Dollar stays generally weak today but selling pressure is so far limited. Markets are looking forward to FOMC’s rate hike as well as new economic projections. Yen is currently the strongest one for the day, followed by Aussie and Swiss Franc. New Zealand Dollar is the weakest, followed by Canadian and Sterling. Much volatility is expected in the next 24 hours with SNB, BoE and ECB featured tomorrow.

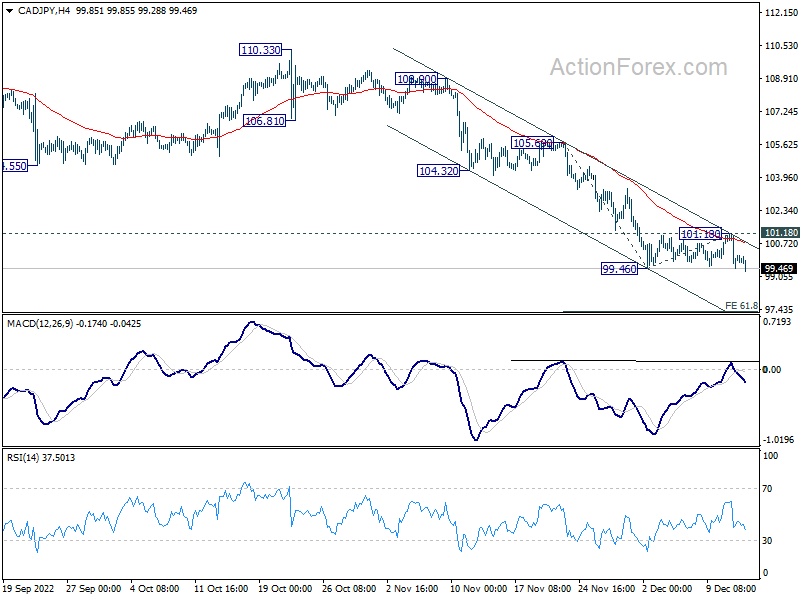

Technically, CAD/JPY finally breaks out to the downside as consolidation from 99.46 completed at 101.18. Near term outlook remains clearly bearish with rejection from 4 hour 55 EMA and near term falling channel. Further decline is now expected to 61.8% projection of 105.69 to 99.46 from 101.18 at 97.32.

In Europe, at the time of writing, FTSE is down -0.19%. DAX is down -0.57%. CAC is down -0.38%. Germany 10-year yield is up 0.040 at 1.963. Earlier in Asia, Nikkei rose 0.72%. Hong Kong HSI rose 0.39%. China Shanghai SSE rose 0.01%. Singapore Strait Times rose 0.22%. Japan 10-year JGB yield rose 0.0031 to 0.258.

Canada manufacturing sales rose 2.8% mom in Oct, driven by higher prices

Canada manufacturing sales rose 2.8% mom to CAD 72.6B in October, above expectation of 1.9% mom.

Sales increased in 12 of 21 industries, led by the petroleum and coal (+12.7%), food (+2.9%), chemical (+4.9%) and miscellaneous manufacturing (+13.3%) industries. Meanwhile, motor vehicles (-3.2%) and machinery (-1.7%) posted the largest monthly declines.

But Statistics Canada also noted: “Sales in constant dollars were unchanged in October, indicating that the entire increase in current dollar sales was driven by higher prices as the Industrial Product Price Index rose 2.4% in October. ”

Eurozone industrial production down -2.0% mom in Oct, EU down -1.9% mom

Eurozone industrial production dropped -2.0% mom in October, worse than expectation of -1.4% mom. Production of energy fell by -3.9%, durable consumer goods by -1.9%, intermediate goods by -1.3% and capital goods by -0.6%, while production of non-durable consumer goods rose by 0.3%.

EU industrial production dropped -1.9% mom. Among Member States for which data are available, the largest monthly decreases were registered in Ireland (-10.7%), Luxembourg (-4.4%) and Czechia (-3.7%). Increases were observed in Slovakia (+1.3%), Lithuania (+1.1%), Greece (+0.5%) and Austria (+0.2%).

Ifo: Germany economy to contract in Q4 and Q1

Ifo said the German economy is “suffering from huge supply shocks”. Price press is “not expected to ease until 2024, and then only slowly”. Overall inflation is expected to fall from 7.8% in 2022 to 6.4% in 2023. However, core inflation is expected to rise from 4.8% to 5.8% next year.

