Dollar attempted to extend recovery today but once again lacked follow through momentum. The greenback is mildly supported by slight risk aversion, but lags behind Yen and Swiss Franc. For now, Australian Dollar remains the worst for the day on poor retail sales data, followed by Canadian and New Zealand Dollar. Euro and Sterling are mixed despite better than expected Eurozone GDP. Moves in the financially will likely lacks firepower until tomorrow’s FOMC rate decision and statement.

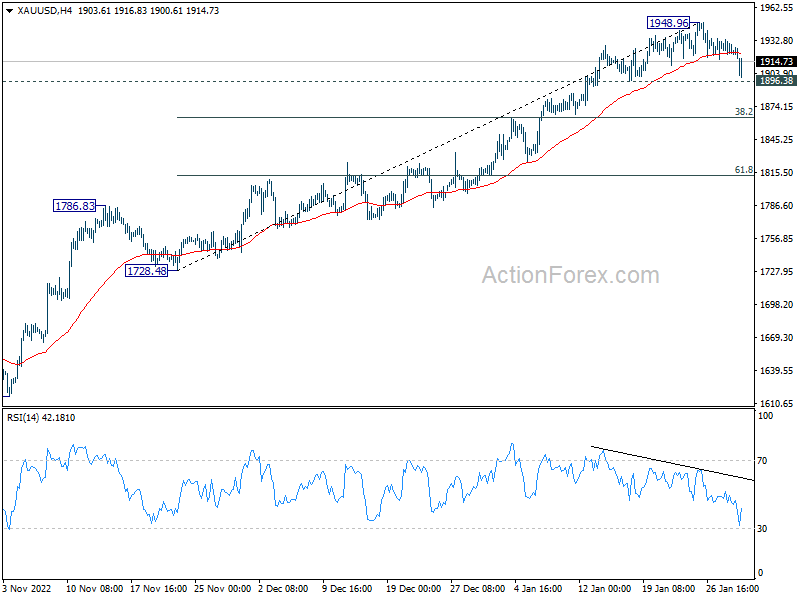

Technically, deeper pull back should be due in Gold considering the extended loss of upside momentum, as seen in 4 hour MACD. Firm break of 1896.38 minor support should confirm short term topping, and bring deeper pull back to 38.2% retracement of 1728.48 to 1948.96 at 1864.73, Ideally, if that happens, it should be accompanied by a stronger rebound in Dollar.

In Europe, at the time of writing, FTSE is down -0.53%. DAX is down -0.32%. CAC is down -0.21%. Germany 10-year yield is down -0.0044 at 2.275. Earlier in Asia, Nikkei dropped -0.39%. Hong Kong HSI dropped -1.03%. China Shanghai SSE dropped -0.42%. Singapore Strait Times dropped -0.37%. Japan 10-year JGB yield rose 0.0178 to 0.499.

Canada GDP rose 0.1% mom in Nov, to be essentially flat in Dec

Canada GDP grew 0.1% mom in November, matched expectations. Services-producing industries expanded 0.2% mom while goods-producing industries contracted -0.1% mom. 14 of 20 industrial sectors increased in the month.

Advance information indicates that real GDP was essentially unchanged in December. Also for Q4, GDO growth should be 0.4% qoq, 3.8% yoy.

Also released, US employment cost index rose 1.0% in Q4, below expectation of 1.2%. Wages and salaries rose 1.0%. Benefit costs rose 0.8%.

Eurozone GDP grew 0.1% qoq, 1.9% yoy in Q4,

Eurozone GDP grew 0.1% qoq in Q4, better than expectation of -0.2% qoq. Comparing to the same quarter a year ago, GDP rose 1.9% yoy. EU GDP was flat qoq in Q4, up 1.8% yoy. Annual growth in 2022 was 3.5% in Eurozone and 3.6% in EU.

Among the Member States for which data are available for the fourth quarter of 2022, Ireland (+3.5%) recorded the highest increase compared to the previous quarter, followed by Latvia (+0.3%), Spain and Portugal (both +0.2%). The highest declines were recorded in Lithuania (-1.7%) as well as in Austria (-0.7%) and Sweden (-0.6%).

The year-on-year growth rates were positive for all countries except for Sweden (-0.6%) and Lithuania (-0.4%).

France GDP grew 0.1% qoq in Q4, up 2.6% in 2022

France GDP grew 0.1% qoq in Q4, better than expectation of 0.0% qoq. On average over the year 2022, GDP increased by 2.6% (after +6.8% in 2021 and -7.9% in 2020).

