Yen opens the week broadly lower on rumors that current ultra-loose monetary policy would be maintained by the next BoJ governor. Meanwhile, markets are mixed elsewhere. Dollar is paring some gains after initial rally, but stays generally firm. Australian Dollar is trying to recover with other commodity currencies. Swiss Franc is slightly outperforming other European majors. The economic calendar is light today, and focuses will be on any other development surrounding the shoot-down of Chinese surveillance balloon by the US military.

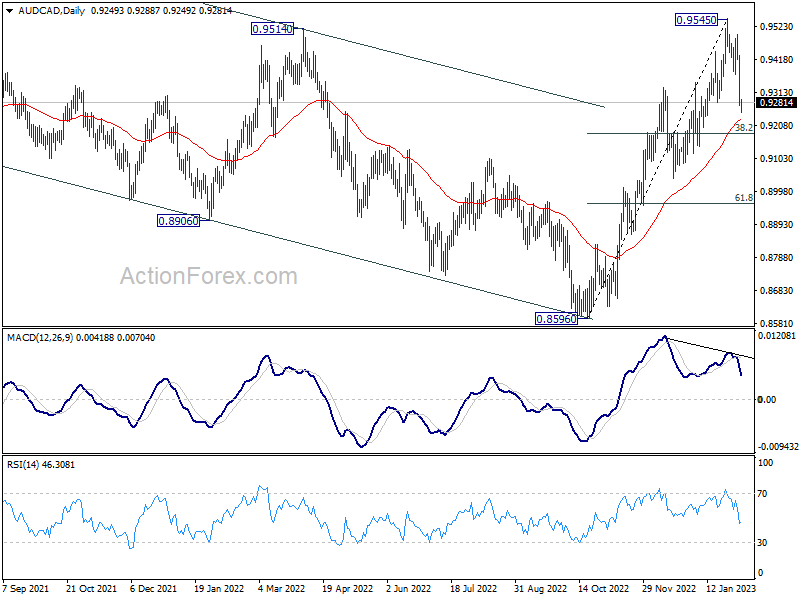

Technically, while AUD/CAD’s correction from 0.9545 was deep, there is no change in the near term bullish outlook. Strong support would be seen between 55 day EMA (now at 0.9233) and 38.2% retracement of 0.8596 to 0.9545 at 0.9182 to contain downside to bring rebound, and then resumption of rise from 0.8596. But that would depend on the reactions to this week’s RBA rate decision.

In Asia, at the time of writing, Nikkei is up 1.06%. Hong Kong HSI is down -2.34%. China Shanghai SSE is down -1.01%. Singapore Strait Times is up 0.15%. Japan 10-year JGB yield is up 0.0042 at 0.495.

