Overall risk sentiment is stable in Asian session today. Australian and New Zealand Dollar are trading mildly higher as recoveries extend, while Sterling is also slightly higher. On the other hand, Yen is softening together with Swiss Franc and Dollar, and that is in-line with risk trades. Euro and Canadian Dollar are mixed for now.

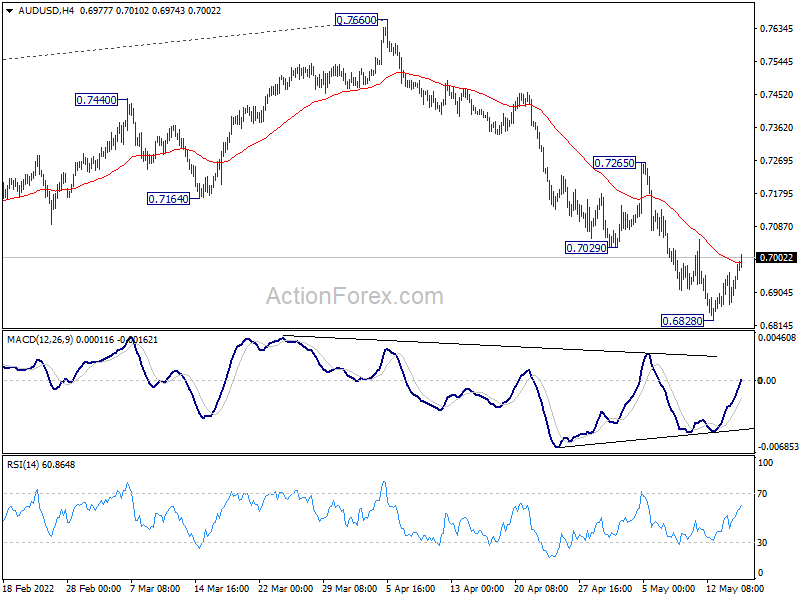

Technically, there are some early signs of turn around in overall risk sentiment. Hence, some focuses will be on commodity currencies today. EUR/AUD’s break of 1.4961 minor support raises the chance that corrective rise from 1.4318 has already completed with three waves up to 1.5277. Underlying strength of Aussie would be further affirmed if AUD/USD could break through 0.7029 support turned resistance. But of course, the fall in EUR/AUD could be accompanied by breakdown in EUR/USD through 1.0339 low, which signal Euro’s weakness instead. Let’s see.

In Asia, at the time of writing, Nikkei is up 0.28%. Hong Kong HSI is up 2.23%. China Shanghai SSE is up 0.29%. Singapore Strait Times is up 0.39%. Japan 10-year JGB yield is up 0.0024 at 0.246. Overnight, DOW rose 0.08%. S&P 500 dropped -0.39%. NASDAQ dropped -1.20%. 10-year yield dropped -0.058 to 2.877.

RBA considered 15bps, 25bps, 40bps hikes in May

In the minutes of May 3 meeting, RBA revealed that three options on interest rate hikes were considered, including 15bps, 25bps and 40bps.

Raising the cash rate by 15bps was not preferred “given that policy was very stimulatory and that it was highly probable that further rate rises would be required.” And argument for 40bps “could be made given the upside risks to inflation and the current very low level of interest rates”.

But the preferred option of was 25bps, as “a move of this size would help signal that the Board was now returning to normal operating procedures after the extraordinary period of the pandemic”.

BoE Bailey: There were range of views on both sides of the narrow path we are navigating

At the report to the Treasury Committee, BoE Governor Andrew Bailey reiterated that most MPC members judge that “some degree of further tightening in monetary policy might still be appropriate in the coming months”.

But he also acknowledged there are “risks on both sides of that judgement”, and a “range of views among these members on the balance of risks”. “This reflects the narrow path we are navigating, given the magnitude of the risks on both sides of our inflation projections,” he added.

Reflecting risks on one side of that “narrow path”, three MPC members voted for 50bps hike in May, instead of 25bps.

Reflecting risks on the other side, there were also a “range of views about the need for, and extent of, any further tightening in policy in the coming months”. Some members judged that “the risks around activity and inflation over the policy horizon were more evenly balanced and that such guidance was not appropriate at this juncture.

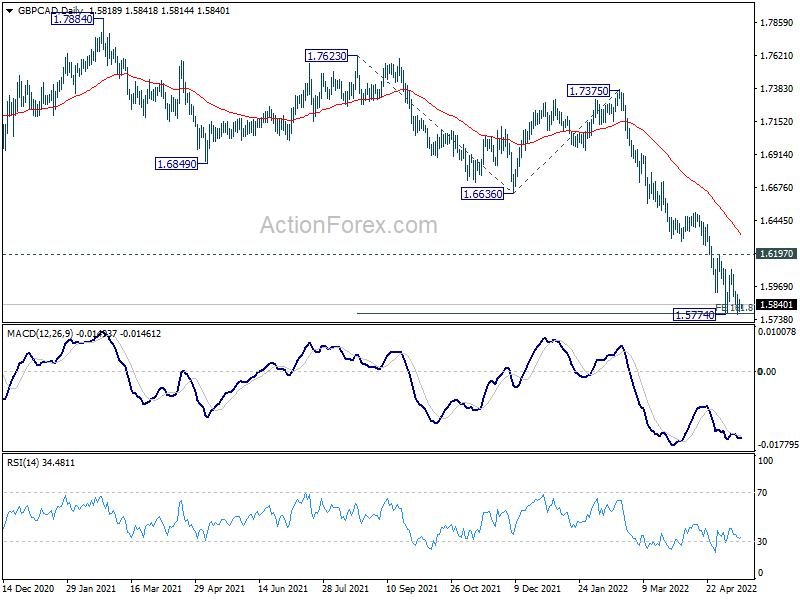

GBP/CAD holding above 2016 low, awaiting wave of UK data

Sterling is a major focus this week with a batch of economic data featured, starting from jobs today, to inflation and retail sales. Risks to the inflation outlook are on both sides as BoE Governor Andrew Bailey explained. Thus, the path of monetary policy, as well as the Pound’s movements, are also highly uncertain.

