Canadian Dollar surges broadly after employment blows past expectations. While US non-farm payroll growth was solid, Dollar reacted more to improving risk sentiment and fall sharply. Yen is the second weakest for the day following the greenback. European majors are gaining against the greenback but are all under heavy selling pressure against commodity currencies.

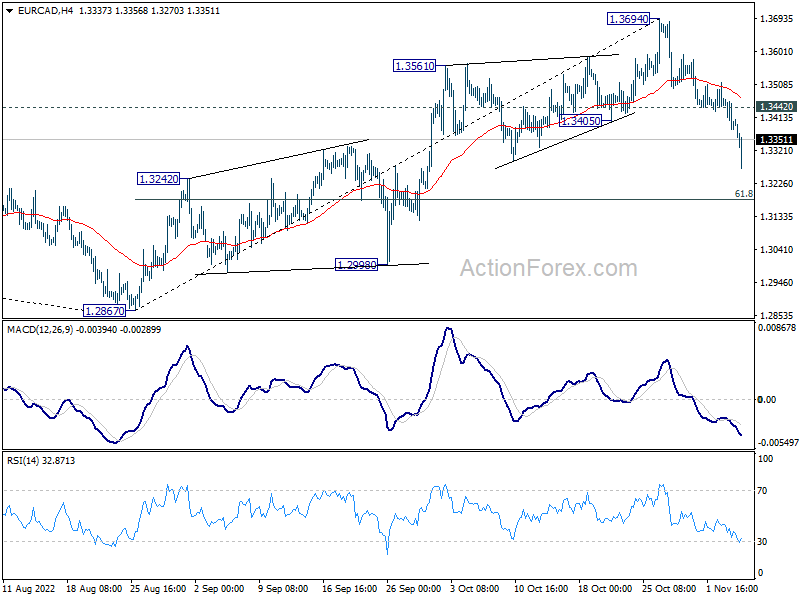

Technically, EUR/CAD’s steep decline suggests that it’s at least on correction to whole rise from 1.2867. Further decline is expected as long as 1.3442 minor resistance holds. The next line of defense is 61.8% retracement of 1.2867 to 1.3694 at 1.3183. Reaction to this fibonacci level would very much depends on whether USD/CAD would break through 1.3494/3501 support to complete a head and shoulder top reversal pattern.

In Europe, at the time of writing, FTSE is up 1.58%. DAX is up 1.81%. CAC is up 2.34%. Germany 10-year yield is up 0.030 at 2.275. Earlier in Asia, Nikkei dropped -1.68%. Hong Kong HSI rose 5.36%. China Shanghai SSE rose 2.43%. Singapore Strait Times rose 0.89%. Japan 10-year JGB yield rose 0.010 to 0.257.

US NFP rose 261k in Oct, unemployment rate rose to 3.7%

US non-farm payroll employment grew 261k in October, well above expectation of 200k. Prior month’s figure was also revised sharply higher from 263k to 315k. Monthly job growth has averaged 407k thus far in 2022.

Unemployment rate rose from 3.5% to 3.7%, above expectation of 3.6%. Number of unemployed persons rose 306k to 6.1m. Labor force participation rate, dropped -0.1% to 62.2%. Average hourly earnings rose 0.4% mom, above expectation of 0.3% mom.

Canada employment grew 108k in Oct, unemployment rate steady at 5.2%

Canada employment grew strongly by 108k in October, well above expectation of 11k.

Unemployment rate held steady at 5.2%. Labor forecast participation rate rose 0.2% to 64.9%.

Year-over-year growth in the average hourly wages of employees remained above 5% for a fifth consecutive month in October, rising 5.6% yoy. Total hours worked increased 0.7% mom.

BoE Pill: Interest rates don’t need to rise as high as markets are pricing

BoE Chief Economist Huw Pill told CNBC, “Our current assessment is that we don’t think interest rates would need to rise as high as markets are pricing precisely because it would produce a slowdown in the economy that is bigger than we need to get these prices under control.”

“That is why the message has been, yes, maybe the market was pricing in too aggressively over this period of turmoil where bank rate is headed. What we are seeking, are always seeking is to find that balance that gets us back to the 2% inflation target without generating unnecessary and costly problems in the real economy,” he said.

He added that the challenge is to “ensure that inflation, particularly this domestically generated inflation, is evolving consistent with our target in a sustainable way”. At the same time, “also to avoid that we overshoot in the opposite direction and generate a slowdown that is not required.”

The question for us is, even as headline inflation begins to fall, have we done enough with monetary policy to contain those underlying or persistent dynamics on inflation to ensure that they end up consistent with our target over time? And I think the answer to that is, we still think there’s more to do to control that domestically driven wage-price cost dynamic.”

ECB Lagarde: Withdrawing accommodation may not be enough to bring inflation back to target

ECB President Christine Lagarde said in a speech that after increasing interest rates by 200bps, “we expect to raise rates further”. He added that, “withdrawing accommodation may not be enough to bring inflation back to our target”. But how much further to go, and how fast, will be determined by a few factors.