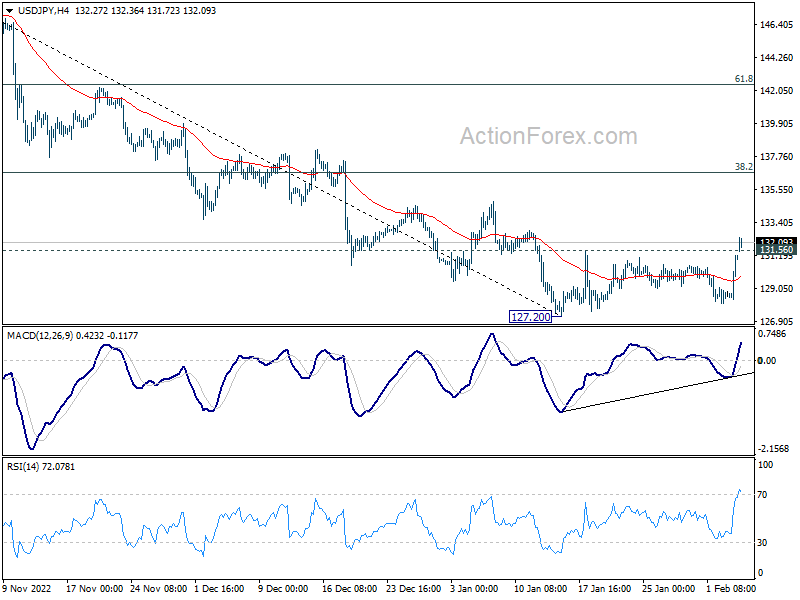

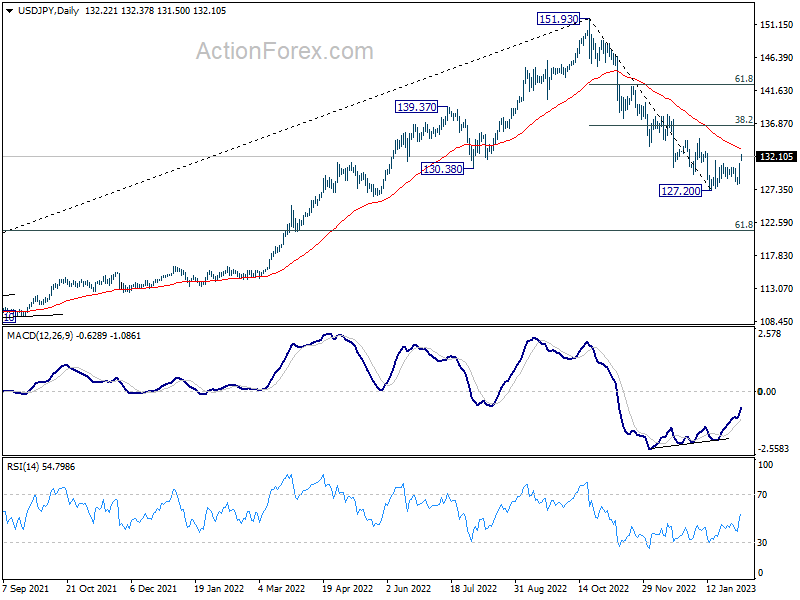

USD/JPY extend rebound on BoJ Amamiya rumor, more upside ahead

Yen tumbles broadly today after Nikkei newspaper reported, quoting unnamed source that current BoJ Deputy Governor Masayoshi Amamiya was approached by the government to take over Governor Haruhiko’s job. The news was seen as bearish for the currency, as Amamiya would likely stick with the current ultra-loose monetary policy, comparing to a hawkish alternative.

Nevertheless, Finance Minister Shunichi Suzuki told reports that he had not heard that the government offered Amamiya the job. The prime minister’s office and the BOJ were also not immediately available to comment. Amamiya did not comment to reporters himself neither.

Kuroda’s term will end on April 8 while his deputies Masayoshi Amamiya and Masazumi Wakatabe will have their terms expire on March 19. The final monetary policy policy meeting the three would hold together would be on March 9-10. The more concrete details of the appointments would probably come in early March by latest.

USD/JPY’s break of 131.56 resistance should confirm short term bottoming at 127.20, on bullish convergence condition in daily MACD. Further rally should be seen to 55 day EMA (now at 133.28) first. Firm break there will target 38.2% retracement of 151.93 to 127.20 at 136.64, even just as a correction to the decline from 151.93.

BoJ Kuroda: Monetary easing steps a necessary approach shared by others

BoJ Governor Haruhiko Kuroda told the parliament today, “with our monetary easing steps, we sought to stimulate economic activity and tighten the labour market so that prices and wages would rise more.”

“This was a necessary approach and one that is shared by other central banks,” he said. There was “no better way” to aim at sustainably achieving its 2% inflation target.