GBP/CAD’s decline slowed after falling to 1.5774 earlier in the month, hitting 161.8% projection of 1.7623 to 1.6636 from 1.7375 at 1.5778. More importantly, it’s now close to long term support at 1.5746 (2016 low). Further decline will remain in favor as long as 1.6197 resistance holds. Break of 1.5774 could easily push GBP/CAD through 1.5746 to resume the down trend from 2.0971 (2015 high). Such development will also raise the chance of resuming larger down trend from 2.5471 (2002 high) through 1.4831 (2010 low) in the medium term. It could be rather significant.

Looking ahead

UK employment, Italy trade balance, Eurozone GDP will be released in European session. Later in the day, US will release retail sales, industrial production, business inventories and NAHB housing index.

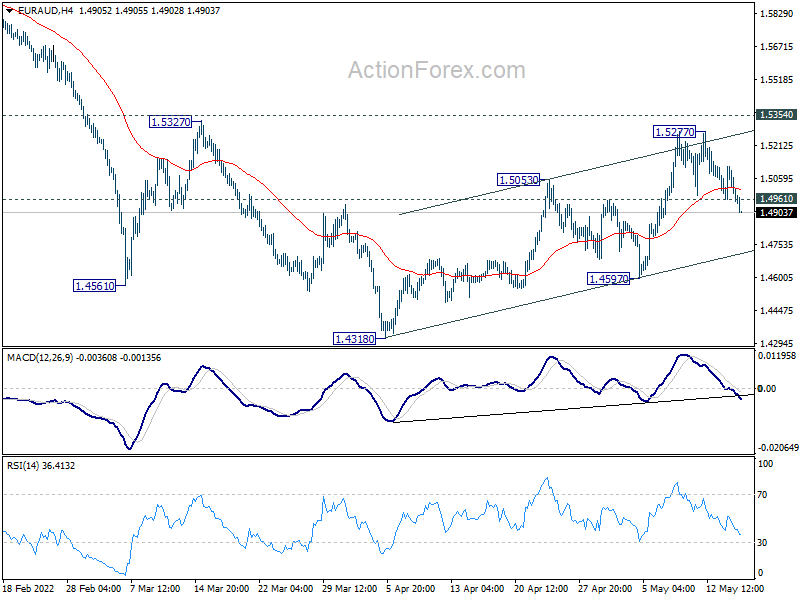

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.4910; (P) 1.5014; (R1) 1.5075; More…

EUR/AUD’s break of 1.4961 minor support suggest that corrective rise from 1.4318 has completed with three waves up to 1.5277. Rejection by 1.5354 support turned resistance retains near term bearishness. Intraday bias is back on the downside for 1.4597 support first. Break there will bring retest of 1.4318 low.

In the bigger picture, as long as 1.5354 support turned resistance holds, larger down trend form 1.9799 (2020 high) is still expected to continue. On resumption, next target is 61.8% projection of 1.9799 to 1.5250 from 1.6434 at 1.3623, which is close to 1.3624 long term support (2017 low). However, firm break of 1.5354 will indicate medium term bottoming and bring stronger rally back to 1.6434 key resistance.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 01:30 | AUD | RBA Meeting Minutes | ||||

| 04:30 | JPY | Tertiary Industry Index M/M Mar | 1.30% | 1.20% | -1.30% | |

| 06:00 | GBP | Claimant Count Change Apr | -42.3K | -46.9K | ||

| 06:00 | GBP | ILO Unemployment Rate (3M) Mar | 3.80% | 3.80% | ||

| 06:00 | GBP | Average Earnings Including Bonus 3M/Y Mar | 5.40% | 5.40% | ||

| 06:00 | GBP | Average Earnings Excluding Bonus 3M/Y Mar | 4.20% | 4.00% | ||

| 08:00 | EUR | Italy Trade Balance (EUR) Mar | 0.79B | -1.66B | ||

| 09:00 | EUR | Eurozone GDP Q/Q Q1 P | 0.20% | 0.20% | ||

| 09:00 | EUR | Eurozone Employment Change Q/Q Q1 P | 0.50% | 0.50% | ||

| 12:30 | USD | Retail Sales M/M Apr | 1.10% | 0.50% | ||

| 12:30 | USD | Retail Sales ex Autos M/M Apr | 0.30% | 1.10% | ||

| 13:15 | USD | Industrial Production M/M Apr | 0.40% | 0.90% | ||

| 13:15 | USD | Capacity Utilization Apr | 78.60% | 78.30% | ||

| 14:00 | USD | Business Inventories Mar | 1.80% | 1.50% | ||

| 14:00 | USD | NAHB Housing Market Index May | 76 | 77 |

{kind=link}