Ifo also said Germany GDP is forecast to grow 1.8% in 2022, contract slightly by -0.1% in 2023, and back at 1.6% in 2024. Economy output to expected to fall by -0.3% qoq and -0.4% qoq in the two quarters of the 2022-23 winter half-year (i.e. Q4 and Q1). Thus, Germany will be technically in a recession. But starting in spring 2023, the economy is expected recovery and growth at stronger rates in the second half .

UK CPI slowed to 10.7% yoy in Nov, core CPI down to 6.3% yoy

UK CPI rose 0.4% mom in November, below expectation of 0.6% mom. In the 12 months to November, CPI slowed from 11.1% yoy to 10.7% yoy, below expectation of 10.9% yoy. Core CPI also slowed from 6.5% yoy to 6.3% yoy, below expectation of 6.5% yoy.

ONS said: “The easing in the annual inflation rate in November 2022 reflected, principally, price changes in the transport division, particularly for motor fuels and second-hand cars. There were also downward effects from tobacco, accommodation services, clothing and footwear, and games, toys and hobbies. The largest, partially offsetting, upward effect came from price rises for alcohol in restaurants, cafes and pubs.”

Japan Tankan manufacturing mood deteriorated, but non-manufacturing upbeat

Japan Tankan Large Manufacturing Index dropped from 8 to 7 in Q4, above expectation of 6. Sentiment has been deteriorating for the fourth straight quarter, and hit the lowest level since Q1 2021. Large Manufacturing Outlook dropped from 9 to 6, matched expectations.

On the other hand, Large Non-Manufacturing Index rose from 14 to 19, above expectation of 17. That’s the highest level since Q4 2019. Large Non-Manufacturing Outlook was unchanged at 11, below expectation of 16.

Large all industry capex dropped from 21.5% to 19.2%, above expectation of 18.4%.

Regarding inflation, 1-year ahead general prices expectations for all industries rose from 2.6% to 2.7%. 3-year ahead expectations rose from 2.1% to 2.2%. 5-year ahead expectations was unchanged at 2.0%.

RBNZ Hawkesby: We’ve seen very little impact of higher interest rates so far

RBNZ Deputy Governor Christian Hawkesby said in a speech that “we still think we have more work to do” to bring down inflation.

“We’ve seen very little impact of higher interest rates so far, outside of falling house prices and a cooling of the construction pipeline,” he added.

“As inflation expectations have been rising, we also think that neutral interest rates have drifted higher, meaning that the OCR needs to be higher than otherwise before monetary policy is really restricting the demand side of the economy,” he said.

Hawkesby pointed to November projections that the OCR would peak around 5.50%. But he noted, “25 years as an economist has taught me that the only certainty is that our forecasts won’t be exactly right. There are always shocks and unexpected developments that will evolve the story.”

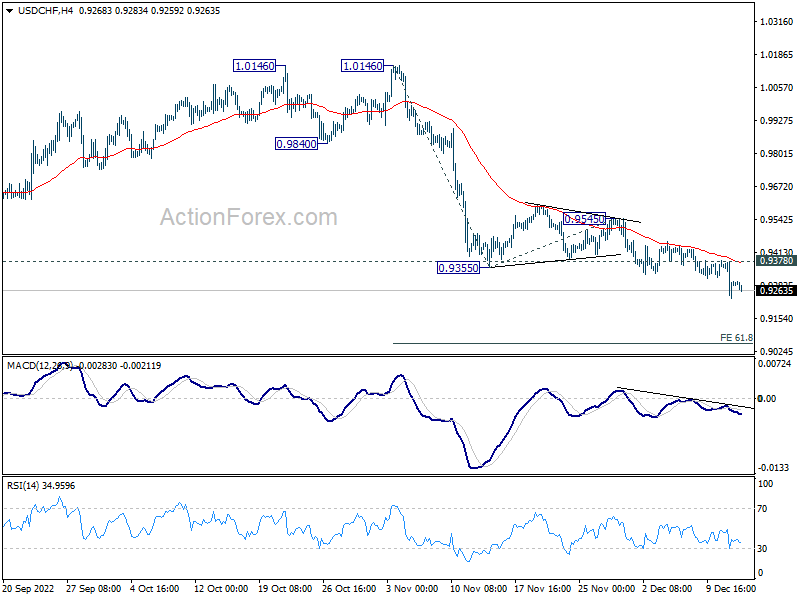

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9220; (P) 0.9297; (R1) 0.9363; More…

USD/CHF’s decline from 1.0146 is in progress and intraday bias stays on the downside. Next target is 61.8% projection of 1.0146 to 0.9355 from 0.9545 at 0.9056. However, break of 0.9378 resistance will indicate short term bottoming and turn bias back to the upside for 0.9545 resistance instead.

