Dollar surges further in early US session against Yen, after BoJ Governor Haruhiko Kuroda dropped no hint on intervention despite today’s Yen selloff. Indeed, he noted that Yen depreciation could be could for the economy as a whole, just that speculation driven move is bad. But the greenback is actually struggling to gain against other major currencies. FOMC minutes will be featured later today but they’re unlikely to reveal anything new. Traders will be keenly awaiting tomorrow’s US CPI release.

Technically, one focus for now is whether USD/JPY’s rally could taken other Yen crosses higher, especially EUR/JPY and GBP/JPY. Both are still having 140.77 and 159.41 minor support levels in pocket. Break of 144.06 and 165.69 will resume last week’s rebound, towards 145.62 and 148.93 highs respectively.

In Europe, at the time of writing, FTSE is down -0.67%. DAX is down -0.25%. CAC is down -0.29%. Germany 10-year yield is up 0.107 at 2.410. Earlier in Asia, Nikkei dropped -0.02%. Hong Kong HSI dropped -0.78%. China Shanghai SSE rose 1.53%. Singapore Strait Times dropped -0.70%. Japan 10-year JGB yield dropped -0.007 to 0.254.

BoJ Kuroda: Yen depreciation may have good impact on economy, but speculation is bad

BoJ Governor Haruhiko Kuroda said, “yen depreciation may have a good impact on macro-economy as a whole, but there are some sectors which are suffering from weak yen.” He added that “we have to carefully watch, and analyze the impact of currency movements on the economy.”

Kuroda also qualified that “if currency movement is so fast and uni-direction, probably caused by speculation, that would be bad for the economy.”

Meanwhile, he reiterated, “we will continue our monetary easing to achieve the 2% inflation target in a stable and sustainable manner.”

US PPI up 0.4% mom, 8.5% yoy in Sep

US PPI for final demand rose 0.4% mom in September, above expectation of 0.2% mom. Two-thirds can be traced to a 0.4% mom prices for services. The index for goods rose 0.4%. Prices less food, energy, and trade services rose 0.4% mom.

For the 12 months ended in the period, PPI slowed from 8.7% yoy to 8.5% yoy. PPI ex food, energy and trade was unchanged at 5.6% yoy.

BoE Pill: A significant monetary policy response required in Nov

BoE Chief Economist Huw Pill said in a speech, “Given the uncertain world and volatile markets we face, November can seem a long time away. At present, I am still inclined to believe that a significant monetary policy response will be required to the significant macro and market news of the past few weeks.”

“But I will see when we get to November how events have evolved in the meantime. As always, my policy choices will be driven by the data and guided by pursuit of the inflation target,” he added.

UK GDP contracted -0.3% mom in Aug, driven by production

UK GDP contracted -0.3% mom in August, worst than expectation of 0.1% mom expansion. In the three months to August, compared with the three months, GDP contracted by -0.3%, with -1.5% fall in production, -0.1% fall in services and flat growth in construction.

Production fell by -1.8% mom, and was the main contributor to the decline in GDP. Growth was negative in three of the four sectors. Services dropped -0.1% mom. Construction rose 0.4% mom.

Also released, industrial production came in at -1.8% mom, -5.2% yoy, versus expectation of -0.2% mom, 0.6% yoy. Manufacturing production came in at -1.6% mom, -6.7% yoy, versus expectation of 0.0% mom, 0.7% yoy. Goods trade deficit widened to GBP -19.3B, but smaller than expectation of GBP -20.5B.

UK NIESR: Energy price guarantees to drive GDP growth higher in Q4

NIESR said the -0.3% contraction in UK GDP in August “possibly signalling the beginning of an economic recession”. Given that September PMI pointed to further decrease in the manufacturing sector, it’s likely to continue to drag on the economy in Q3.

However, it expects “the energy price guarantees for households and firms announced in September’s fiscal event to drive GDP growth higher in the fourth quarter. The extent to which the measures in the mini-budget will counter the dampening effects of plummeting confidence and increased interest rates will become clearer over the coming months.”

Eurozone industrial production up 1.5% mom in Aug, EU up 1.1% mom

Eurozone industrial production rose 1.5% mom in August, above expectation of 0.5% mom. Production of capital goods rose by 2.8% mom, durable consumer goods by 0.9% mom and non-durable consumer goods by 0.7% mom, while production of intermediate goods fell by -0.5% mom and energy by 2.1% mom.

EU industrial production rose 1.1% mom. Among Member States for which data are available, the highest monthly increases were registered in Ireland (+16.6%), Estonia (+5.0%) and Denmark (+4.3%). The largest decreases were observed in Sweden (-7.0%), Belgium (-6.1%) and the Netherlands (-1.5%).

RBA Ellis: Neutral is not a destination we necessarily reach

RBA Assistant Governor Luci Ellis said in a speech that “don’t think of this as a mechanistic approach of ‘we have to get back to neutral’, or above neutral” interest rate.

“The neutral rate is an important guide rail for thinking about the effect policy might be having. It is not necessarily a prescription for what policy should do,” he said.

“‘Neutral’, then, is not a destination we necessarily reach, but more a pole-star to guide us. And even then, its location is sufficiently uncertain that we are perhaps better served by paying more attention to the ground as it shifts beneath our feet than to that faraway pole-star,” he added.

