Dollar is trading on the softer side again as focus turns to CPI report from the US today. While the markets are finally buying in that federal fund rates would peak above 5% level, there are already some bets on a higher terminal rate. Meanwhile, the bets on a rate cut this year is receding after Fed officials repeatedly rule that out. Eventually, the path would be heavily dependent on the inflation outlook. Elsewhere, Yen is recovering but remains the weakest one for the weak. Sterling is the strongest, followed by Aussie and then Swiss Franc. Euro is mixed for now.

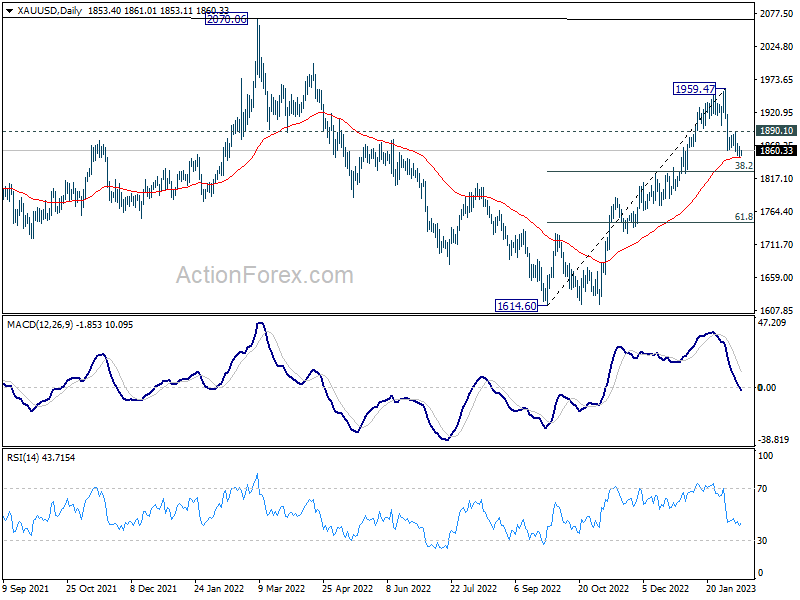

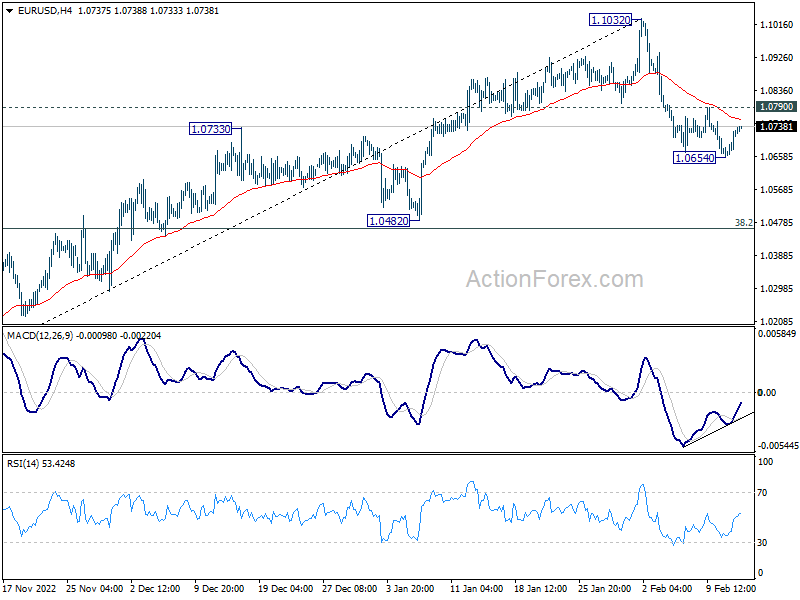

Technically, selloff in Gold and EUR/USD have slowed, as they are both trying to draw support from 55 day EMAs respectively. For Gold, strong rebound from current level, followed by break of 1890.10 resistance, will indicate that pull back from 1959.47 has completed. More importantly, in such case, even if the corrective pattern might extent, rise from 1614.60 should resume at a later stage. Such development would also affirm EUR/USD’s bullishness for another rally through 1.1032.