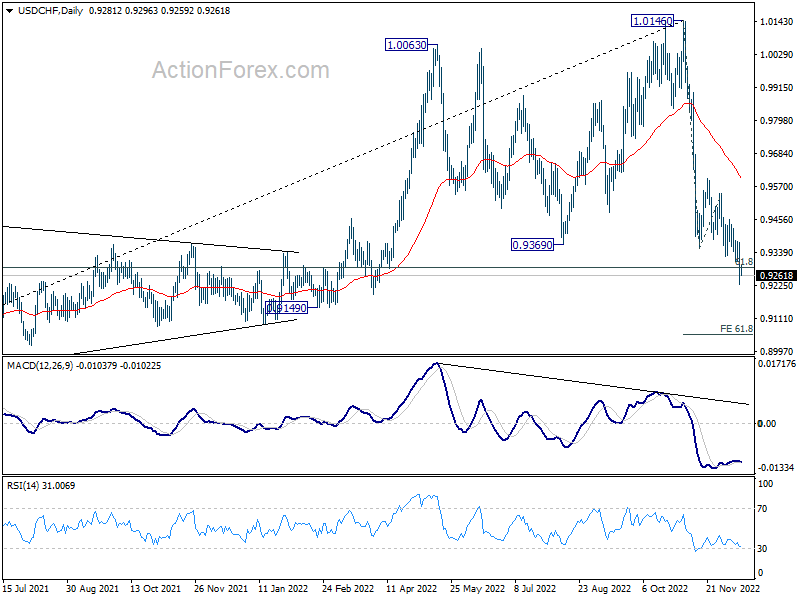

In the bigger picture, rise from 0.8756 (2021 low) has completed at 1.0146, well ahead of 1.0342 long term resistance (2016 high). Based on current downside momentum, fall from 1.0146 might be a medium term down trend itself. Sustained break of 61.8% retracement of 0.8756 to 1.0146 at 0.9287 will pave the way to 0.8756. In any case, risk will stay on the downside as long as 0.9545 resistance holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | Current Account (NZD) Q3 | -10.21B | -10.20B | -5.22B | -5.42B |

| 23:50 | JPY | Tankan Large Manufacturing Index Q4 | 7 | 6 | 8 | |

| 23:50 | JPY | Tankan Large Manufacturing Outlook Q4 | 6 | 6 | 9 | |

| 23:50 | JPY | Tankan Non – Manufacturing Index Q4 | 19 | 17 | 14 | |

| 23:50 | JPY | Tankan Non – Manufacturing Outlook Q4 | 11 | 16 | 11 | |

| 23:50 | JPY | Tankan Large All Industry Capex Q4 | 19.20% | 18.40% | 21.50% | |

| 23:50 | JPY | Machinery Orders M/M Oct | 5.40% | -1.00% | -4.60% | |

| 04:30 | JPY | Industrial Production M/M Oct F | -3.20% | -2.60% | -2.60% | |

| 07:00 | GBP | CPI M/M Nov | 0.40% | 0.60% | 2.00% | |

| 07:00 | GBP | CPI Y/Y Nov | 10.70% | 10.90% | 11.10% | |

| 07:00 | GBP | Core CPI Y/Y Nov | 6.30% | 6.50% | 6.50% | |

| 07:00 | GBP | RPI M/M Nov | 0.60% | 1.50% | 2.50% | |

| 07:00 | GBP | RPI Y/Y Nov | 14.00% | 14.30% | 14.20% | |

| 07:30 | CHF | Producer and Import Prices M/M Nov | -0.50% | 0.40% | 0.00% | |

| 07:30 | CHF | Producer and Import Prices Y/Y Nov | 3.80% | 4.80% | 4.90% | |

| 10:00 | EUR | Eurozone Industrial Production M/M Oct | -2.00% | -1.40% | 0.90% | 0.80% |

| 13:30 | CAD | Manufacturing Sales M/M Oct | 2.80% | 1.90% | 0.00% | |

| 13:30 | USD | Import Price Index M/M Nov | -0.60% | -0.50% | -0.20% | |

| 15:30 | USD | Crude Oil Inventories | -3.4M | -5.2M | ||

| 19:00 | USD | Fed Interest Rate Decision | 4.50% | 4.00% | ||

| 19:30 | USD | FOMC Press Conference |

{kind=link}