Markets are generally steady in Asian session today. European majors are firming up slightly but there is no clear follow through buying so far. On the other hand, Yen is losing ground while commodity currencies are also soft. Dollar is mixed in the middle. Focuses are back to economic data this week, with particular attention on inflation data from the US, as well as a wave of data from the UK.

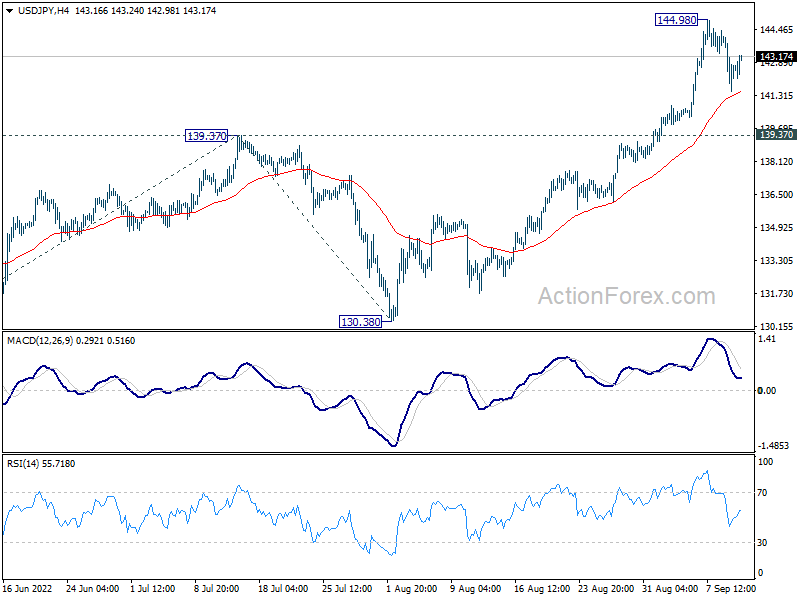

Technically, Yen might be ready to resume recent down trend. Break of 144.71 resistance in EUR/JPY will confirm resumption of recent rally. That could lead other Yen crosses higher. Corresponding break of 144.98 temporary top in USD/JPY would confirm the overall underlying momentum.

In Asia, at the time of writing, Nikkei is up 1.02%. Japan 10-year JGB yield is down -0.0002 at 0.251. Singapore Strait Times is up 0.33%. China and Hong Kong are on holiday.

Bundesbank Nagel: Further clear steps must follow if inflation stays the same

Bundesbank President Joachim Nagel said in a radio interview on Sunday that last week’s 75bps hike was a “clear sign and if the inflation picture stays the same, further clear steps must follow.”

He added that inflation may peak at more than 10% in December. “In the course of 2023, the inflation picture is likely to weaken somewhat,” he said. Still, the rate “is likely to be at a far-too-high level of over 6%.”

While there “currently are some indications that the economy could stagnate or even contract in the second half of 2022 and that this trend could continue into next year, any recession may be shallow,” Nagel added.

“In the end, stable prices are much more important for medium-term, long-term growth, for a good outlook for the euro area,” he said. “We may need to overcome a dry spell, but for now at least it looks like this dry spell and the decline in economic output will not be severe.”

ECB Elderson: Very important that inflation expectations not become unanchored

ECB Executive Board member Frank Elderson told Dutch television, “it’s very important that the expectations that the people have on how the inflation will develop in the medium to long term will not become unanchored.”

“It is vital that people and companies or actors in the economy in general maintain their trust that we as the ECB will reach our of target of 2 per cent inflation,” Elderson said.

Economic data from US and UK to rock the markets

Attention is back to economic data this week. CPI from US will be a major focus, along with retail sales. A wave of data from the UK will also be published including GDP, production, CPI, employment and retail sales. These data will provide much food for thoughts for Fed and BoE before their meeting next week, and could rock the markets.

Other data to be watched include Germany ZEW economic sentiment; Australia employment and business confidence, as well as China industrial production, retail sales and fixed asset investment.

Here are some highlights for the week:

- Monday: UK GDP, production, trade balance.