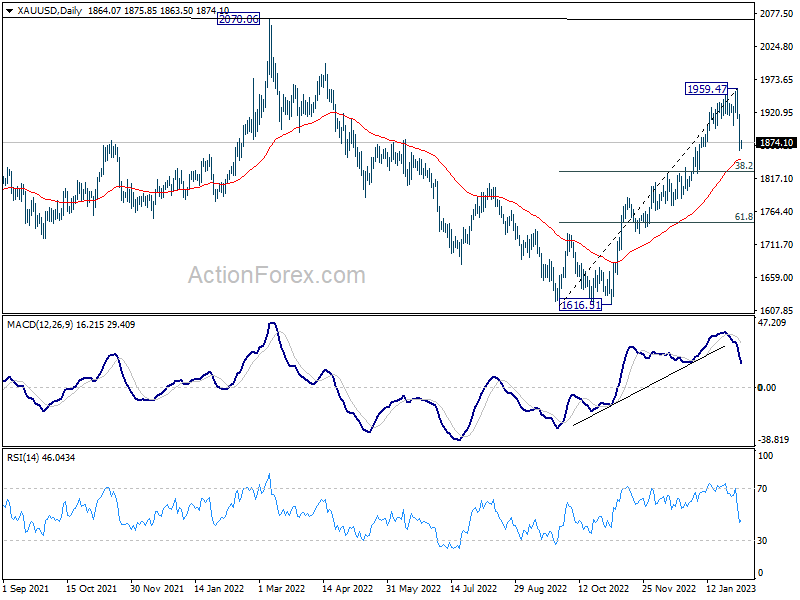

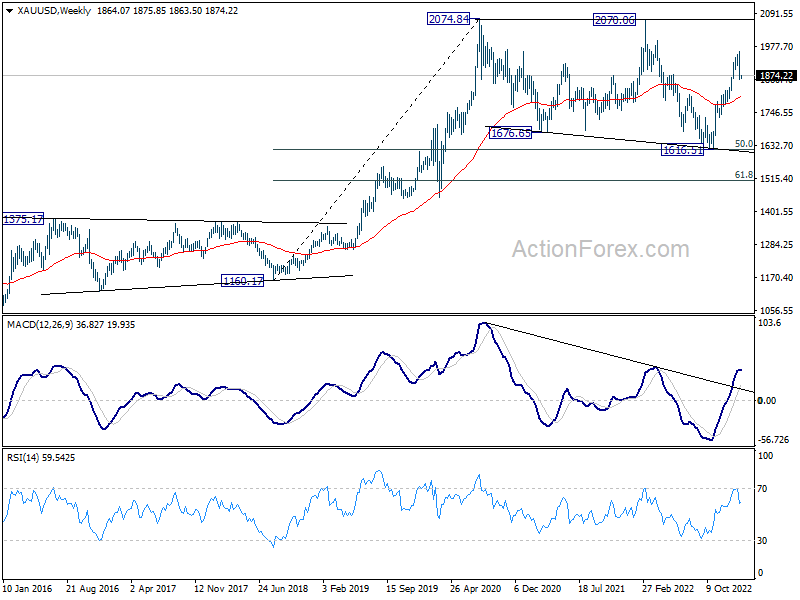

Gold in pull back on strong Dollar rebound

Gold declined sharply last week on the back of strong rebound in Dollar following solid US job and services data. The development indicates short term topping at 1959.47. Deep pull back is now in favor to 55 day EMA (now at 1847.23), or further to 38.2% retracement of 1616.51 to 1959.47 at 1828.45.

Still, as long as 55 week EMA (now at 1798.35) holds, the favored case is still that corrective pattern from 2074.84 has completed with three waves down to 1616.51. That is, rise from there is resuming the larger up trend and should break through 2704.84 “sooner” in medium term.

However, sustained break of the 55 week EMA will argue that corrective pattern from 2074.84 is developing into a five-wave triangle pattern, and delay upside breakout.

RBA to hike 25bps, BoE hearing also watched

RBA is widely expected to continue its tightening pace with 25bps to 3.35% this week. It’s likely not the end of the current cycle yet, and thus markets will be looking for affirmation of another hike in March. While there is scope for another hike in April to bring the terminal rate to 3.85%, it’s still a bit early to make the call. Instead, focus will be on RBA’s assessment on the path of inflation and the risk of recession to see which side the central bank is leaning towards.

BoE monetary policy report hearing is another major central bank activity this week. Sterling was pressured last week after the “perceived” dovish BoE rate hike. There are speculations that the central bank will deliver a final 25 bps hike in March, with interest rate peaking at 4.25%. Governor Andrew Bailey’s comments would be crucial in gauging market expectations.

As for the UK, much attention will also be on GDP and production data to be released on Friday. Other data to be watched include Eurozone Sentix investor confidence, Germany GPI flash, Canada employment, as well as US U of Michigan consumer sentiment. Here are some highlights for the week:

- Monday: Germany factory orders; Eurozone Sentix investor confidence, retail sales; UK construction PMI; Canada Ivey PMI.

- Tuesday: Japan average cash earnings, household spending; RBA rate decision, trade balance; Swiss unemployment rate, foreign currency reserves; Germany industrial production; France trade balance; Canada trade balance; US trade balance.

- Wednesday: Japan bank lending, current account; Italy retail sales; US wholesale inventories final.

- Thursday: UK RICS house price balance; Germany CPI flash; US jobless claims.

- Friday: New Zealand BusinessNZ manufacturing index; Japan PPI machine tool orders; China CPI, PPI; UK GDP, production, trade balance; Italy industrial production; Canada employment; US U of Michigan consumer sentiment.

