Selloff in Yen continues today even though 10-year JGB yield closed above BoJ’s 0.5% cap. Traders are probably positioning for a not-that-hawkish BoJ governor nomination by the government tomorrow. Dollar also softens as major European indexes rise, together with US futures. Sterling firms up ahead of a string of economic data this week, including employment (Tue), CPI (Wed) and retail sales (Fri). Aussie and Kiwi are also trading slightly higher. Euro is mixed for now, even though European Commission projects a better economic outlook with higher growth and lower inflation for this year.

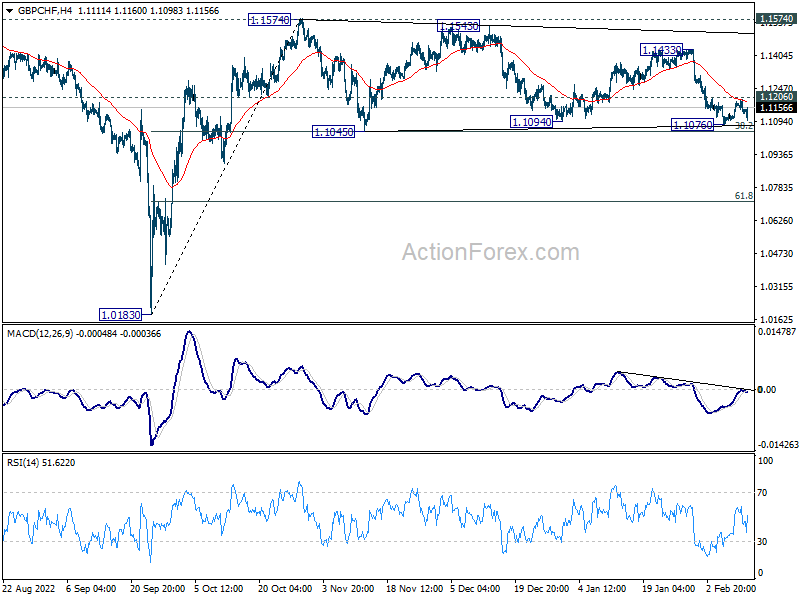

Technically, GBP/CHF should be close to complete the corrective pattern from 1.1574. Firm break of 1.1206 minor resistance should have 4 hour 55 EMA taken out too. Bias will be turned back to the upside for 1.1433 resistance first. Sustained break there will raise the chance of resuming larger rally through 1.1574 high. The next few days would be important for the pound, with clearing of 1.1206 as the first step for GBP/CHF.

In Europe, at the time of writing, FTSE is up 0.25%. DAX is up 0.46%. CAC is up 0.83%. Germany 10-year yield is up 0.015 at 2.381. Earlier in Asia, Nikkei dropped -0.88%. Hong Kong HSI dropped -0.12%. China Shanghai SSE rose 0.72%. Singapore Strait Times dropped -1.07%. Japan 10-year JGB yield rose 0.0129 to 0.504.

European commission upgrades 2023 growth forecasts, lowers inflation slightly

In the Winter interim Forecast, European commission upgraded growth projections for Eurozone in 2023 and downgraded inflation projections.

“Europe’s economy is proving resilient in the face of current challenges. We were able to narrowly avoid a recession. We are somewhat more optimistic about growth prospects and the projected decline in inflation this year,” said Valdis Dombrovskis, Executive Vice-President for an Economy that Works for People.

“We have entered 2023 on a firmer footing than anticipated: the risks of recession and gas shortages have faded and unemployment remains at a record low,” said Paolo Gentiloni, Commissioner for Economy.

GDP growth forecasts for:

- 2023 at 0.9% (upgraded from Autumn’s 0.3%).

- 2024 at 1.5% (unchanged).

HICP inflation forecasts for:

- 2023 at 5.6% (downgraded from 6.1%).

- 2024 at 2.5% (downgraded from 2.6%).

ECB Centeno: For sure, we’re much closer to that terminal rate than before

ECB Governing Council member Mario Centeno told BloombergTV, “for sure, we’re much closer to that terminal rate than before… We’re approaching it and I think March will be a great moment for us to be very clear about it.”

Meanwhile, for the central bank to slow tightening pace from current 50bps per meeting, Centeno said, “we really need to see inflation converging to 2% in the medium term”.

He added, the new forecasts in March are “going to tell us exactly where we are in that process”.

Swiss CPI bounce back to 3.3% yoy in Jan

Swiss CPI rose 0.6% mom in January, above expectation of 0.5% mom. Core CPI (excluding fresh and seasonal products, energy and fuel) was flat mom. Domestic product prices rose 1.0% mom while imported product prices dropped -0.6% mom.

Compared with the same month of the previous year, CPI accelerated from 2.8% yoy to 3.3% yoy, well above expectation of 2.9% yoy. Core CPI rose from 2.0% yoy to 2.2% yoy. Domestic product inflation jumped from 1.9% yoy to 2.6% yoy. Imported product inflation slowed from 5.8% yoy to 5.2% yoy.