This annual growth figure was essentially the result of the rebound in activity in the second and third quarters of 2021, as the health crisis receded. Quarter-on-quarter growth was significantly less dynamic over the year 2022. The growth overhang for 2023 stands at +0.3% at the end of the fourth quarter of 2022.

China official PMI manufacturing rose to 50.1, non-manufacturing up to 54.4

China official PMI Manufacturing rose from 47.0 to 50.1 in December, slightly below expectation of 50.2. PMI Non-Manufacturing jumped from 41.6 to 54.4, above expectation of 51.0. Both indexes were also back in expansion region.

Senior NBS statistician Zhao Qinghe noted that economic activity returned to expansion amid an improvement in the business operation climate and the situation.

“Meanwhile, many companies in the manufacturing and services sectors still reported a lack of market demand is the major concern for their businesses. The foundation of economic recovery still needs to be further consolidated,” he added.

Japan industrial production declined -0.1% mom in Dec, but expected to rebound

Japan industrial production declined -0.1% mom in December, much better than expectation of -0.8% mom. The Ministry of Economy, Trade and Industry retained the assessment from the previous month that industrial production is “weakening.” 10 of the 15 industries surveyed, reported decline in output, four reported increase, and one remained unchanged.

Based on a poll of manufacturers, the ministry expects output to remain flat in January, and then grow 4.1% in February. A ministry official said, “we still need to keep a close eye on the influence of a potential spread in coronavirus infections, material shortages and high prices.”

Also released, retail sales rose 3.8% yoy in December, above expectation of 3.1% yoy. Unemployment rate was unchanged at 2.5%. housing starts dropped -1.7% yoy. Consumer confidence rose from 30.3 to 31.0 in January.

Australia retail sales turnover down sharply by -3.9% mom in Dec

Australia retail sales turnover dropped sharply by -3.9% mom to AUD 34.47m in December, much worse than expectation of -0.3% mom. That’s the first contraction after 11 straight months of growth. Still, sales turnover remained elevated at its sixth highest level on record, and was up 7.5% yoy for the year.

Ben Dorber, ABS head of retail statistics, said: “The large fall in December suggests that retail spending is slowing due to high cost-of-living pressures… The latest Consumer Price Index showed that prices continued to rise strongly in the December quarter. To see the effect of consumer prices on recent turnover growth, it will be important to look at quarterly retail sales volumes which we will release next week.”

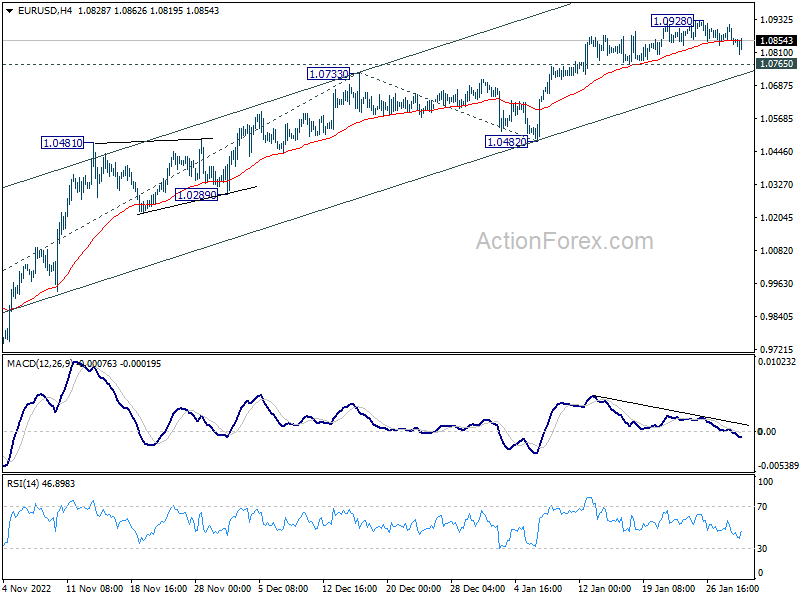

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0823; (P) 1.0868; (R1) 1.0898; More…

EUR/USD continues to gyrate lower but stays above 1.0765 support, comfortably so far. Intraday bias remains neutral for the moment. With 1.0765 support intact, further rally remains in favor. On the upside, break of 1.0928 will resume larger rise to 61.8% projection of 0.9630 to 1.0733 from 1.0482 at 1.1164 next. On the downside, though, break of 1.0765 support should now confirm short term topping, and turn bias back to the downside for 55 day EMA (now at 1.0601).

