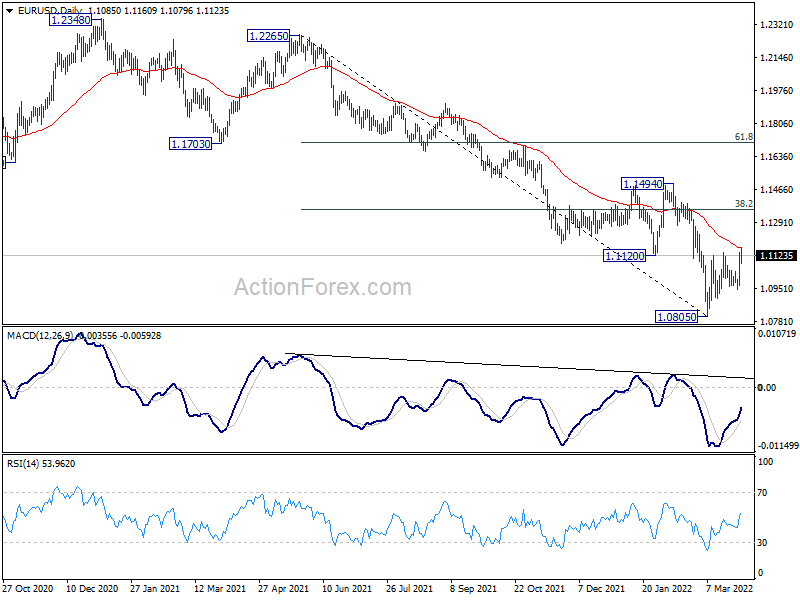

In the bigger picture, the decline from 1.2348 (2021 high) is expected to continue as long as 1.1494 resistance holds. Firm break of 1.0635 (2020 low) will raise the chance of long term down trend resumption and target a retest on 1.0339 (2017 low) next. Nevertheless, break of 1.1494 will maintain medium term neutral outlook, and extending term range trading first.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | Building Permits M/M Feb | 10.50% | -9.20% | -8.70% | |

| 23:01 | GBP | BRC Shop Price Index Y/Y Feb | 2.10% | 1.80% | ||

| 23:50 | JPY | Retail Trade Y/Y Feb | -0.80% | -0.30% | 1.10% | |

| 00:00 | NZD | ANZ Business Confidence Mar | -41.9 | -51.8 | ||

| 07:00 | CHF | KOF Leading Indicator Mar | 99.7 | 101 | 105 | 105.3 |

| 08:00 | CHF | Credit Suisse Economic Expectations Mar | -27.8 | 9 | ||

| 09:00 | EUR | Eurozone Economic Sentiment Indicator Mar | 108.5 | 110 | 114 | 113.9 |

| 09:00 | EUR | Eurozone Industrial Confidence Mar | 10.4 | 8.9 | 14 | 14.1 |

| 09:00 | EUR | Eurozone Services Sentiment Mar | 14.4 | 10 | 13 | 12.9 |

| 09:00 | EUR | Eurozone Consumer Confidence Mar F | -18.7 | -18.7 | -18.7 | |

| 12:00 | EUR | Germany CPI M/M Mar P | 2.50% | 1.60% | 0.90% | |

| 12:00 | EUR | Germany CPI Y/Y Mar P | 7.30% | 6.10% | 5.10% | |

| 12:15 | USD | ADP Employment Change Mar | 455K | 450K | 475K | 486K |

| 12:30 | USD | GDP Annualized Q4 F | 6.90% | 7.10% | 7.00% | |

| 12:30 | USD | GDP Price Index Q4 F | 7.10% | 7.10% | 7.10% | |

| 14:30 | USD | Crude Oil Inventories | -2.0M | -2.5M |

{kind=link}