The first and most important factor is “inflation outlook”. The second factor is “corresponding policy stance and its transmission lags into demand and inflation”.With the lag in transmission and prevailing uncertainty, “the rate path ahead will look different depending on the contingencies we face.”

Eurozone PPI up 1.6% mom, 41.9% yoy in Sep

Eurozone PPI rose 1.6% mom, 41.9% yoy in September, below expectation of 1.7% mom, 42.0% yoy. For the month, industrial producer prices in Eurozone increased by 3.3% in the energy sector, by 0.9% for non-durable consumer goods, by 0.4% for capital goods and for durable consumer goods and by 0.1% for intermediate goods. Prices in total industry excluding energy increased by 0.4%.

EU PPI rose 1.5% mom, 41.4% yoy. The highest monthly increases in industrial producer prices were recorded in Bulgaria (+9.2%), Slovakia (+8.9%) and Italy (+3.5%), while the largest decreases were observed in Ireland (-18.9%), Estonia (-3.9%) and Greece (-2.4%).

Eurozone PMI Composite finalized at 47.3, headed for a winter recession

Eurozone PMI Services was finalized at 48.5 in October, down from September’s 48.8, a 20-month low. PMI Composite was finalized at 47.3, down from prior month’s 48.1, a 23-month low. Looking at some member states, Germany PMI Composite dropped to 45.1 (29-month low), Italy to 45.8 (22-month low), Spain to 48.0 (9-month low), France to 50.2 (19-month low), and Ireland to 52.1, (2-month low).

Joe Hayes, Senior Economist at S&P Global Market Intelligence said:

“After a weak third quarter of PMI and official GDP data, the latest survey results for the start of the fourth quarter suggest the eurozone economy is now headed for a winter recession. High inflation is dampening demand and hurting business confidence. Fears that the energy crisis could intensify over the winter period are also feeding uncertainty and weighing on decision-making.

“Nonetheless, the ECB will want to continue with monetary tightening to contain inflation. October PMI data suggest inflationary pressures remained extremely elevated across the eurozone. We did, however, see some dovish tones in the rhetoric surrounding the ECB’s October policy decision, clearly showing that the Governing Council are concerned by the rapidly deteriorating economic outlook. A substantial worsening of economic conditions in the coming months may give policymakers a difficult decision to make with regards to the path of monetary tightening, for fear of being too aggressive and prolonging the downturn.”

RBA downgrades 2023, 2024 growth forecast, raised inflation

In the Statement on Monetary Policy, RBA noted that after a sequence of 50bps and 24bps rate hikes, “the Board recognised that interest rates had already been increased significantly in a short period of time”.

“In an uncertain environment, slowing the adjustment of policy allows time to assess the effects of the increases to date and the evolving economic outlook,” it added.

The Board expects that “interest rates will need to increase further”, but “monetary policy is not on a pre-set path”. The size and timing of future interest rate hikes will be determined by incoming data and assessment of the outlook of inflation and labor market.

In the new economic projections, year-average GDP growth forecast for:

- 2022 was left unchanged at 4%.

- 2023 was downgraded from 2.25% to 2.00%.

- 2024 was downgraded from 1.75% to 1.50%.

Year-end forecasts for headline CPI for:

- 2022 was revised up from 7.75% to 8.00%.

- 2023 was revised up from 4.25% to 4.75%.

- 2024 was revised up from 3.00% to 3.25%.

Year-end forecasts for trimmed mean CPI for:

- 2022 was revised up from 6.00% to 6.25%.

- 2023 was left unchanged at 3.75%.

- 2024 was revised up from 3.00% to 3.25%.

Year-end forecasts for unemployment rate for:

- 2022 was revised up from 3.25% to 3.50%.

- 2023 was revised up from 3.50% to 3.75%.

- 2024 was revised up from 4.00% to 4.25%.