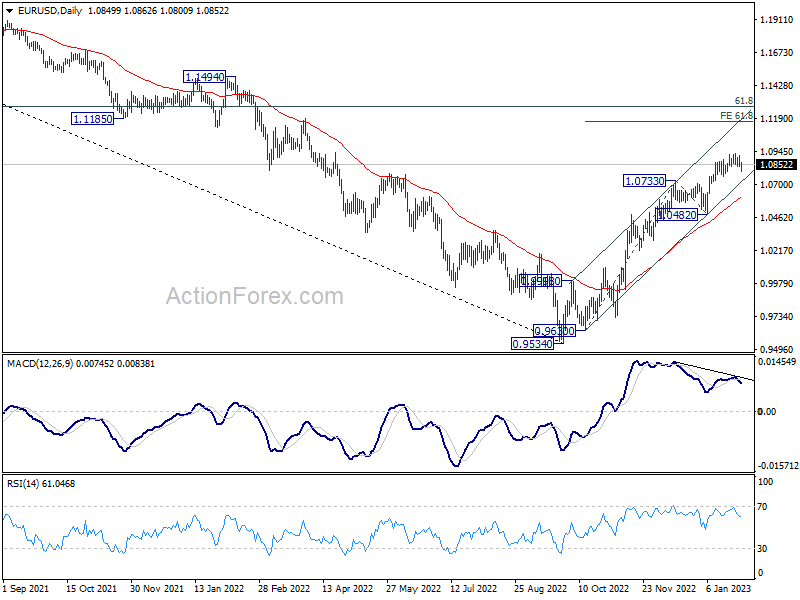

In the bigger picture, current development suggests that the rally from 0.9534 low (2022 low) is a medium term up trend rather than a correction. Further rise is in favor to 61.8% retracement of 1.2348 (2021 high) to 0.9534 at 1.1273 next. This will remain the favored case as long as 1.0482 support holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | Unemployment Rate Dec | 2.50% | 2.50% | 2.50% | |

| 23:50 | JPY | Industrial Production M/M Dec P | -0.10% | -0.80% | 0.20% | |

| 23:50 | JPY | Retail Trade Y/Y Dec | 3.80% | 3.10% | 2.50% | |

| 00:30 | AUD | Private Sector Credit M/M Dec | 0.30% | 0.50% | 0.50% | |

| 00:30 | AUD | Retail Sales M/M Dec | -3.90% | -0.30% | 1.40% | 1.70% |

| 01:00 | CNY | Manufacturing PMI Dec | 50.1 | 50.2 | 47 | |

| 01:00 | CNY | Non-Manufacturing PMI Dec | 54.4 | 51 | 41.6 | |

| 05:00 | JPY | Consumer Confidence Jan | 31 | 30.5 | 30.3 | |

| 05:00 | JPY | Housing Starts Y/Y Dec | -1.70% | 0.50% | -1.40% | |

| 06:30 | EUR | France Consumer Spending M/M Dec | -1.30% | 0.20% | 0.50% | |

| 06:30 | EUR | France GDP Q/Q Q4 P | 0.10% | 0.00% | 0.20% | |

| 07:30 | CHF | Real Retail Sales Y/Y Dec | -2.80% | 2.60% | -1.30% | -1.40% |

| 08:55 | EUR | Germany Unemployment Change Dec | -22K | 5K | -13K | |

| 08:55 | EUR | Germany Unemployment Rate Dec | 5.50% | 5.50% | 5.50% | |

| 09:30 | GBP | Mortgage Approvals Dec | 36K | 44K | 46K | |

| 09:30 | GBP | M4 Money Supply M/M Dec | -0.80% | -0.30% | -1.60% | |

| 10:00 | EUR | Italy GDP Q/Q Q4 P | -0.10% | -0.20% | 0.50% | |

| 10:00 | EUR | Eurozone GDP Q/Q Q4 P | 0.10% | -0.10% | 0.30% | |

| 13:30 | CAD | GDP M/M Nov | 0.10% | 0.10% | 0.10% | |

| 13:30 | USD | Employment Cost Index Q4 | 1.00% | 1.20% | 1.20% | |

| 14:00 | USD | S&P/CS Composite-20 HPI Y/Y Nov | 6.80% | 8.60% | ||

| 14:00 | USD | Housing Price Index M/M Nov | -0.40% | 0.00% | ||

| 14:45 | USD | Chicago PMI Jan | 45.4 | 44.9 | ||

| 15:00 | USD | Consumer Confidence Jan | 109.2 | 108.3 |

{kind=link}