Dollar is turning softer entering into US session, as traders might start to lighten up position ahead tomorrow’s FOMC rate decision. Commodity currencies are also soft, except Aussie which is supported by RBA’s hawkish rate hike. Yet, there is no clear follow through buying in Aussie. European majors, on the other hand, are trying to rebound.

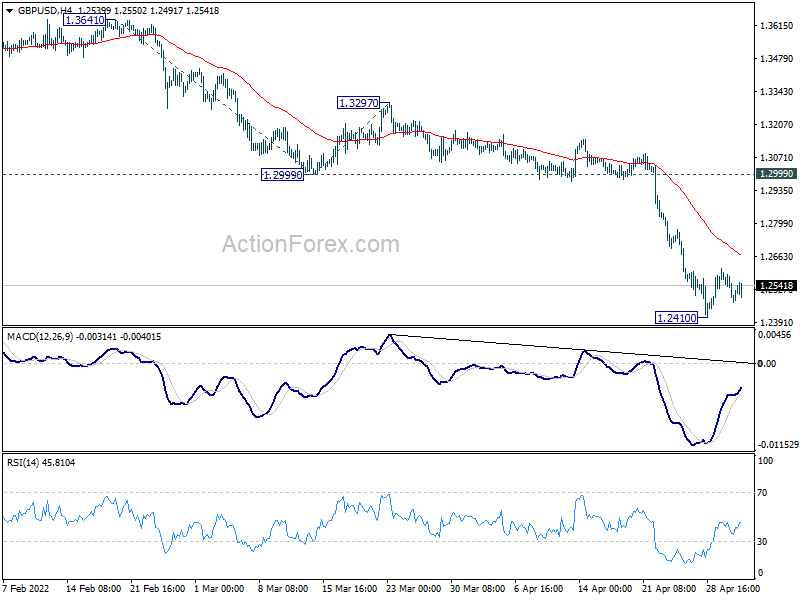

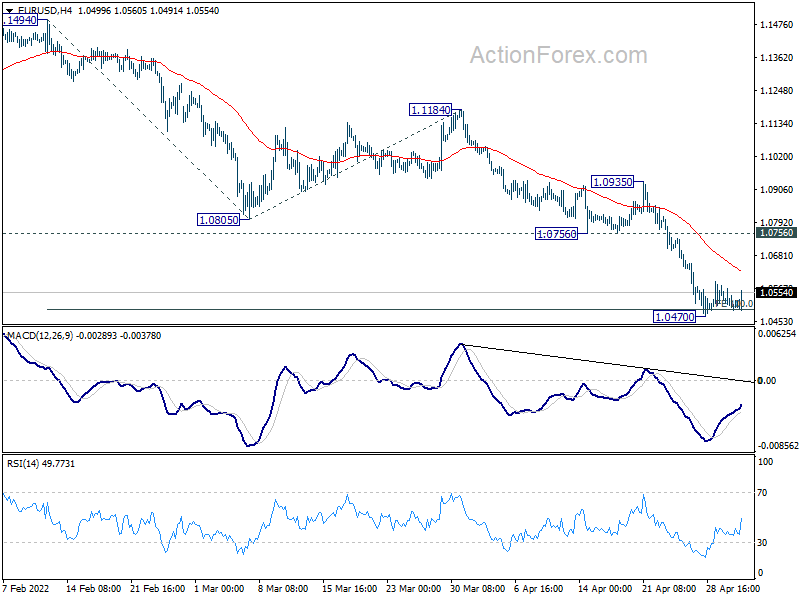

Technically, some focuses will be on whether European majors build on current recovery to develop more sustainable rebound. The levels to watch include 4 hours 55 EMA in EUR/USD at 1.0626, 4 hours 55 EMA in GBP/USD at 1.2667, and 4 hours 55 EMA in USD/CHF at 0.9646. Without breaking these level, the rebound in European majors wouldn’t last long.

In Europe, at the time of writing, FTSE is down -0.48%. DAX is up 0.33%. CAC is up 0.41%. Germany 10-year yield is down -0.028 at 0.942. Earlier in Asia, Hong Kong HSI rose 0.06%. Singapore Strait Times rose 0.65%. Japan and China were on holiday.

Eurozone PPI rose 5.3% mom, 36.8% yoy in Mar

Eurozone PPI rose 5.3% mom, 36.8% yoy in March, above expectation of 4.9% mom, 36.3% yoy. For the month, industrial producer prices increased by 11.1% in the energy sector, by 2.8% for intermediate goods, by 2.4% for non-durable consumer goods and by 0.8% for capital goods and durable consumer goods. Prices in total industry excluding energy increased by 2.1%.

EU PPI rose 4.% mom, 36.5% yoy. The highest monthly increases in industrial producer prices were recorded in Ireland (+36.1%), Greece (+8.8%) and Portugal (+8.4%). The only decrease was observed in Slovakia (-1.1%) while in Malta the industrial producer prices remained unchanged.

Eurozone unemployment rate dropped to 6.8% in Mar, EU dropped to 6.2%

Eurozone unemployment rate dropped from 6.9% to 6.8% in March, matched expectations. EU unemployment rate dropped from 6.3% to 6.2%.

Eurostat estimates that 13.374m men and women in EU, of whom 11.274m in Eurozone, were unemployed. Compared with February, the number of persons unemployed decreased by -85k in EU and by -76k in Eurozone.