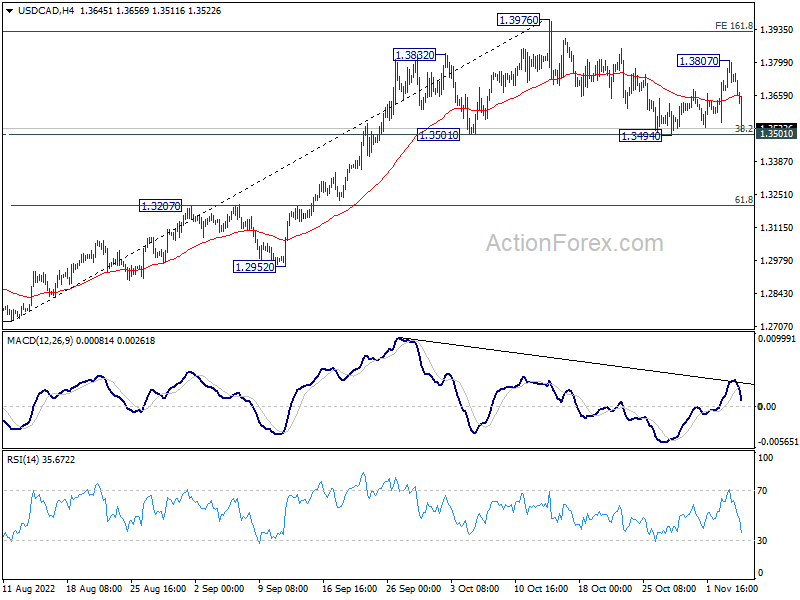

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.3683; (P) 1.3746; (R1) 1.3808; More….

Immediate focus is now on 1.3494/3501 support in USD/CAD. Sustained break there will complete a head and shoulder top pattern (ls: 1.3832; h: 1.3976; rs: 1.3807). Outlook will be turned bearish for deeper fall to 1.3207 cluster support (61.8% retracement of 1.2726 to 1.3976 at 1.3204. On the upside, above 1.3807 minor resistance will bring retest of 1.3976 high.

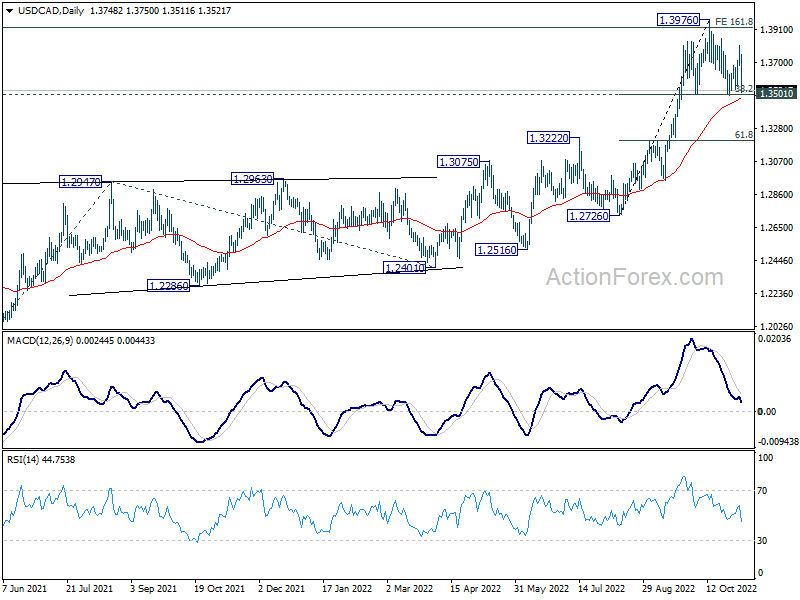

In the bigger picture, up trend from 1.2005 (2021 low) is still in progress. Based on current impulsive momentum, it could be resuming long term up trend from 0.9056 (2007 low). Whether it is or it isn’t, retest of 1.4689 (2016 high) should be seen next. This will now remain the favored case as long as 1.3222 resistance turned support holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:30 | AUD | AiG Performance of Construction Index Oct | 43.3 | 46.5 | ||

| 07:00 | EUR | Germany Factory Orders M/M Sep | -4.00% | -0.60% | -2.40% | -2.00% |

| 07:45 | EUR | France Industrial Output M/M Sep | -0.80% | -1.00% | 2.40% | |

| 08:45 | EUR | Italy Services PMI Oct | 46.4 | 48.5 | 48.8 | |

| 08:50 | EUR | France Services PMI Oct F | 51.7 | 51.3 | 51.3 | |

| 08:55 | EUR | Germany Services PMI Oct F | 46.5 | 44.9 | 44.9 | |

| 09:00 | EUR | Eurozone Services PMI Oct F | 48.6 | 48.2 | 48.2 | |

| 09:30 | GBP | Construction PMI Oct | 53.2 | 52.1 | 52.3 | |

| 10:00 | EUR | Eurozone PPI M/M Sep | 1.60% | 1.70% | 5.00% | |

| 10:00 | EUR | Eurozone PPI Y/Y Sep | 41.90% | 42.00% | 43.30% | 43.40% |

| 12:30 | USD | Nonfarm Payrolls Oct | 261K | 200K | 263K | 315K |

| 12:30 | USD | Unemployment Rate Oct | 3.70% | 3.60% | 3.50% | |

| 12:30 | USD | Average Hourly Earnings M/M Oct | 0.40% | 0.30% | 0.30% | |

| 12:30 | CAD | Net Change in Employment Oct | 108.3K | 11.0K | 21.1K | |

| 12:30 | CAD | Unemployment Rate Oct | 5.20% | 5.30% | 5.20% | |

| 14:00 | CAD | Ivey PMI Oct | 60.2 | 59.5 |

{kind=link}