- Tuesday: Japan BSI manufacturing, PPI; Australia NAB business confidence; Germany CPI final, ZEW economic sentiment; UK employment; Swiss PPI; US CPI.

- Wednesday: New Zealand current account; Japan machine orders; UK CPI, PPI; Eurozone industrial production; Canada manufacturing sales; US PPI.

- Thursday: New Zealand GDP; Japan trade balance, tertiary industry index; Australia employment; Eurozone trade balance; US retail sales, Empire state manufacturing, Philly Fed manufacturing, jobless claims, import prices, industrial production, business inventories.

- Friday: New Zealand BusinessNZ manufacturing index; China industrial production, retail sales, fixed asset investment; UK retail sales; Italy trade balance; Eurozone CPI final; Canada housing starts, wholesale sales; US U of Michigan consumer sentiment.

USD/JPY Daily Outlook

Daily Pivots: (S1) 141.34; (P) 142.73; (R1) 143.96; More…

USD/JPY recovers mildly today but stays in range below 144.98. Intraday bias remains neutral and more consolidations could be seen. Downside of retreat should be contained by 139.37 resistance turned support. On the upside, break of 144.98 will resume larger up trend to 147.68 long term resistance. Break there will target 161.8% projection of 126.35 to 139.37 from 130.38 at 151.44 next.

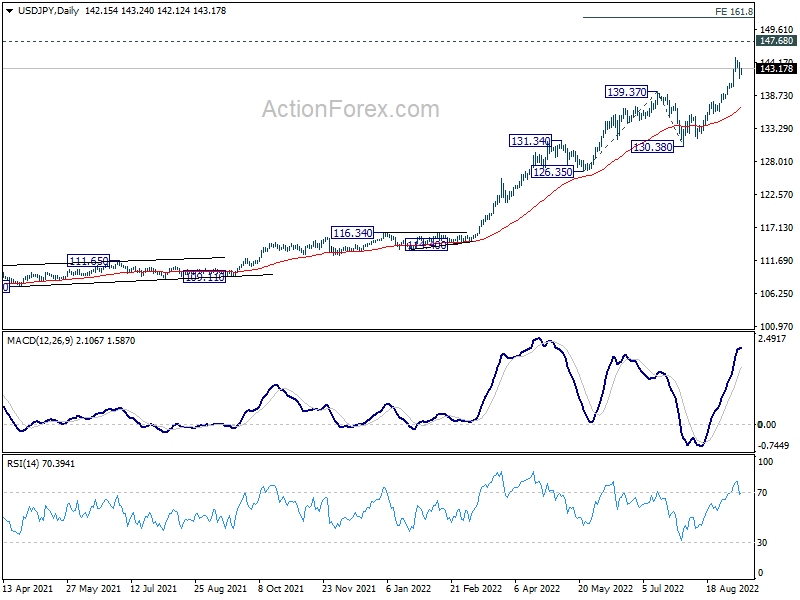

In the bigger picture, up trend from 101.18 is still in progress, as part of the whole up trend from 75.56 (2011 low). Further rise should be seen to 147.68 (1998 high). For now, break of 130.38 support is needed to be the first indication of medium term topping. Otherwise, outlook will stay bullish even in case of deep pull back.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 06:00 | JPY | Machine Tool Orders Y/Y Aug | 5.50% | |||

| 06:00 | GBP | GDP M/M Jul | 0.30% | -0.60% | ||

| 06:00 | GBP | Industrial Production M/M Jul | 0.40% | -0.90% | ||

| 06:00 | GBP | Industrial Production Y/Y Jul | 2.00% | 2.40% | ||

| 06:00 | GBP | Manufacturing Production M/M Jul | 0.60% | -1.60% | ||

| 06:00 | GBP | Manufacturing Production Y/Y Jul | 1.70% | 1.30% | ||

| 06:00 | GBP | Index of Services 3M/3M Jul | -0.80% | -0.40% | ||

| 06:00 | GBP | Goods Trade Balance (GBP) Jul | -23.2B | -22.8B | ||

| 08:00 | EUR | Italy Industrial Output M/M Jul | 0.00% | -2.10% | ||

| 13:00 | GBP | NIESR GDP Estimate Aug | 0.00% |

{kind=link}