In Asia, Nikkei closed up 0.64%. Hong Kong HSI is down -0.17%. China Shanghai SSE is up 0.10%. Singapore Strait Times is down -0.25%. Japan 10-year JGB yield is up 0.0020 at 0.506. Overnight, DOW rose 1.11%. S&P 500 rose 1.14%. NASDAQ rose 1.48%. 10-year yield dropped -0.027 to 3.717.

Japan GDP grew 0.2% in Q4 only, missed expectations

Japan GDP grew 0.2% qoq in Q4, below expectation of 0.5% qoq. In annualized term, GDP rose 0.6%, below expectation of 2.0%. GDP deflator rose 1.1% yoy, matched expectations. For the full year of 2022, GDP expanded 1.1%, slowed from 2021’s 2.1%.

Economy Minister Shigeyuki Goto said after the release, “Rising inflation and the global slowdown are risks… But corporate spending appetite hasn’t cooled … we’re not too pessimistic about the outlook.”

Finance Minister Shunichi Suzuki said, “With global monetary tightening continuing, the slowdown in overseas economies could still drag on Japan’s economy as well. We also need to pay attention to the impact from inflation, supply constraints, volatility in financial markets and the spread of Covid cases in China.”

Separately, it’s confirmed that the government nominated Kazuo Ueda as the next BoJ Governor, when Haruhiko Kuroda’s term ends on April 8. Ueda is a 71-year-old former BoJ board member and an academic at Kyoritsu Women’s University.

Australia consumer sentiment dropped back to 78.5, pressures bearing down on consumer becoming intense

Australia Westpac-Melbourne Institute Consumer Sentiment Index fell -6.9%mom from 84.3 to 78.5 in February. The reading was already below the trough of 79.0 as seen in the global financial crisis, but above the 75.6 low in April 2020 when the pandemic first hit.

Westpac noted: “Cost of living pressures and interest rate rises continue to weigh heavily. Hopes of some easing in both have been dashed by the strong December quarter CPI and the RBA’s resumption of its interest rate tightening cycle.”

Regarding RBA policy, Westpac expects another 25bps hike to 3.60% on March 7, a pause in April, and then a final 35bps hike in May to 3.85%.

It added, “The consumer sentiment survey continues to give a very clear warning that the pressures bearing down on the consumer are becoming intense. While spending has held up relatively well to date, we expect an abrupt slowdown to show through in coming months.”

Australia NAB business confidence rose to 6, conditions rose to 18

Australia NAB Business Confidence rose further from 0 to 6 in January. Business Conditions also improved from 13 to 18. Looking at some details, trading conditions rose from 20 to 28. Profitability conditions rose from 13 to 17. Employment conditions rose from 9 to 10.

NAB Chief Economist Alan Oster: “Business conditions picked back up in January after three months of softening in late 2022. There were strong increases in conditions for ‘upstream’ sectors such as wholesale, construction and manufacturing, and importantly, conditions in the more consumer-facing industries remained very strong.”

“Confidence dipped into negative territory late in 2022 but is now back around the average after rebounding over the past two months. The improvement in confidence suggest firms have a more optimistic outlook as concerns about global growth prospects ease, while strong conditions are also providing evidence that the economy is more resilient than previously expected.”

RBNZ survey: OCR expected to rise to 5% by year end

According to RBNZ Survey of Expectations (Business), one-year inflation expectations rose slightly from 5.08% to 5.11% in February quarter. The reading was similar to value from the 1990 survey when actual CPI was 7.60%.

On the other hand, two-year inflation expected dropped further from 3.62% to 3.30%. The spread also narrowed, with no respondent answering below 2.00% or above 6.00%.

Official Cash Rate (OCR) expectations increased notably by 74 basis points from 4.25% to 4.89% by the end of this quarter. OCR is expected rise further to 5.00% by the end of the year, up from 4.67%.

Looking ahead

UK employment data is the main focus in European session. Swiss will release PPI and Eurozone will publish GDP revision.

Later in the day, US will release CPI data as one of the main events of the week.

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0677; (P) 1.0704; (R1) 1.0751; More…

EUR/USD recovered after edging lower to 1.0654 and intraday bias is turned neutral again. On the downside, break of 1.0654 will resume the corrective fall from 1.1032 to 38.2% retracement of 0.9534 to 1.1032 at 1.0463. Strong support should be seen around there to bring rebound, at least on first attempt. On the upside, above 1.0790 minor resistance will turn bias back to the upside for retesting 1.1032 high instead.