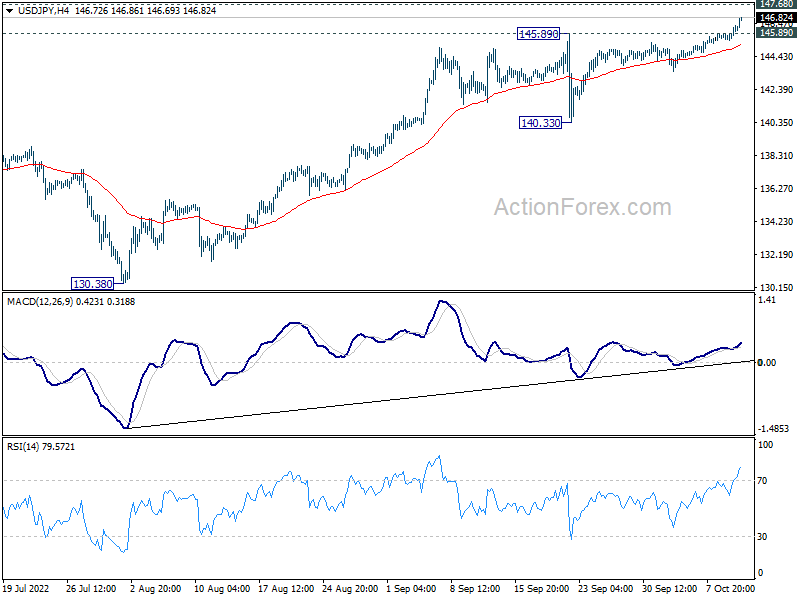

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 145.56; (P) 145.73; (R1) 146.03; More…

USD/JPY’s rally continues today and accelerates to as high as 146.81 so far. Intraday bias remains on the upside for 147.68 long term resistance. On the downside, break of 145.789 resistance turned support will turn intraday bias neutral and bring consolidations again. But overall, outlook will remain bullish as long as 140.33 support holds, even in case of deep pullback.

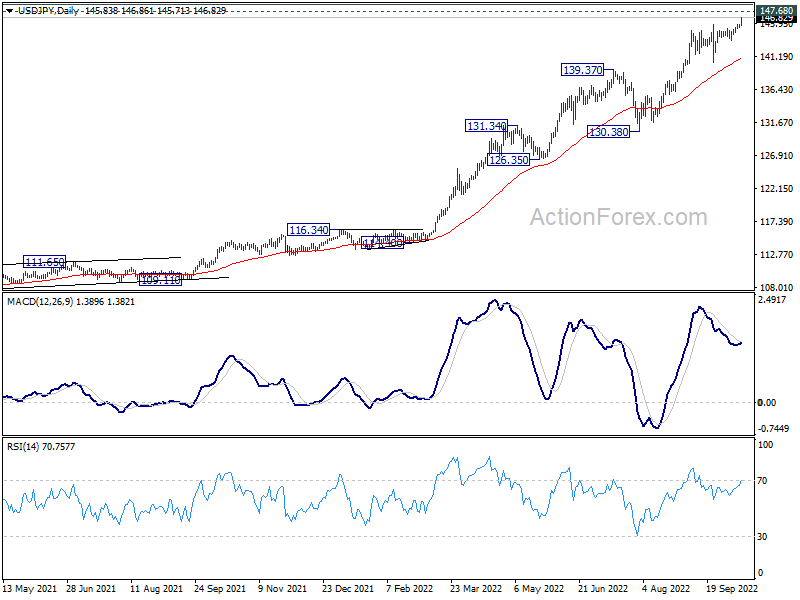

In the bigger picture, up trend from 101.18 is still in progress, as part of the whole up trend from 75.56 (2011 low). Further rise should be seen to 147.68 (1998 high), and possibly to 100% projection of 75.56 (2011 low) to 125.85 (2015 high) from 98.97 at 149.26, For now, break of 130.38 support is needed to be the first indication of medium term topping. Otherwise, outlook will stay bullish even in case of deep pull back.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Machinery Orders M/M Aug | -5.80% | -2.30% | 5.30% | |

| 06:00 | GBP | GDP M/M Aug | -0.30% | 0.10% | 0.20% | 0.10% |

| 06:00 | GBP | Index of Services 3/3M Aug | -0.10% | 0.10% | -0.20% | |

| 06:00 | GBP | Industrial Production M/M Aug | -1.80% | -0.20% | -0.30% | |

| 06:00 | GBP | Industrial Production Y/Y Aug | -5.20% | 0.60% | 1.10% | |

| 06:00 | GBP | Manufacturing Production M/M Aug | -1.60% | 0.00% | 0.10% | |

| 06:00 | GBP | Manufacturing Production Y/Y Aug | -6.70% | 0.70% | 1.10% | |

| 06:00 | GBP | Goods Trade Balance (GBP) Aug | -19.3B | -20.5B | -19.4B | -17.6B |

| 09:00 | EUR | Eurozone Industrial Production M/M Aug | 1.50% | 0.50% | -2.30% | |

| 12:00 | GBP | NIESR GDP Estimate Sep | -0.30% | -0.30% | ||

| 12:30 | USD | PPI M/M Sep | 0.40% | 0.20% | -0.10% | -0.20% |

| 12:30 | USD | PPI Y/Y Sep | 8.50% | 8.30% | 8.70% | |

| 12:30 | USD | PPI Core M/M Sep | 0.30% | 0.30% | 0.40% | 0.30% |

| 12:30 | USD | PPI Core Y/Y Sep | 7.20% | 7.30% | 7.30% | |

| 18:00 | USD | FOMC Minutes |

{kind=link}