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0745; (P) 1.0842; (R1) 1.0892; More…

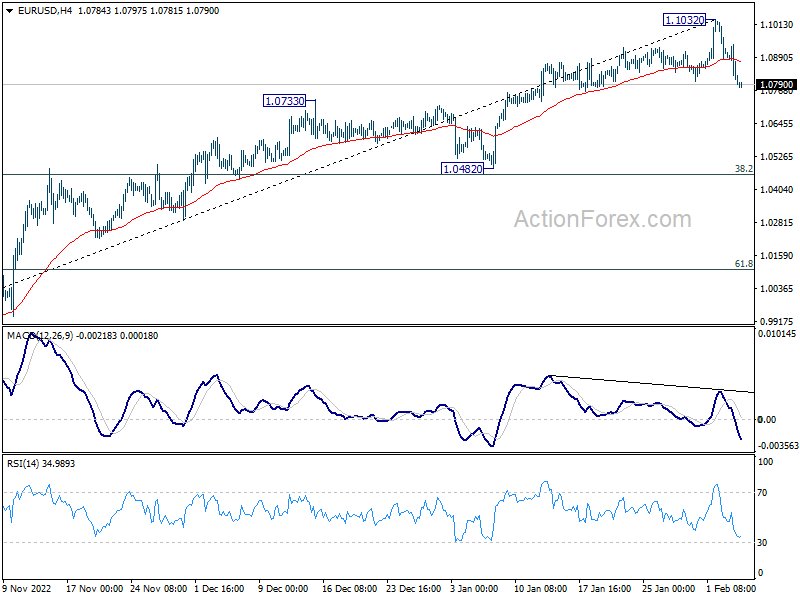

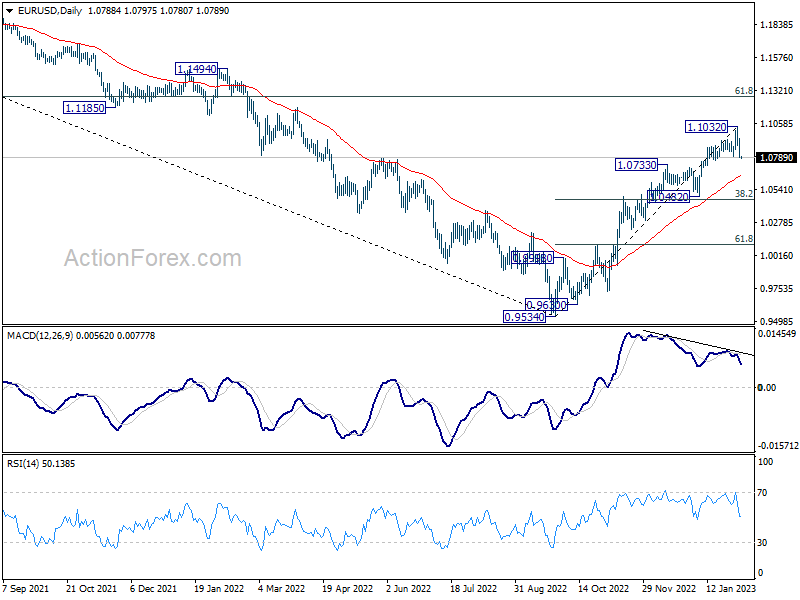

Intraday bias in EUR/USD remains on the downside at this point. Fall form 1.1032 is correcting whole rise from 0.9534, and should target 1.0482 support, which is close to 38.2% retracement of 0.9534 to 1.1032 at 1.0463. For now, risk will stay on the downside as long as 1.1032 resistance holds, in case of recovery.

In the bigger picture, current development suggests that the rally from 0.9534 low (2022 low) is a medium term up trend rather than a correction. Further rise is in favor to 61.8% retracement of 1.2348 (2021 high) to 0.9534 at 1.1273 next. This will remain the favored case as long as 1.0482 support holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 00:00 | AUD | TD Securities Inflation M/M Jan | 0.90% | 0.20% | ||

| 07:00 | EUR | Germany Factory Orders M/M Dec | 2.00% | -5.30% | ||

| 09:30 | EUR | Eurozone Sentix Investor Confidence Feb | -11.8 | -17.5 | ||

| 09:30 | GBP | Construction PMI Jan | 49.5 | 48.8 | ||

| 10:00 | EUR | Eurozone Retail Sales M/M Jan | -2.50% | 0.80% | ||

| 15:00 | CAD | Ivey PMI Jan | 42.3 | 33.4 |

{kind=link}