NZ BusinessNZ services rose to 54.5, but negative comments trend higher

New Zealand BusinessNZ Performance of Services Index rose from 52.0 to 54.5 in January. Looking at some details, activity/sales rose form 51.9 to 52.1. Employment rebounded strongly from 46.9 to 51.9. New orders/business dropped from 57.7 to 54.5. Stocks/inventories rose from 51.6 to 54.3. Supplier deliveries dropped from 53.9 to 52.0.

BusinessNZ chief executive Kirk Hope said: “Despite the halt in lower expansionary levels, the trend of a higher proportion of negative comments continued in January (61.7%), compared with 58.2% in December and 47.3% in November. The holiday season was a common theme, along with the shortage of labour and general market uncertainty that has been evident for some months now”.

BNZ Senior Economist Doug Steel said that “as encouraging as January’s PSI result might look, we are reluctant to read too much into one month’s result – especially around the holiday period”.

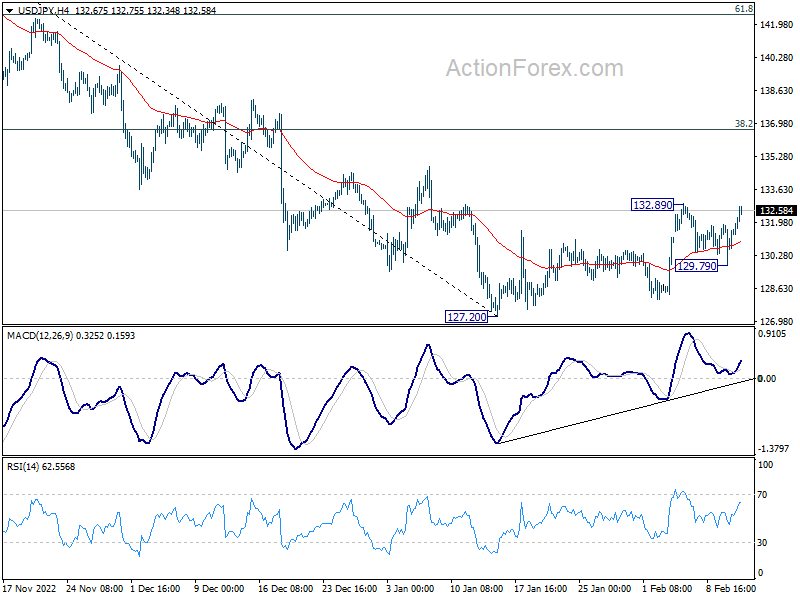

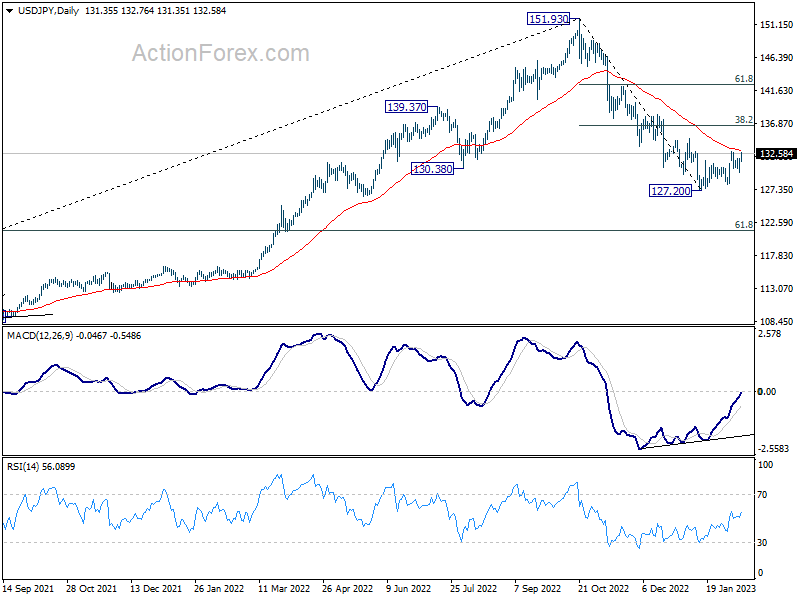

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 130.21; (P) 131.04; (R1) 132.28; More…

Intraday bias in USD/JPY remains on the upside at this point. Break of 132.89 will resume whole rebound from 127.20 short term bottom. Further rally should then be seen to 38.2% retracement of 151.93 to 127.20 at 136.64, even as a correction to the decline from 151.39. For now, further rise is in favor as long as 129.79 support holds, in case of retreat.

In the bigger picture, prior of 55 week EMA (now at 131.47) raises the chance of medium term bearish reversal, but that’s not confirmed yet. Strong rebound from current level, followed by sustained break of 38.2% retracement of 151.93 to 127.20 at 136.64 will argue that price actions from 151.93 is merely a corrective pattern. However, rejection by 136.64 will solidify medium term bearishness for 61.8% retracement of 102.58 to 151.93 at 121.43 and 38.2% retracement of 75.56 to 151.93 at 122.75.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:30 | NZD | BusinessNZ Services Index | 54.5 | 52.1 | 52 | |

| 07:30 | CHF | CPI M/M Jan | 0.60% | 0.50% | -0.20% | |

| 07:30 | CHF | CPI Y/Y Jan | 3.30% | 2.90% | 2.80% |

{kind=link}