UK PMI manufacturing finalized at 55.8, failed to mask the continued headwinds

UK PMI Manufacturing was finalized at 55.8 in April, up slightly from march’s 55.2. S&P Global said production growth improved slightly. New orders rose at slower pace as new export business retreated. Selling prices rose at record pace as cost inflation accelerated.

Rob Dobson, Director at S&P Global, said: “The improved expansion of output at manufacturers, while positive in itself, failed to mask the continued headwinds buffeting the sector… Manufacturers and their clients are struggling as lockdowns in China and the Ukraine war exacerbate stretched global supply chains, the inflationary picture worsens and geopolitical tensions rise. Specific to the UK, Brexit represents an additional headwind…

“Business optimism has fallen to a 16-month low as companies become more cautious about the future outlook… The inflationary situation is getting increasingly fraught. Input costs rose to the second-greatest extent in the 30-year survey history, leading to a record increase in factory gate selling prices.”

RBA hikes by 25bps to 0.35%, more to come

RBA raises cash rate target by 25bps to 0.35% today, larger than expectation of 15bps to 0.25%. The interest rate on Exchange Settlement balances is also lifted by 25bps to 0.25%. In the forward guidance, RBA said it’s committed to “ensure that inflation in Australia returns to target over time”. That will “require a further lift in interest rates over the period ahead”.

In the accompanying statement, RBA said the economy has “proven to be resilient and inflation has picked up more quickly, and to a higher level, than was expected” while “wages growth is picking up”. It’s appropriate to start the process of normalizing monetary conditions.”

Unemployment rate is expected to decline to around 3.5% by early 2023, hitting the lowest level in almost 50 years. GDP is projected to grow by 4.25% over 2022 and 2% over 2023. Headline expected to rise further from current 5.1% to 5% this year. Underlying inflation is also expected to rise from current 3.7% to 4.75%. By mid-2024, headlines and underlying inflation are projected to have moderated back to around 3%, with assumption of further rate hikes.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0476; (P) 1.0523 (R1) 1.0555; More…

EUR/USD recovers mildly as consolidation from 1.0470 extends. But intraday bias remains neutral for the moment. Upside of recovery should be limited by 1.0756 support turned resistance to bring fall resumption. Break of 1.0470 will resume larger down trend and target 161.8% projection of 1.1494 to 1.0805 from 1.1184 at 1.0069.

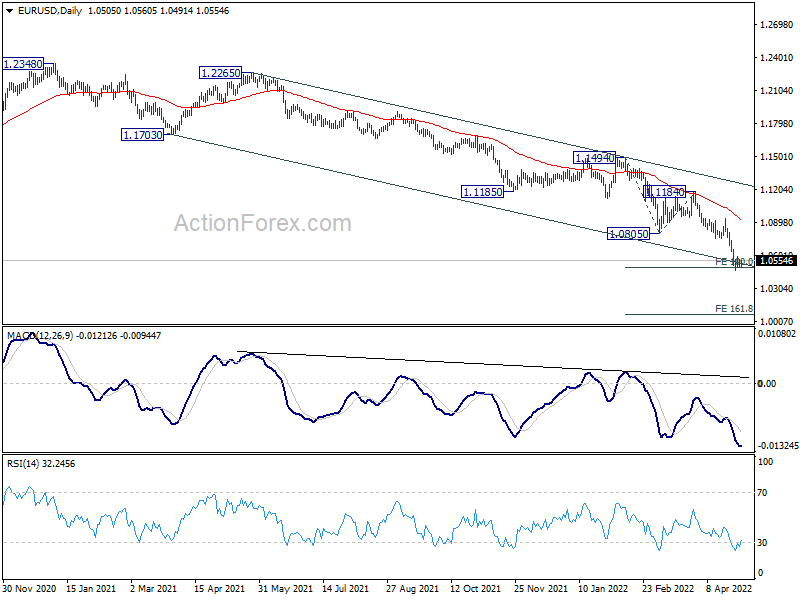

In the bigger picture, the decline from 1.2348 (2021 high) is expected to continue as long as 1.1185 support turned resistance holds. The break of 1.0635 (2020 low) now raises the chance that it’s resuming long term down trend from 1.6039 (2008 high). Retest of 1.0339 (2017 low) low should be seen next. Decisive break there will confirm this bearish case.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Building Permits M/M Mar | 5.80% | 10.50% | 12.20% | |

| 04:30 | AUD | RBA Interest Rate Decision | 0.35% | 0.25% | 0.10% | |

| 07:55 | EUR | Germany Unemployment Change Apr | -13K | -15K | -18K | |

| 07:55 | EUR | Germany Unemployment Rate Apr | 5.00% | 5.00% | 5.00% | |

| 08:30 | GBP | Manufacturing PMI Apr F | 55.8 | 55.3 | 55.3 | |

| 09:00 | EUR | Eurozone Unemployment Rate Mar | 6.80% | 6.80% | 6.80% | 6.90% |

| 09:00 | EUR | Eurozone PPI M/M Mar | 5.30% | 4.90% | 1.10% | |

| 09:00 | EUR | Eurozone PPI Y/Y Mar | 36.80% | 36.30% | 31.40% | 31.50% |

| 14:00 | USD | Factory Orders M/M Mar | 1.20% | -0.50% |

{kind=link}