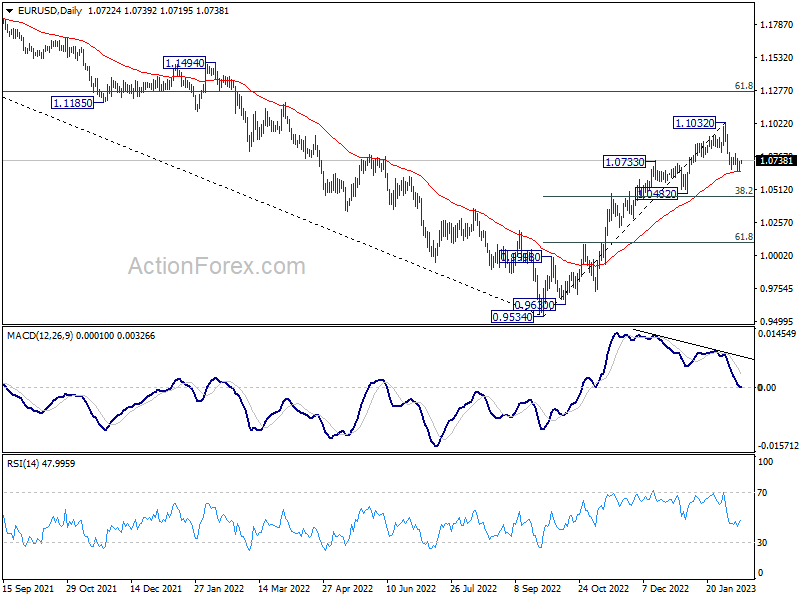

In the bigger picture, the rally from 0.9534 low (2022 low) is a medium term up trend rather than a correction. Further rise is in favor to 61.8% retracement of 1.2348 (2021 high) to 0.9534 at 1.1273 next. This will remain the favored case as long as 1.0482 support holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | AUD | Westpac Consumer Confidence Feb | -6.90% | 5.00% | ||

| 23:50 | JPY | GDP Q/Q Q4 P | 0.20% | 0.50% | -0.20% | |

| 23:50 | JPY | GDP Deflator Y/Y Q4 P | 1.10% | 1.10% | -0.30% | |

| 00:30 | AUD | NAB Business Conditions Jan | 18 | 12 | ||

| 00:30 | AUD | NAB Business Confidence Jan | 6 | -1 | ||

| 02:00 | NZD | RBNZ Inflation Expectations Q/Q Q1 | 3.30% | 3.62% | ||

| 04:30 | JPY | Industrial Production M/M Dec F | 0.30% | -0.10% | -0.10% | |

| 07:00 | GBP | Claimant Count Change Jan | 9K | 19.7K | ||

| 07:00 | GBP | ILO Unemployment Rate (3M) Dec | 3.70% | 3.70% | ||

| 07:00 | GBP | Average Earnings Excluding Bonus 3M/Y Dec | 6.50% | 6.40% | ||

| 07:00 | GBP | Average Earnings Including Bonus 3M/Y Dec | 6.20% | 6.40% | ||

| 07:30 | CHF | Producer and Import Prices M/M Jan | 0.20% | -0.70% | ||

| 07:30 | CHF | Producer and Import Prices Y/Y Jan | 2.20% | 3.20% | ||

| 10:00 | EUR | Eurozone GDP Q/Q Q4 P | 0.10% | 0.10% | ||

| 10:00 | EUR | Eurozone Employment Change Q/Q Q4 P | 0.10% | 0.30% | ||

| 11:00 | USD | NFIB Business Optimism Index Jan | 89.8 | |||

| 13:30 | USD | CPI M/M Jan | 0.50% | 0.10% | ||

| 13:30 | USD | CPI Y/Y Jan | 6.20% | 6.50% | ||

| 13:30 | USD | CPI Core M/M Jan | 0.40% | 0.40% | ||

| 13:30 | USD | CPI Core Y/Y Jan | 5.30% | 5.70% |

{kind=link}